Puget Sound Energy and Avista told the Washington Utilities and Transportation Commission that they have taken steps to build clean energy resources quickly to qualify for expiring federal tax credits, while voicing concern that limited transmission capacity and the state’s greenhouse gas targets pose challenges.

PSE and Avista provided comments as part of the Washington UTC’s investigation into how federal tax law changes impact clean energy projects in the state. The deadline to submit comments in the docket was March 20.

The UTC’s investigation follows new rules imposed by the Trump administration in summer 2025 that changed eligibility requirements for tax credits on new wind and solar construction.

Under the rules, solar and wind projects face a July 4 construction-start deadline to claim the tax credits. A project must begin significant physical construction before July 5, proceed continuously and be completed within four calendar years to be eligible. (See IRS Guidance on Wind and Solar Credits Not as Bad as Feared.)

For PSE, the new laws have prompted the utility to invest in projects “earlier than it otherwise would have absent the tax law changes presented in [One Big Beautiful Bill Act],” Wendy Gerlitz, PSE’s director of regulatory policy, wrote in the utility’s comments.

PSE prioritizes projects with a construction-start date before July 4 and requires involved parties to comply with the law’s sunset deadlines, Gerlitz wrote.

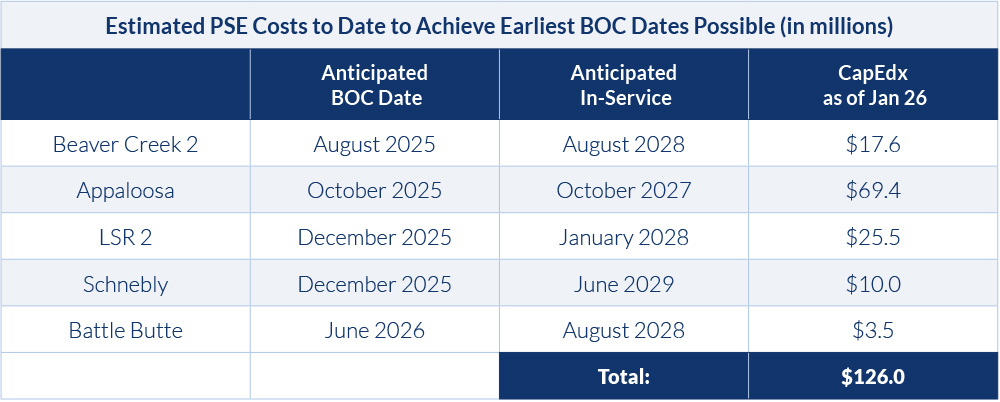

At least five projects are slated to begin construction before the July 4 deadline, including Beaver Creek, a 248-MW utility-scale wind project in Montana; the Appaloosa solar project, a 142-MW project in Washington; and a 130-MW solar project in Montana called Battle Butte, according to PSE’s filing.

One of the major challenges to securing the tax credits is “the slow pace of the Bonneville Power Administration interconnection studies and commencement of upgrades,” Gerlitz stated.

BPA paused certain planning processes in 2025 to consider how to address nearly 61 GW of transmission service requests. The agency has presented several proposals to reduce the queue, but the efforts have been criticized as moving too slowly for utilities in Oregon and Washington to meet strict greenhouse gas standards and secure the federal tax credits. (See Northwest Lawmakers Explore Building Transmission Without BPA’s Help.)

“BPA is undergoing a significant reformation of our queue processes,” agency spokesperson Kevin Wingert told RTO Insider in an email. “This reform will ultimately drive major transmission construction and integration timelines from what is seen typically across the nation of 15 or more years down to a four-to-six-year average.”

Wingert noted that BPA launched the $6 billion Grid Expansion & Reinforcement Portfolio, which includes 23 projects that are being brought online between now and 2035.

Although PSE is collaborating with BPA on the interconnection studies, “in general, actual progress has been too slow to facilitate timely [commercial operation dates] for projects that otherwise have a high probability of meeting the year-end 2029 and 2030 tax credit deadlines,” according to Gerlitz.

Washington’s Clean Energy Transformation Act (CETA) requires all electric utilities in the state to become greenhouse gas-neutral by 2030 (allowing for use of offsets and other programs) on the way to generating all power from emissions-free resources by 2045. It also prohibits utilities from serving their Washington customers with any coal-fired generation after 2025. (See Washington Agencies Adopt New Rules to Implement CETA.)

BPA’s transmission planning pause coupled with Trump’s new tax laws “will certainly increase the cost of compliance with CETA and negatively impact PSE’s financial health, making it more challenging to accelerate important renewable projects,” Gerlitz contended.

Gerlitz urged the UTC to mitigate the impact of the federal tax changes, saying the utility is speeding up investments in projects that “will not be placed in service for many years.”

“This acceleration places additional pressure on PSE’s credit metrics, which is a critical measure of PSE’s financial health and a key set of metrics for credit rating agencies and fixed-income investors,” Gerlitz added.

Avista made similar requests, proposing the UTC accelerate permitting, support procurement processes and provide incentives to developers to acquire equipment to show that “significant physical work” has begun as required under the bill, according to Shawn Bonfield, senior manager of regulatory policy and strategy at Avista.

Bonfield wrote that the company initiated a request for proposals process in 2025 for renewable projects with the uncertainty around the tax credits in mind.

For example, the utility sped up the RFP release schedule to benefit tax-advantaged projects and requested proposals for additional renewable energy before tax credit deadlines.

“Avista is working towards agreements with selected developers based on proposals that meet identified needs, and as applicable, have a planned path towards achieving tax credits,” Bonfield wrote.

“The accelerated expiration of federal tax credits for wind and solar resources is concerning to Avista, particularly as customer growth calls for additional resources into the future,” he stated. “Avista’s top priority is to keep power safe, reliable and affordable for its customers, and the loss of federal tax credits has a significant impact on those goals.”