FERC has approved NorthWestern’s acquisition of Puget Sound Energy’s shares in the coal-fired Colstrip power plant in Montana and authorized NorthWestern to sell electricity produced by the plant.

FERC issued two orders Feb. 27 related to the company’s acquisition of shares in Colstrip (ER26-129 and ER26-411). Both orders concern NorthWestern’s subsidiary NorthWestern Colstrip, which was created to hold ownership in the coal-fired generation asset, according to FERC.

In the first order, FERC accepted NorthWestern’s cost-based rate (CBR) tariff for short-term sales of electricity produced by its share of the plant. In the second order, the commission approved a power purchase and sale agreement between NorthWestern and Mercuria Energy America.

FERC said both filings were “just and reasonable and not unduly discriminatory or preferential.” The orders are effective Jan. 1, 2026.

NorthWestern reached an agreement in 2024 to acquire PSE’s 370-MW stake in two units of the Colstrip power plant effective Jan. 1, 2026. The deal came about after PSE was forced to exit the plant because of Washington state law.

NorthWestern also has acquired Avista’s 222-MW share in the plant, giving the company 55% ownership, according to NorthWestern’s website.

The transaction received backlash from Montana Public Service Commissioners and the Montana Environmental Information Center. The opponents argued in filings with FERC that NorthWestern failed to receive authorization for the agreement under Section 203 of the Federal Power Act.

The opponents said there is a risk that “generation from the Colstrip station will be contracted to a large load customer and will not benefit the people and small businesses of Montana,” according to the orders.

FERC rejected those arguments, saying the FPA requires prior authorization only for transactions valued at more than $10 million.

NorthWestern acquired PSE’s shares in the power plant “at a transaction price of $0. Therefore, this transfer is under the $10 million threshold required for commission jurisdiction under Section 203,” the orders stated.

Montana Gov. Greg Gianforte (R) supported the deal, saying the plant is “essential” to “maintaining reliability during winter conditions, stabilizing the regional grid and keeping energy affordable for Montana families, farmers and employers,” according to the orders.

According to the CBR filing, NorthWestern is negotiating various deals and made the filing to ensure it has the authority to make any short-term sales while committing to filing any long-term sale agreements with the commission.

FERC accepted NorthWestern’s proposed maximum demand charges under the CBR:

$11,920/MW-month

$2,750/MW-week

$390/MW-day

$16.30/MWh

The order states that all services agreements should be governed under the terms and conditions of the Western Systems Power Pool agreement.

Meanwhile, NorthWestern’s agreement with Mercuria Energy provides for the sale of long-term capacity and energy from the power plant. NorthWestern is responsible for all “interconnection and transmission arrangements, electric losses and necessary costs to deliver energy, capacity and ancillary services to the point of delivery,” according to the order.

FERC found the agreement’s proposed capacity and energy rates “just and reasonable” because they fall below the ceiling demand charge in the associated CBR tariff, the order stated.

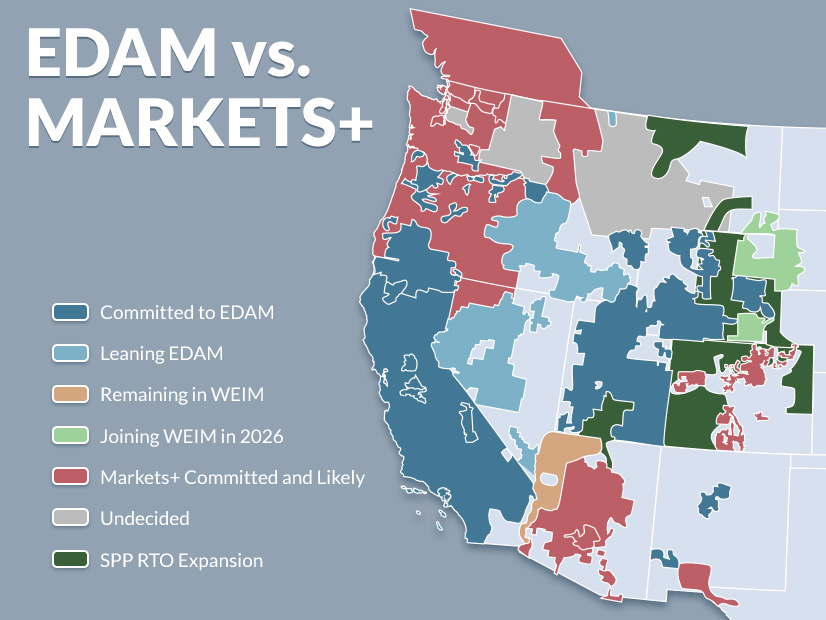

BOULDER, Colo. — Conversations remained cordial despite the ongoing competition between CAISO and SPP in the West as the RTOs’ top executives took the stage at Yes Energy’s annual EMPOWER conference.

RTO Insider’s Robert Mullin moderated a panel in which Elliot Mainzer of CAISO and Lanny Nickell of SPP emphasized the importance of cooperation and friendly competition while making their pitches for their respective Western markets.

CAISO is preparing to launch its Extended Day-Ahead Market (EDAM) in May, while SPP plans to roll out Markets+ — which includes day-ahead and real-time market components — in October 2027.

Over the past few years, the competing markets have fought to sign up participants across the West. CAISO plans to go live with EDAM in May with the participation of PacifiCorp, with Portland General Electric to join in the fall. SPP also has several major commitments, headlined by the Bonneville Power Administration’s decision in May 2025 to join Markets+. (See BPA Chooses Markets+ over EDAM.)

Mainzer clearly was disappointed with BPA’s choice. He was BPA administrator and had worked there for 18 years before moving to CAISO in 2020.

Regardless of the choices of individual entities, CAISO and SPP “continue to motivate each other to get better,” Nickell said. “If one of us goes away, the motivation to improve isn’t as great.”

Mainzer and Nickell emphasized those potential cost savings associated with the adoption of day-ahead markets in the West.

Mainzer said the success of the Western Energy Imbalance Market (WEIM), launched by CAISO in 2014, gave participants confidence in the possibilities of regionwide markets.

“Now we’re seeing this second chapter,” he said, with participants realizing “we’re leaving money on the table now in the day-ahead.”

In SPP’s eastern RTO territory, Nickell said the wholesale markets provided about $10 billion in adjusted production cost savings over the past five years.

The launch of organized day-ahead markets in the West will “allow the provision of energy in a much more affordable way because we will have access to resources across a much broader region, and we’ll be able to commit those on a day-ahead basis, which will ensure a much higher degree of reliability,” he added.

The CEOs’ perspectives differed regarding potential issues associated with the seams between the market areas, reflecting ongoing debates about the benefits of the two markets.

“When you look at that map and look at the Swiss cheese that’s opening up in the West, that’s going to be challenging to deal with,” Mainzer said. While seams agreements can help mitigate issues, seamless market footprints provide the greatest reliability value, he added. (See FERC Report Urges West to Address Looming Market Seams Issues.)

As the lines between markets harden, “I don’t think any seams agreement or combination of seams agreements is going to be able to fully restore the loss of efficiency that we’re going to get from breaking apart [WEIM] and having multiple market operators,” he said. “We’ll work hard to do it, but it is a point of departure.”

Nickell expressed more optimism about the potential for productive seams agreements and said the only way to truly eliminate all seams is through the creation of a regionwide RTO.

“Seams exist all over the West today, and they’re still going to exist … there’s still going to be balancing authorities, there’s still going to be transmission owners and providers operating their own tariffs,” he said. “We’re simply operating markets.”

“Our job is to work together to try to optimize the exchange of energy, not only within the market but across the two markets,” he added. “I think we can optimize those seams in a way that assures that energy is produced, it’s accessed and it’s delivered in a much more reliable way.”

Governance Structures

Trust in SPP’s governance structure has been a key factor for entities deciding to join Markets+, Nickell said. BPA cited governance as a key qualitative factor in its decision to join Markets+.

Nickell emphasized the importance of developing long-term trust with stakeholders, saying trust is “hard to get and it’s easy to lose, and we’ll do everything we have to maintain that trust that our participants have with us.”

“We’ve operated a highly engaged stakeholder process for decades,” he said. “We’re experienced in doing that, and I think a lot of the Western participants and stakeholders saw that and found it attractive.”

Mainzer said participants joining EDAM have been motivated primarily by economic considerations.

“We’ve tried to really build on the platform of physics and economics… and continue evolving the governance,” he said.

In an effort to address concerns about the influence of California policymakers on EDAM, the state passed legislation in the fall enabling the creation of an independent regional organization to govern WEIM and EDAM. (See Newsom Signs Calif. Pathways Bill into Law.)

When he was CEO of BPA, Mainzer said he knew “as well as anybody” the governance concerns about CAISO’s markets.

“The governance structure for [CAISO] for many years was just not a sustainable structure for true multi-state participation,” he said. “That’s why we spent five years working to get that law passed last year.”

“You’ve done great work — I think it’s awesome that you were able to get those governance reforms in place,” Nickell said to Mainzer.

Asked whether the ultimate goal of Markets+ is to expand SPP’s western RTO footprint, Nickell said it’s possible SPP will continue to expand its RTO operations in the West but emphasized that “you can’t force somebody into an RTO — that’s a voluntary construct.”

“It takes time and it takes people getting comfortable with that approach,” he said.

SPP’s western RTO expansion is to take effect April 1 when it incorporates utilities in Arizona, Colorado, Utah and Wyoming.

Mainzer framed the developments in the West as a process of natural evolution that started with the implementation of real-time markets and has moved gradually toward the addition of components that can add value for the region.

“I think both our constituencies have tended to prefer this matchbox slogan of ‘evolution, not revolution,’” he said, adding that the West can benefit from best practices and lessons learned from existing markets across the country.

He emphasized the importance of maintaining local responsibility for resource adequacy planning and generation development as the markets grow.

“You are going to see a ton of change and continued evolution, but we get the chance to do it with steps and features that we think really produce value with less downside,” he said.

U.S. Sens. Peter Welch (D-Vt.) and Dave McCormick (R-Pa.) have introduced the Reconductoring Existing Wires for Infrastructure Reliability and Expansion (REWIRE) Act, which aims to accelerate the deployment of advanced transmission technologies.

The bipartisan bill comes as Congress is working on permitting legislation. It seeks to streamline environmental reviews for projects like reconductoring or installing grid-enhancing technologies (GETs) on existing rights of way.

“We’re up against the clock when it comes to meeting America’s growing energy needs,” Welch said in a statement March 2. “Increasing the capacity of the grid by accelerating the permitting process and incentivizing practices like reconductoring will not only allow us to connect new and affordable clean energy to the grid — it’ll also save consumers money.”

Demand is projected to rise by as much as 5.7% by 2030. This requires about 5,000 miles of new, high-capacity transmission lines each year, but in 2024 the country saw only 322 miles constructed, the senators’ offices said.

“Electricity demand in Pennsylvania and across America is rising rapidly, and that requires innovative solutions to strengthen our electric grid and cut through the bureaucracy that’s holding us back,” McCormick said in a statement. “The bipartisan REWIRE Act is exactly the kind of common-sense fix we need by using the infrastructure we already have, bringing down costs and stopping years of unnecessary permitting delays from standing in the way of real progress.”

The REWIRE Act would encourage upgrading existing transmission with advanced conductors that can double the capacity of existing transmission lines, which is far cheaper and quicker than building new lines from scratch.

The bill would create a categorical exclusion from the National Environmental Policy Act for projects that increase grid capacity within existing rights of way such as reconductoring, GETs or deploying energy storage.

It would direct FERC to improve the return on equity for reconductoring projects to encourage wider adoption of advanced transmission conductors. The bill would allow state energy offices to use federal funds from the Department of Energy to conduct feasibility studies for reconductoring and GETs projects.

The bill proposes regional collaboratives between DOE, national laboratories and universities to evaluate grid performance and identify good opportunities for deploying advanced transmission. DOE would be authorized to create a national clearinghouse of advanced transmission applications, case studies and best practices to spread the information nationally.

The REWIRE Act has a lengthy list of supporters including American Clean Power, American Council on Renewable Energy, Bipartisan Policy Center Action, Conservative Energy Network, CTC Global, Electricity Consumers Resource Council, EQT Corporation, Grid Action, GridWise Alliance, National Electrical Manufacturers Association, PPL Corporation, the Solar Energy Industries Association and others.

“The REWIRE Act is a smart, bipartisan step to unlock more capacity from the grid we already have,” Grid Action Director Christina Hayes said in a statement. “Reconductoring and advanced transmission technologies can deliver meaningful reliability gains and additional transfer capability faster and more cost-effectively by working within existing rights of way.”

The demand growth the industry is facing requires both the kind of near-term upgrades that would be encouraged by the bill, along with a buildout of completely new transmission, she added.

“The REWIRE Actis exactly the kind of pragmatic, bipartisan policy needed to unlock grid capacity quickly and affordably,” CTC Global Chief Policy Officer Theodore Paradise said in a statement. “By accelerating reconductoring with advanced conductors in existing rights of way, the bill lowers costs, strengthens reliability and delivers meaningful transmission capacity on timelines the grid urgently needs.”

When it comes to the grid, can artificial intelligence be two things at once? Demand planners and climate realists see AI as the bad guy, driving up demand and grinding decarbonization goals into the ground. Yet industry leaders and techno-optimists believe it can be the good guy.

I met with some of Silicon Valley’s biggest brains recently to unpack this complex question — and, critically, whether AI can be the good guy while meeting FERC-approved NERC Critical Infrastructure Protection (CIP) standards.

There’s no doubt AI could be exponentially faster, smarter, more innovative and more efficient than the current workforce, but can it be reliable? We’ve all heard of AI hallucination in everything from government reports to research papers, but when you are dealing with HVDC, errors can have life-and-death consequences.

If the industry does not quickly define “reliable AI” and build guardrails around its deployment, we risk importing stochastic behavior into systems designed for determinism.

That is not a technology debate. It is a reliability and safety debate. And it is one RTOs, regulators, grid and power plant operators, and utilities cannot afford to postpone.

The AI-Enabled Vision for the Future Grid

Dej Knuckey |

AI can optimize transmission and distribution, move more electrons through the same wires, free workers from mundane tasks, and manage preemptive maintenance. And there are ways it can help the grid that we are only beginning to imagine.

One of the most interesting use cases is building photorealistic digital twins of nuclear power plants and substations to enable remote operations and maintenance, which I’ll dig into more later.

Another application involves drones analyzing snow-cloaked power lines without waiting for a winter storm to provide the training environment. AI not only creates images of the storm-that-doesn’t-exist but also teaches the system what to look for in the white-on-white, post-storm landscape from all the angles an experienced drone pilot would use. The goal: eliminate the need to wait until roads are accessible before lines can be inspected. Grid operators will be able to keep drones in habs (the boxes drones call home) near HVDC towers so they can deploy after storms and for regular maintenance.

There also are ways to make AI less power-hungry, at least in an electron sense. AI may still want to rule over its human underlings but can do so more efficiently with better data compression.

Why AI Sometimes Gets it Wrong

AI is ubiquitous: You can’t do a simple web search without an AI-generated summary popping up. Sometimes it’s great. Other times it’s amusingly wrong.

“When I ask it to search the web, nine out of 10 times it gets the right source with the right quote. But 10%, I go to the link that it showed, and it doesn’t exist,” said Yuriy Yuzifovich, chief technology officer of enterprise AI at GlobalLogic, while referring to a popular AI assistant.

Users refer to AI errors as hallucinations. When I was using early versions of ChatGPT to research technical topics, rather than admit “I can’t find any sources for that,” the eager-to-please AI would sometimes invent research papers. If I’m searching for sources for an RTO Insider article, that hallucination is an annoyance. I correct it and move on.

And here’s the part that’s poorly understood in the public conversation: The large language models (LLMs) that power consumer AI tools are built to behave this way. They are intentionally probabilistic.

Hallucinations and HVDC Don’t Mix

You have to go inside LLMs to understand how and why it can deliver errors with such confidence.

LLMs “understand” the world with tokens and vectors. Tokens break language down into small chunks that AI models read, while vectors represent those tokens in a numerical, high-dimensional way that give each token context and relationships with similar tokens. If “All-Bran” were a token, its vector would tell you it’s in aisle 5 on the third shelf with all the other cereals. AI constructs answers to questions by stringing together a series of tokens it has found using vectors.

Continuing to use a three-dimensional analogy to simplify the multidimensional space that AI operates in, imagine AI is doing your shopping. It enters the supermarket, looking where the vector has directed it. At the third shelf of aisle 5, it grabs the closest box of cereal with bran in its name. Because it is closer than the proper target and similar enough, the model assumes it’s right and stops looking.

As it gives you bran flakes, it hasn’t made a wild guess, but it has delivered something any fan of All-Bran (yes, they exist) would consider wildly, soggily wrong.

“The randomness of the answer is built in. It’s a feature. It’s not a bug,” Yuzifovich said.

In some cases, such as writing a conference presentation, that randomness can look like creativity. But the stakes are higher in the electricity sector. The grid, especially the HVDC side, operates with life-and-death stakes. If AI was advising one of your control room operators during a switching event, or guiding a field crew during storm restoration, that “nine out of 10 times” isn’t innovation. It’s an unacceptable risk.

Does this mean there’s no space for AI in managing critical infrastructure? The problem is most public discourse treats “AI” as a monolithic technology. It isn’t. And if regulators and operators fail to draw sharper distinctions, we risk regulating the wrong thing while deploying tools that introduce the instability we work hard to eliminate.

When ‘Good Enough’ AI Isn’t Close to Good Enough

Utilities have been pitched an avalanche of AI solutions over the past few years: copilots for engineers, chatbot overlays for procedures, systems that promise to answer questions from internal manuals.

On slides, it looks compelling, but in practice, the results have been uneven.

“Most of these organizations love the idea that you’re going to do something with their data and get some magic beans of intelligence back,” Malcolm Hay, GlobalLogic’s vice president of energy, said. “There have been a lot of proof of concepts done that are kind of ‘meh.’ They deliver a bit,” he said, but are not accurate enough to be relied on in operational settings that can’t tolerate any kind of ambiguity. “Any hallucinations … would destroy confidence and obviously [pose] security and safety risks.”

Retrieval-augmented generation (RAG) is a perfect example of this gap between promise and performance. Instead of letting a model roam the internet, you point it at curated internal documents. The failure mode, however, is often indistinguishable.

“RAG is similar to ChatGPT, but instead of the internet, you give your documents,” Yuzifovich said. “The results are very similar: most of the time it gets it right, but sometimes it doesn’t — and when it doesn’t, you don’t know when.”

That last clause is the operational killer. If a human has to verify every output, the efficiency case collapses.

Meanwhile, workforce pressures are intensifying. During one storm restoration workshop, a utility described line workers running 16-hour shifts after a major event. “We need to really help them and give them the tools they need to support us,” said Carlos Elena-Lenz, vice president for digital enablement and transformation at Hitachi Energy.

Those tools cannot be probabilistic guessers.

What ‘Reliable AI’ Actually Means

In the aerospace world, craft or launch vehicles that carry people are called “human-rated” in contrast to vehicles that carry a non-human payload. They are designed to a higher standard because their failure has more significant consequences. It’s a concept that easily translates to the energy world. Every day, crews work with a complex system that, if mishandled, could have fatal consequences.

In safety-critical environments, the definition of AI success is radically different from Silicon Valley’s definition.

Four requirements for “Reliable AI” surfaced repeatedly in my conversations.

1. Deterministic, not Stochastic

If you ask the same question under the same conditions, you have to get the same answer every time. “It’s very important to show … on a small subset … that no matter how many times you’re asking the same question, it’s the same answer,” Yuzifovich said. Variability is intolerable in a control room.

2. Grounded in Structured Knowledge

The foundation of reliable AI is not linguistic fluency; it is structured domain knowledge. “Knowledge is just a collection of interconnected knowledge: This fact is related to this fact,” Yuzifovich said. “With LLMs, we can finally produce enormous amounts of this knowledge as code.”

This is not “upload your PDFs and hope.” It requires iterative extraction, validation and SME oversight, and multiple passes of extraction with a human in the loop to codify critical rules.

3. Able to Say ‘I Don’t Know’

Safety-critical systems must value accuracy over giving an answer. It needs to know when it doesn’t know and never guess. In other words, we want a Hal that will say, “I’m sorry, Dave. I’m afraid I can’t do that.” An “I don’t know” state is not weakness. It is governance.

4. Traceable and Auditable

When an AI suggests an action, operators must see the chain of reasoning and trace back as far as needed, even if it means going back to the source documents that contain the standard operating procedures. Mainstream AI models often are opaque by design, but grid-grade AI must be engineered for auditability. The system must behave like a senior engineer, not just a librarian. It must be grounded in rules, not merely fluent in text.

Building the World of Truth

As part of the nation’s critical infrastructure, utilities, power plant owners and grid operators must isolate their data systems from external sources to ensure cybersecurity. That means even if some of the data exists on the web, it’s not accessed there. For example, the installation and commissioning manual for a transformer may exist on the manufacturer’s website, but it will need to be replicated inside a secure system for internal use.

To create “knowledge as code,” everything gets uploaded, Renan Giovanini, chief technology officer of energy business at GlobalLogic, said. And by everything, he means everything: the original RFQ with specs, the operations manuals of every component, the history of faults and repairs.

For a greenfield plant, that’s probably already digitized and easily uploaded. However, for a 70-year-old substation with transformers as old as the average worker, creating the knowledge base requires sifting through warehouses of records and digitizing the handwritten notes of electricians who have serviced the plant over the years.

The sheer magnitude of the task may seem overwhelming and industry players will need to believe there will be a real return on that investment. The challenge for technology providers will be to help customers make the case for the long-term benefits the considerable investment will deliver.

From Chatbots to Operational Systems

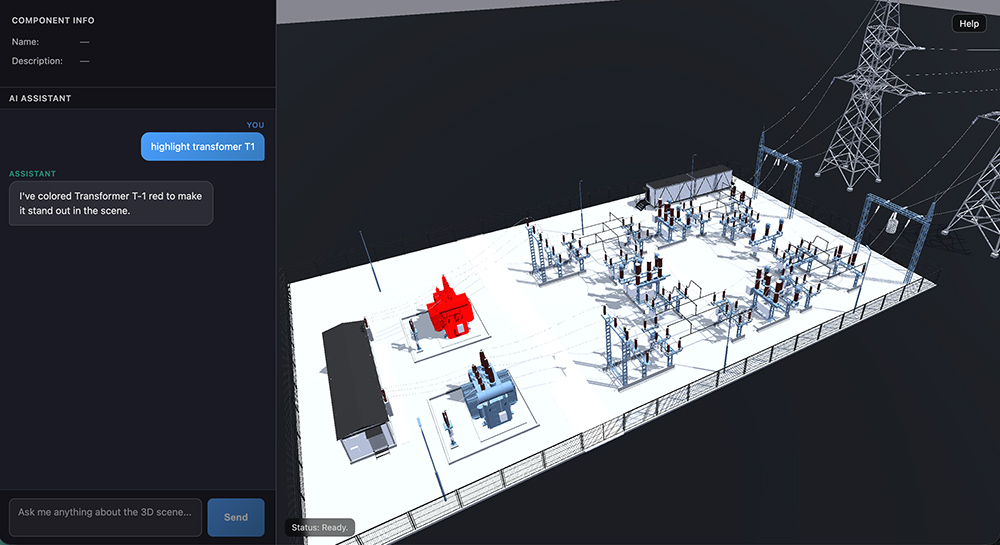

The public narrative around AI remains chatbot-centric. Inside utilities and OEM environments, the picture looks very different. In one nuclear maintenance platform demonstration, a GlobalLogic project that is live today, engineers built a detailed digital twin tied directly to procedures and asset data.

“The customer wanted to have a solution to better coordinate their maintenance teams, so they could remotely get together and plan for work,” Giovanini said. “They had team members across the globe, that, in the past, would go to a [Microsoft] Teams meeting.” The challenge would come as soon as people on the call needed the position of a particular piece of equipment or access to a user guide. “We worked with them to create a digital twin representation of the nuclear power plant and enrich it with many different data sets, user guides, maintenance procedures and so forth.”

The representation replicates the plant’s facilities in an immersive metaverse, enabling remote access, real-time collaboration and AI-powered operations management. The visual layer is important, but the real innovation is underneath: structured rule enforcement tied to plant documentation.

A digital twin of a nuclear power plant (right) is a realistic representation of the real thing (left) layered with manuals, data and other intelligence. | GlobalLogic

In a demonstration of a substation digital twin under development, those structured rules became concrete: an operator instructed the AI to open a disconnector. The system refused.

“I cannot open this disconnector because there is a circuit breaker that must be opened first,” it replied.

The rule was not manually coded by a software engineer.

“What we take is a standard operating procedure from the utility that gets ingested by a knowledge database. There is no need now for a software engineer to transform that into rules,” Giovanini said.

It enables procedural enforcement at machine speed.

In storm response, similar pipelines are emerging, as in the example of the inspection drones. “We started using synthetic data generation to create snowy scenes and we’re feeding them into our computer vision model,” Elena-Lenz said.

Beyond having a fleet of drones that can inspect and report on damage, the sensing-to-decision architecture should be able to collate the damage reports, prioritize them, and then feed into a workforce management platform that can assign the work based on the crew’s locations, tools and capacity, he said.

Remote teams can interact with a digital representation of a substation using natural language questions. | GlobalLogic

The Human Knowledge Emergency

The most urgent case for reliable AI is not automation. It is retention. The industry is facing a crisis as the generation that holds deep experience retires.

“We’re losing this context for these old systems,” Giovanini said. “By capturing this knowledge into a digital format, that tribal knowledge now will be part of this utility or company knowledge space.”

Another engineer described veterans who can diagnose issues by sound alone. “They can go out to a substation and just by listening tell you if everything is working. You can’t create software that beats decades of knowledge.” Yet the industry must capture as much of that knowledge as it can before it loses that experience, and possibly train systems in ways no one planned, such as audio detection of certain fault types.

Reliable AI, in this context, becomes a continuity strategy, embedding institutional memory into auditable systems.

Planning for an AI-enabled Future

By the end of a dozen conversations and demonstrations, I’d laid my dun-colored climate realist glasses to one side and donned a techno-optimist’s hat. AI data centers’ demand may create a challenge for the grid, one that will put emissions reduction goals on the back burner in a way that I find hard to stomach, but that doesn’t mean the industry won’t also benefit from it.

The select few examples of how AI can multiply human capabilities and preserve human experience for generations to come barely scratch the surface. There are many ways AI can help the industry become faster, smarter, safer and more responsive at getting more out of existing assets.

But regulators and industry leaders need to ensure the industry maintains the highest standards in this rapidly evolving digital world.

“Reliable AI” guardrails are essential, not only to meet NERC’s CIP requirements, but to also continue protecting the grid and the people who work on it and live near it in the conservative, risk-averse way the industry holds as sacred.

Power Play Columnist Dej Knuckey is a climate and energy writer with decades of industry experience.

MISO said its modeling estimates show it could have 413 to 501 GW of installed capacity on its system by 2045.

The grid operator is nearing its final four futures scenarios, which estimate the system makeup 20 years down the road for transmission planning purposes. The nearly final estimates are higher than MISO’s prior draft release. (See MISO Draft Tx Planning Futures Envision 400-GW Supply or More by 2045.)

Across all futures, MISO shows that solar, natural gas and wind resources would jockey for lead fuel type:

MISO’s low-end estimate of 413 GW includes 32% solar, 26% gas and 21% wind. However, it expects to use gas only 14% of the time and lean on wind and solar 28 and 27% of the time, respectively.

The middle-of-the-road future has a 437-GW fleet at 28% gas, 26% wind and 23% solar. Gas would supply output 13% of the time, with solar at 17% and wind at 36%.

The third future, which allows for the fastest fleet transition, contains 501 GW split among 27% wind, 27% gas and 24% solar. In that scenario, gas generation is dispatched 10% of the time, with solar at 18% and wind 36%.

Finally, MISO’s supply chain-constrained scenario has a 455-GW fleet by 2045, at 30% solar, 28% gas and 20% wind. Gas and solar are used equally, 23% of the time, while wind is responsible for 28%.

In all four cases, battery storage remains at 4% of the mix. “Other” generation (oil, conventional hydro, biomass, geothermal and other resource types) takes a 10% slice in nearly all futures.

The most aggressive, 500-GW future contemplates an 8% share of nuclear power that supplies 25% of output — the highest MISO foresaw. Meanwhile, coal ranges between 4% (the supply constrained future) and 1% (the aggressive fleet change future) and mostly runs 1% of the time.

MISO said its resource mixes were shaped by planning reserve margin requirements and states’ carbon-reduction and renewable energy goals.

Members have 171 GW planned by 2045. Natural gas and solar take the largest share at 53 and 50 GW, respectively. Members also plan to add 30 GW of the “other” generation, 24 GW of wind, 12 GW of battery storage and 3 GW of nuclear.

MISO currently has 202 GW of installed capacity.

The RTO plans to finalize its 20-year transmission planning scenarios early in the second quarter of 2026; it will host a final stakeholder workshop April 9.

At a Feb. 26 workshop webinar to discuss the futures, MISO Policy Planner Logan Pollander said all four futures are resource adequate. He said the RTO’s loss-of-load expectation analysis exhibited no expected unserved energy in each of the selected study years (2030, 2035 and 2045).

The modeling doesn’t include a finalized capacity accreditation method for energy storage. Multiple stakeholders said MISO was missing a large piece of the puzzle if it didn’t decide accreditation values for storage.

Pollander said the results could change once MISO factors in storage accreditation.

Red States Ask for Comparison Model Free of Clean Energy Goals

Bill Booth, a consultant to the Mississippi Public Service Commission, asked MISO to create a purely economic expansion future that doesn’t consider any carbon goals in order to see how much transmission might be built for the purposes of decarbonization.

MISO Executive Director of Transmission Planning Laura Rauch said the RTO is not comfortable with scenarios that diverge from enacted carbon-reduction laws and the goals of members.

South Dakota Public Utilities Commission staffer Darren Kearney said he would like to see a “counterfactual” of what the buildout would be without the constraints of carbon abatement, so states with carbon-reduction goals don’t pass on their costs to those without them.

Rauch said MISO could have a discussion on that once new transmission is proposed.

But the Union of Concerned Scientists’ Sam Gomberg cautioned the RTO against singling out renewable energy goals to make some states’ cost allocation smaller.

“In each state you can find biases and preferences … written in state code that drive resource adequacy decision-making outside the bounds of least-cost planning,” Gomberg said.

For example, he said, if states restrict or shut out cost-effective solar or wind generation when their political climate is suited for it, that’s putting their thumb on the scale. “We could go in countless directions here … and find ourselves in a death spiral of paralysis by analysis,” Gomberg said.

According to MISO, just 3% of its load base is not associated with any carbon-reduction goals.

The Independent Market Monitor has been in discussions with MISO about introducing a sensitivity that reflects a maximum willingness to pay for carbon reductions. IMM David Patton has said the RTO should “balance cost objectives with carbon objectives” in the futures.

At previous futures workshops, Patton has said it’s worthwhile to examine the point at which members wouldn’t invest in a new clean energy technology because it would lose money or “produce retail rates that are astronomical.”

Representing MISO industrial customers, Kavita Maini said she had a hard time believing states would reason that “even if this standard costs a million-bajillion dollars, I still want to pursue this” when rates become unaffordable.

WEC Energy Group’s Chris Plante said he struggled with how MISO could assume no expected unserved energy from its modeling. “I don’t think that’s even possible based on the probabilities,” he said.

“It’s below the criterion. It doesn’t mean there’s no expected unserved energy. It just doesn’t exceed the one-day-in-10-years” standard, said RaeLynn Asah, MISO senior manager of regulatory and policy planning.

Plante argued the RTO can meet the loss-of-load criteria but still experience unserved energy. He said they are two separate concepts.

Asah clarified there was no significant unserved energy, not a complete lack of unserved energy.

MISO’s modeling does not factor in deliverability or transmission constraints.

Booth said it would behoove the RTO to consider transmission so it doesn’t rely on generation that’s situated in MISO South that might not be deliverable to the Midwest. He said its resource-adequate assumption is flawed without deliverability considerations.

Asah said MISO would consider deliverability when it sites its generation totals across the footprint. MISO’s Neil Shah added the method is in line with how the RTO conducts its loss-of-load expectation studies.

“How do you not consider whether these resources are actually deliverable?” Booth asked.

Shah said deliverability is handled in subsequent steps and said MISO doesn’t account for transmission constraints in its first step.

NEW ORLEANS — The MISO and SPP proposals to accelerate the interconnection of shovel-ready generation projects may share an acronym more widely associated with a certain global superstar, but it was intended that way.

The “ERAS” acronym, that is; not the wink to Taylor Swift and her record-setting Eras Tour.

“We both chose that name to reflect what it was intended to do … but the acronym stayed the same,” SPP’s Steve Purdy, technical director of engineering policy, said during an early session of the Gulf Coast Power Association’s 12th annual MISO-SPP Regional Conference Feb. 23-24.

SPP’s ERAS is a one-time study process conducted outside the regular generator interconnection study in about three to six months’ time. The grid operator’s state regulators must approve the projects selected by load-responsible entities.

At MISO, ERAS evaluates up to 15 projects per quarter, on a first-come-first-served basis, that are ready to move forward in addressing a resource need. The study is capped at 68 projects in three categories: 10 independent power producers, eight serving retail choice load and 50 load-serving entities.

Purdy said SPP staff began talking with their MISO counterparts and engaged in several brainstorming sessions.

“The question was, ‘What can we do that’s outside the box that would help us address this in a meaningful way?’” he said. “We got together with them and brainstormed those ideas and came up with a similar process. We knew that it was not going to be able to be exactly the same, but we thought if we could come to our stakeholders, our regulators and FERC with a process that is cohesive and largely the same, that will ease the process of acceptance and approval.”

Kari Valley, MISO’s senior director of state policy and strategy, said the interregional collaboration between the seams neighbors is “fundamental for our continued success.”

“We work together to make sure that each partner’s ERAS process works as planned. We made joint operating agreement changes that were accepted by FERC to ensure that timeline’s implementation,” she said. “I just remember … sitting around the table with the folks from SPP and issue spotting. The issues are the same across the footprints.”

“The early collaboration was key for us; the opportunity to work together and then to continue that as we both developed our processes was one of the keys to success in the process,” Purdy said. “We addressed the seams issues at the same time that we were developing this process, and then we went to our stakeholders and regulators and really engaged in a partnership with them to refine the product and tailor that solution to the unique needs of both SPP and MISO.”

Heavy Responsibilities for LREs

Golden Spread Electric Cooperative’s Mike Wise, the co-op’s senior vice president of regulatory and market strategy, spoke up for the little guys — the LREs also accountable for balancing reliability and affordability — following multiple discussions of the need to match the pace of change.

“I think everybody in here has probably novice to an expert level of knowledge about resource adequacy because it’s been the title of the topic of everything we’ve had to deal with in this industry for the last two, three years,” Wise said. “We’re responsible to come up with those resources and meet the requirements. The perfect storm is when SPP says, ‘Well, this is what we need, and you’ve got to do it.’ Well, we’re the ones that have to figure out how we’re going to comply and make this thing work.”

SPP wants “to move faster, where we as stakeholders are barely able to keep up,” Wise said. “And we think, ‘Hey, we’ve done a lot of things. We’ve created a lot of new acronyms,” he added, ticking off HILLGA (high impact large load generation assessment), HILLs (high impact large loads), CHILLs (conditional high impact large loads) and PDA (peak demand assessment).

“We have all these different resource advocacy terms, and it’s a challenge for us to be able to meet these requirements,” Wise said. “We’re balancing this problem between reliability and the big ‘A’ word, affordability. As a G&T co-op, we’re really focused on trying to make sure that the end-use consumers can afford this level of reliability and quality of service they’ve been able to receive over the last decades. It is a challenge.”

Google, KCC Collaborate on Tariff

Kansas Corporation Commissioner Andrew French and Google Energy Policy and Markets Lead Neka Goka, who worked together on a 2025 settlement agreement that created a large load power service rate plan, were reunited on the obligatory panel on data centers and a discussion on the disruptions they bring.

Under the Kansas rate plan, loads 75 MW or more of peak power consumption must take service for at least 12 years after an optional ramp-up period of up to five years. The loads must also pay a minimum monthly bill based on 80% of contract demand and pay for any transmission upgrades necessary to serve their facilities.

“I think we just worked together pretty closely in Kansas,” Goka said. Google broke ground on a $1 billion data center in 2024 and recently began construction on another facility near Kansas City.

“When you talk about speed to capacity of serving data center load growth, the underlying message there is ‘who’s going to pay for what and when?’” Goka said. “I think what we have viewed in our effort is that we believe that the utilities build up resources that can serve the system. Our view is we’re willing to pay for our part of the system plus a little bit more to recognize the fact that we’re getting utilities to move a little bit faster.”

French countered by reminding his audience that the grid is at its limit, and there’s no surplus generation sitting around. The system needs help, he said.

“One thing that does concern me is sort of an inefficient use of capital right now, in that data centers may be incentivized just because of the speed element to put inefficient generation on-site; to do things that aren’t really in the long-term public interest,” French said. “This is a real opportunity to have new payers come on the system and help build the grid of the future. We have a very aging grid, a grid that needs replacement, and it would be great for existing customers to have assistance to help renew and refurbish that grid.”

Seams Work for MISO, SPP

Although they had just formally met minutes before, MISO’s Tabitha Hernandez and SPP’s Yasser Bahbaz came off as old friends as they cheerfully engaged in a lighthearted discussion of the seams between the neighboring grid operators.

“A fun fact as I was prepping for this: Did you know that we have over 1,000 miles of seams between us?” said Bahbaz, SPP’s senior director of market development. “It’s the longest one in the country.”

“It’s quite busy, too,” responded Hernandez, director of operations management, balancing and interchange.

Indeed: During the brutal February 2021 winter storm, SPP imported as much as 7 GW from MISO and other neighbors, with as much as 4 GW flowing to MISO in the other direction through the grid operators’ regional directional transfer operations.

The two RTOs also collaborate on energy transfer settlements and with their market-to-market activities, where the non-monitoring RTO adjusts dispatch to ease congestion on binding flowgates.

“Why [do] seams work? From my perspective, seams work because we make it work,” Bahbaz said. “We invest a lot of time, a lot of relationship-building with MISO and other parties, to make sure that it works and it works with a common objective of reliability and efficiency for the whole electric system, not just each party individually.”

“Really, we want to make sure folks understand we are constantly in conversations about what is the best to do for the grid, right?” Hernandez said. “We do not operate in silence. We want to make sure that we are a good neighbor; that we are taking care of the assets we have and that our customers have, our members have; and we can make sure that we all keep our lights on on a day-to-day basis.”

Calpine’s Kruse Gets Award

The conference began Feb. 23 with about 350 attendees and GCPA’s presentation of the 2026 Moeller Sugg Impact Award to Calpine’s Brett Kruse for his “significant and demonstrable impact” within the MISO and SPP markets.

The award is named for the now-retired SPP CEO Barbara Sugg and MISO President and COO Clair Moeller. The award was first presented to Sugg and Moeller at the 2025 conference.

“This is a little overwhelming,” Kruse said from the podium, thanking GCPA Executive Director Barbara Clemenhagen and the organization’s staff. “It’s kind of neat because I’ve known Barbara and Clair for a long time, and as I look around the room, I see a lot of people that that went down the same track, either in SPP or MISO, with me.”

As vice president of market design for Calpine, now a business unit of Constellation Energy, Kruse has been responsible for the company’s interests in ISO-NE, NEPOOL, MISO, SPP, NYISO and PJM, and holds or held committee seats in each of the markets.

Kruse served on the SERC Reliability Board of Directors for 14 years, and he has been Calpine’s representative in ReliabilityFirst since its creation. He currently holds a seat on NERC’s Reliability and Security Technical Committee and is a member of the congressionally mandated NERC Interregional Transfer Capability Study Advisory Group.

He recalled joining Calpine in 2001 and, as the asset manager for the central desk, being asked by a “desk kid” what he knew about MISO and two other markets that eventually failed. SPP, already an RTO at the time, was about to begin work on its balancing market.

“We didn’t know anything [then],” Kruse said. “My thought at the end of the day is these are two very durable markets that work very well for the public and the end user.”

IESO officials have broadened the eligibility for hydropower projects in the ISO’s upcoming Long Lead-Time (LLT) procurement, agreeing to accept separately metered expansions as “new build” projects.

Such expansions will be eligible to participate in both the energy and capacity streams of the LLT procurement, which the ISO created for resources that require at least a five-year lead time.

ISO officials had said previously that such expansions would not be eligible for the LLT procurement. But IESO’s Danielle D’Souza told stakeholders Feb. 26 that it changed its position in response to stakeholder feedback that such expansions may require longer design and construction cycles and would be unable to compete against wind and solar projects in its long-term procurements. (See IESO Holds Firm on Hydro Exclusion, Reserve Price in Long Lead-time RFP.)

“What that means is that hydroelectric expansions that are separately metered will be eligible to participate, and this is consistent with the treatment of separately metered expansions under” the pending Long-Term 2 (LT2) procurement, D’Souza said. While the LT2 procurement is limited to resources that can go into operation within four years, the LLT resources will have up to eight years to go into operation.

Pending a final directive from the Ministry of Energy and Mines, IESO expects to offer “rated criteria” incentives to developers by reducing their “submitted” price to an “evaluated” price for comparison against competing offers.

Developers who commit to sourcing 75% of materials and construction services from Canadian suppliers would receive a 2% reduction in their “evaluated” price. The ISO requested feedback on whether the incentive would impact supply chain decisions and whether a 75% threshold is achievable.

Developers making energy proposals will receive up to a 5% reduction for Indigenous economic participation and up to an additional 5% for projects located on tribal lands.

In addition to those incentives, capacity projects will be eligible for up to an additional 5% reduction for facilities that can offer more than the minimum eight hours of continuous energy.

“All of that is pending the final [ministry] directive, but we have a good sense of where that’s going to land now,” IESO’s Ben Weir said.

Prime Agricultural Areas

Weir said IESO expects the ministry to eliminate rated criteria incentives for projects locating outside of Prime Agricultural Areas.

“I think part of the reason why government has been more comfortable in the LLT context to [remove rated criteria] is because of the technologies that are at play,” he said. “Hydroelectric — unless you can prove me wrong — isn’t going to be built on ag land. … And when we’re talking about the [long-duration energy storage] technologies, by and large, the acres taken per megawatt of capacity is a lot smaller … than when we’re talking about wind [or] solar projects.

“I don’t expect government to change tack on that for the LLT,” he added. “But for full transparency, we have not had that discussion with them.”

Assuming the ISO receives a final directive from the ministry in March, Weir said it should complete the request for proposals and contract documents by mid-April. That would enable an Oct. 1 deadline for proposal submissions, with contract awards targeted for March 30, 2027.

Feedback on the supply chain disclosure provisions is due March 5, and comments on the rest of the materials are due March 12 to engagement@ieso.ca.

NEW ORLEANS — The Gulf Coast Power Association’s MISO–SPP Regional Conference showcased the rush to add resources, and panelists mused on which new trends could take hold in resource expansion.

David Mindham, a senior director at EDP Renewables North America, said today’s characterization that a sudden, steep demand for electricity emerged from nowhere is intellectually dishonest. He said more generation than what has been developed was essential for years.

“We have systematically built the shortage into the system today … by poor planning decisions,” Mindham said during the Feb. 23-24 conference. RTO planning relies on the “most conservative set of assumptions you could ever make” and keeps the system chronically underbuilt, he argued.

Far from its intended cost effectiveness, the lack of proactive planning is squeezing customers financially, he said. “We’ve actually needed the generation for decades.”

Wisconsin Public Service Commissioner Marcus Hawkins mulled whether “speed is a premium product” for which generation developers should expect to pay.

“Speed should be the expectation,” Mindham responded, adding that MISO and SPP contain many inefficiencies. He said developers flock to ERCOT not merely to site projects in Texas but because the grid operator offers speedy interconnections.

“If you want two-day shipping, you have to sign up for Amazon Prime,” Hawkins retorted jokingly.

Travis Kavulla, head of policy at the Texas-based Base Power, which installs whole-home batteries for a subscription, suggested that RTOs try holding interconnection rights auctions. He said developers could bid on incremental capacity in auctions, similar to the Federal Communication Commission using competitive bidding to assign spectrum licenses. He said auctions would weed out any unserious large load developers.

“That solution is so obvious, but no one has pursued it with dynamism,” Kavulla said.

Beth Garza, a senior fellow at R Street Institute, said she still is waiting on the “too cheap to meter” nuclear generation that was promised in the 1950s. She said the industry might be at a tipping point where it is ready to embrace new technology and that small modular reactors could be the answer.

Energize Strategies’ Ted Thomas said he worries the industry has become too natural gas-heavy and that he plays scenarios in his head before going to bed in which gas costs spike. Resource planners adding copious amounts of gas-fired generation are doing so based on assumed capacity factors, he argued. He predicted that gas capacity factors will “flatten out” and expose which gas plants ultimately were necessary.

Thomas cited President John F. Kennedy’s famous saying, “A rising tide lifts all boats,” before noting Warren Buffett’s retort on economic vulnerabilities: “It’s only when the tide goes out that you learn who has been swimming naked.” He predicted that some new gas plants will in time “show that we’ve been swimming naked.”

Southern Renewable Energy Association Executive Director Simon Mahan said that adding more generation, particularly battery storage, and interregional transmission is crucial.

“If these extreme weather events are going to keep happening, we need to be better prepared. … People are going to get hosed when they get their bills next month,” Mahan predicted of the late January 2026 winter storm. Gas prices that shot to $7 to $8/MMBtu during the winter storm are a “straight pass-through” on bills, he said.

Those who can afford it are increasingly turning to home battery purchases. “Everyone is getting nervous that the system, today’s system, is inadequate,” Mahan said.

America’s Power CEO Michelle Bloodworth argued that the industry’s saving grace, as shown in NERC’s Long-Term Reliability Assessment, are the delays in planned coal plant retirements across 19 states. She said the postponements kept regions from going even redder in NERC’s assessment.

Bloodworth argued that coal plants can be modernized and cleaned up to run for another 30 years, with the help of the Department of Energy’s more than $500 million in funding. She said it’s going to take “time and sustained investment” to bring in new baseload power to replace coal.

Mahan said subsidizing coal plants should take place at state-level proceedings, not federally. He also said NERC’s LTRA has “significant deviations from reality,” noting that it ignored MISO’s expedited interconnection queue.

“There’s a disconnect between the visuals and the narrative that’s going on in that report,” Mahan said. He said coal lobbyists and environmental advocates can agree on the destination — a reliable, decarbonized grid — just not the timelines they envision to get there.

The Queues

Natasha Henderson, SPP’s senior director of grid asset utilization, said the 108 GW of nameplate capacity in her RTO’s queue is about twice its current load.

SPP also has 40 GW of signed interconnection agreements under its belt, the bulk which are slated to be online by 2030. But Henderson said the RTO forecasts its demand will be 93 to 100 GW by 2035. She likened the queue to “a bit like a bubblegum machine,” where it can be shaken and just a few gumballs pop out.

Of SPP’s 40 GW in generator interconnection agreements, only 7% represent thermal resources, Henderson said. Meanwhile, she said, SPP’s fast-track interconnection queue comprises 70% thermal generation. In its regular queue, SPP is seeing fewer standalone solar or storage projects and more hybrid formats.

Henderson said it’s not a controversial statement that the current transmission infrastructure won’t be able to handle the demand that’s being planned. “The longer we wait to build, the less load we’re going to connect.”

MISO’s queue, on the other hand, contains 190 GW, down from a peak of more than 300 GW in 2025.

“The interconnection queue has been one of the most visible challenges for MISO,” said Robert Kuzman, executive director of external affairs.

Kuzman said MISO remains challenged by 70 GW of generation projects that have signed interconnection agreements but remain unbuilt or unfinished. He said developers behind those projects should answer hard questions as to whether their projects are viable and withdraw them if not. That way, he said, transmission capacity might be freed up for other generation proposals.

The queue has shrunk rapidly on the Trump administration’s announcement that it would phase out renewable generation tax incentives, Kuzman said. He added that although MISO’s expedited queue comprises mostly gas generation, proposed battery storage is also taking up a small chunk.

Kuzman said MISO likely could have benefited from four-hour battery storage during Winter Storm Fern in late January. The RTO might not have had to call up load-modifying resources if it had a larger storage fleet, he said.

“It’s something that’s coming in MISO. There’s definitely a place for it as we continue to add as much solar as we are,” he said.

Henderson agreed that storage would be useful at SPP, though its market ruleset isn’t fleshed out. She said the resource type could help with ramping needs and likely could bridge a gap in intermediate planning needs.

BOULDER, Colo. — The challenges of meeting accelerating load growth pervaded discussions at EMPOWER 26, Yes Energy’s annual summit, where speakers discussed the changing federal regulatory paradigm, long-term market trends, demand flexibility and how to responsibly interconnect hyperscale data centers.

Data center development is the largest driver of forecast load growth across much of the country, though electrification and manufacturing growth also contribute to the rising demand, multiple speakers noted. More than 400 industry professionals attended the conference Feb. 25-27 in Boulder.

Building adequate supply to meet this demand is “one of the big challenges that we face,” said Jesse Jenkins, associate professor of energy systems engineering and policy at Princeton University. In his keynote address, he cited Grid Strategies’ forecast for 5.7% annual growth in U.S. power demand over the next five years.

Significant uncertainty remains regarding which sources of supply will arise to meet this demand and whether these sources will align with decarbonization efforts.

To date, much of the focus from data center developers has centered around fossil resources, with 49 GW of gas-fired generation added to interconnection queues across the country in 2025, Jenkins said. With gas turbine supply chains constrained, developers have turned to dirtier, less efficient gas-fired technologies, including converted jet engines. Coal also saw a resurgence in 2025, in part because of load growth from data centers.

“Gas will continue to play an important role in meeting incremental demand growth,” said Eric Brooks, manager of Americas gas pricing at S&P Global Energy. He said he expects new gas demand from new LNG exports and data centers to cause “slightly more elevated” gas prices over the next five years.

Dan Spangler, senior director of analytics at Natural Gas Intelligence, said the trajectory of data center development could have a significant impact on the need for gas generation in the longer term.

“If we get a lot of demand coming on and renewables and batteries can’t meet it, then gas is a natural place to step in to meet that,” he said. “But similarly, if data centers turn out to be a bust and demand is way lower than what people are expecting, then I would expect renewables and batteries to potentially significantly eat into gas’s share, possibly sooner rather than later.”

Beyond the direct climate and health impacts, reliance on polluting resources to meet load growth could undermine data centers’ social license, Jenkins said.

“Growing public opposition is becoming a key impediment to development,” he noted, citing an analysis that found 25 U.S. data centers totaling at least 4.7 GW were canceled in 2025 following local opposition.

But while renewables and energy storage make up the bulk of new capacity coming online, elimination of the federal tax credits has created uncertainty for the renewable projects unable to access the expiring incentives. The Trump administration’s assault on domestic offshore wind also has created major long-term questions about the future of this industry in the U.S.

Judd Rogers, vice president of new project development at Scout Clean Energy, said rising demand coupled with the shift in federal energy policy has created a complex mix of headwinds and tailwinds for clean energy developers.

While the “demand for our product is incredible,” he said, “the current administration is calling out our industry as being stupid or dumb or causing cancer. It’s obviously incredibly challenging, and the roadblocks that they’ve been able to put up have been incredibly challenging to navigate.”

Demand Flexibility

Several presenters stressed the importance of demand response and flexibility for limiting infrastructure costs and peaking needs.

While data centers tend to have flat load profiles, Jenkins expressed optimism about technological advancements enabling demand flexibility within the facilities. He highlighted a study recently published in Nature Energy which found the potential for 25% demand flexibility for an AI data center in Arizona using software that enables the designation of computing tasks by priority.

Coupled with on-site battery storage, this represents a “truly scalable solution” to minimize the need for major transmission upgrades, he said.

Former FERC Chair Jon Wellinghoff, now the chief regulatory officer at Voltus, said demand response participating in the wholesale markets can play an important role in meeting near-term supply challenges.

“You need load flexibility if you’re going to get these data centers in place quickly,” he said.

PJM’s initial proposal for the backstop auction would not allow load management to participate. But Wellinghoff said it is not clear that the governors and the White House intended to exclude demand response resources.

“From a regulatory standpoint, FERC in orders 719 and 745 clearly said that demand response and load flexibility should be comparable to generation [and] should be included in the auctions,” he said.

Referencing a recently announced deal between the U.S. and Japan over a 9.2-GW gas facility in Ohio, he said the auction should not prioritize foreign-owned generation plants over demand response capabilities that can be provided by American businesses.

Transmission Expansion

Speakers also emphasized the role of transmission expansion in meeting supply needs.

“We’re trying to figure out how we’re going to serve all of this load we’re seeing,” said Andrew Reimers, deputy director of the ERCOT Independent Market Monitor, Potomac Economics. “One way we can do that is we can approve a bunch of transmission projects that will make it to where the effective load carrying capacity of all this generation is high. We can do that now with generation that’s already in the ground rather than waiting and hoping that a new combined cycle gets built in that load pocket.”

ERCOT is betting big on transmission expansion, pursuing the development of a series of 765-kV lines throughout the state to help meet demand growth. Its Strategic Transmission Expansion Plan includes 2,468 miles of new 765-kV lines and has a total estimated cost of about $33 billion.

Jack Farley, chief commercial officer at Grid United, laid out an even broader vision for expanded interregional transmission connectivity across regions throughout the U.S.

He highlighted the potential economic benefits of the company’s Three Corners Connector transmission project to connect Pueblo, Colo., and the SPP system in Oklahoma.

The line should be in service by late 2030, he said. Without transmission connection, Colorado tends to be “sitting on 30% of its reserves … when SPP needs it most,” he said. “When SPP is in its top 3% of net load hours over the last five years … there are about 3 to 4 GW of stranded reserve capacity in Colorado.”

When connected, “this creates capacity, and this can be accredited just like wind and solar with the standard models,” he said.

Projects like the Three Corners Connector “are gigawatt-plus capacity additions that are ideal for data centers and large flat loads because it’s cheaper than natural gas turbines,” he said.

RTO Insider is a wholly owned subsidiary of Yes Energy.

According to the Business Council for Sustainable Energy’s 2026 Factbook, U.S. consumers spent “slightly less” on electricity in 2025 than they did in 2024.

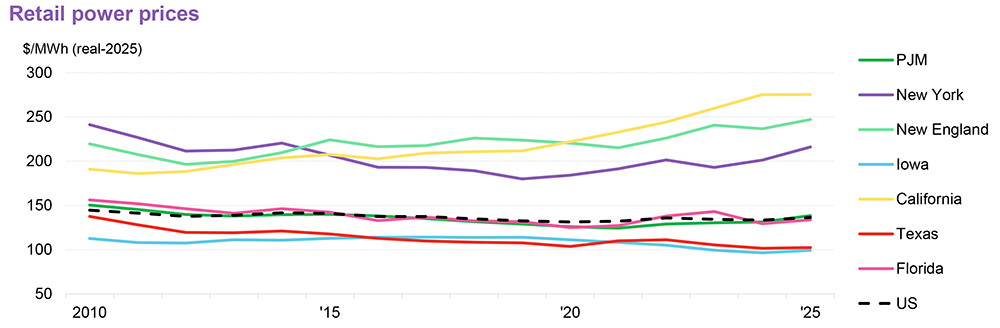

The extent of that “slightly less” is not calibrated in dollars and cents, but you can see in the charts above ─ from BloombergNEF, which compiles the annual report ─ that total energy costs, which include gasoline, and electricity costs are wiggling down, though not by much.

Other charts in the factbook show that while wholesale and retail electricity prices have gone up and down over the past 15 years, they are not appreciably higher today than they were in 2010 ─ with some notable exceptions. After 2021’s dramatic winter storm spike, wholesale prices dropped in Texas, while retail prices are up in New England and California (though BNEF sees a 2025 rate plateau in California).

Retail power prices: How high or low can they go? | BloombergNEF

The factbook and its charts provide the kind of widely quoted data points often used to try to persuade consumers the U.S. electric power industry is working hard to keep their utility bills affordable.

But when I first saw these charts at an advance press briefing for the factbook Feb. 17, what quickly came to mind were the panel discussions I had heard on affordability and transparency at the National Association of Regulatory Utility Commissioners’ Winter Policy Summit in D.C. the week before.

Affordability can be defined in many ways, depending on context. Affordability in the abstract ─ what a utility or regulator thinks of as affordable ─ may have little if any relationship to affordability as experienced day to day by consumers looking at electric bills that keep going up.

David Springe, executive director of the National Association of State Utility Consumer Advocates, talked about his 86-year-old mother, who had upgraded her HVAC system to improve efficiency at the home she has lived in for decades but was still seeing higher electric bills.

“There’s a level of frustration going on out there right now with customers not feeling like they can control their budget and control their usage, and no matter what it is that they do, their bill keeps going up,” Springe said during the panel on affordability that closed the conference. “This is a conversation we seem to have every year at NARUC. … This interaction with customers and giving customers tools and power and ownership is something we always struggle with.”

The pressing issue of demand growth ─ primarily from data centers ─ has only heightened consumers’ and consumer advocates’ anxieties, he said.

“The scary part to me [is that] the answer seems to be that … we’re going to build our way out — spend a lot of money building our way out of this problem — and I’ll tell you that does not give the consumer advocate community the warm and fuzzies.”

Springe pointed to the October 2025 forecast from the Edison Electric Institute, the trade association for investor-owned utilities, that its members will spend $1.1 trillion in capital investments over the next five years ─ a figure that could already be out of date.

For example, in its most recent earnings call Feb. 10, Duke Energy raised its projected five-year capital expense plan 18.4%, from $87 billion for 2025-2029 to $103 billion for 2026-2030.

“Those costs are going to end up in rates,” he said.

‘Growth Must Pay for Growth’

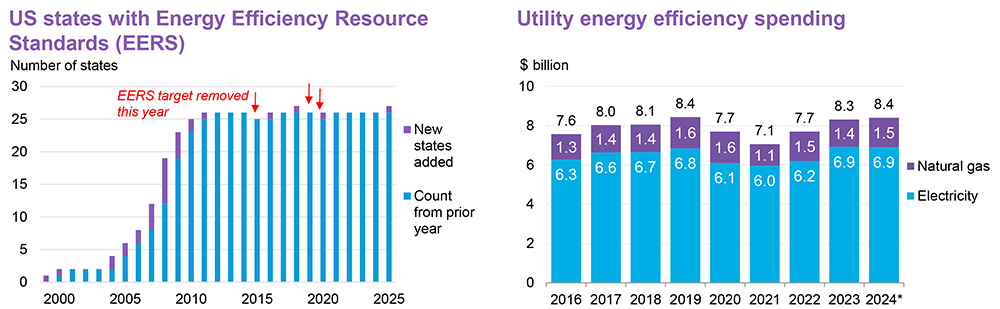

Energy efficiency and better customer communication are the perennial low-hanging fruit ─ and as Springe noted, ongoing pain points ─ of the industry’s efforts to bridge the gap between different definitions and experiences of affordability.

According to the BCSE factbook, utility spending on efficiency programs ─ for electric and natural gas companies ─ has never exceeded $8.4 billion per year over the past decade, or less than 1% of the $1.1 trillion or more the IOUs will invest in new generation and the grid over the next five years.

Efficiency: The low-hanging but underfunded fruit of affordability. | BloombergNEF

Policy signals also are mixed. Currently, 27 states and D.C. have some kind of energy efficiency standard, setting targets for utilities to reduce electricity consumption with efficiency measures. Arizona is expected to repeal and revise its efficiency rules, despite broad public opposition.

Springe cautioned that communication promoting efficiency must be ongoing but balanced. If bombarded with messages about energy conservation, customers could tune out and not react to cut consumption in real emergencies, he said.

Matthew Ketschke, president of Con Edison of New York, agreed that while “it’s very important to constantly [engage] our customers on the value of energy efficiency, I do have concerns about going out right before either a high-load day for heat or cold and sending [an appeal to conserve]. … It gives the impression that we, collectively as the people responsible for their energy delivery systems, did not do our jobs in making sure that we have enough capacity for safe, reliable delivery of energy. … You kind of want to save that messaging for when … there’s no room for failure.”

If efficiency can be a hard sell, the challenge is even greater for convincing consumers of the potential benefits of building new generation and power lines to meet demand growth from data centers, calling for levels of transparency that are not exactly utilities’ or regulators’ strong suit.

The new mantra at the state and federal level is that “growth needs to pay for growth,” according to speakers at a separate panel on demand growth and large loads.

“Whether it’s a regulated or a deregulated area, you need to be trying to develop policies where new large loads are accompanied by new large generation, and you grow the system in a balanced way,” said Nick Elliot, senior policy adviser for the White House’s National Energy Dominance Council.

Several reports have provided case studies in which adding new generation for large loads has helped mitigate rate increases by spreading the fixed system costs of utility bills to a larger customer base. The caveat is that “there are obviously a lot of different models for connecting these loads … [which] may not be replicable and scalable in every scenario,” said Lakin Garth, director of emerging technologies for the Smart Electric Power Alliance.

Trump’s Election Year Ploy

How these ideas play out at the state level is very much a moving target. A map and database compiled by SEPA and the NC Clean Energy Technology Center show that individual states, their regulators, utilities and high-tech customers are trying out different approaches.

According to Christopher Ayers, executive director of public staff and consumer advocate for the North Carolina Utilities Commission, it is too early to say if the various rate structures or contracts being proposed will consistently or substantially lower rates.

Transparency is critical, so the public can understand any proposed rate structures or other regulations on large loads, Ayers said.

Jose Esparza, senior vice president for public policy at Arizona Public Service, pitched for his company’s model, which uses a formula to allocate costs to large load customers so they pay 45% of the utility’s requested rate increase, compared to 14% for residential customers. APS is also providing “special contracts” for data centers looking for fast-track interconnection and service.

“What we’re offering is what we’re calling a subscription rate, where you’ll take a portfolio of resources,” he said. “The customer will have to put up a certain amount of collateral, agree to pay a 20-year or 15-year agreement, to pay down and appreciate those costs as much as possible.”

APS is facing opposition to its special contracts from Arizona Attorney General Kris Mayes, a former utility commissioner who argues they lack transparency and public oversight.

Such calls for transparency could open a new front in industry and regulatory debates, where definitions are again varied and subjective. For example, APS customers might not see a 14% rate increase as particularly affordable.

“We can say growth pays for growth, [but consumers] are not really understanding that because there is a national narrative going around on both sides of the aisle that’s convincing folks that that’s not really happening,” Esparza said. “Utilities and large load customers have to do a better job of partnering with their regulators and our customers to ensure them that we are taking this seriously.”

Briana Kobor, head of energy market innovation for Google, agreed that “transparency is key. We are screaming from the rooftops that we are here to pay our fair share of costs. Help us to show that to the public and to the regulatory ecosystem. … The math is different in every single jurisdiction. Maybe [the data center share] is 70%; maybe it’s 80%. Maybe it’s 12 years; maybe it’s 15 years. Behind that minimum revenue guarantee is a math problem, and it should be compared with what your rate is and what your marginal costs are, what you are going to be investing in, and it’s a conversation that we’re going to be having for years and years to come.”

All of which makes President Donald Trump’s State of the Union announcement of a “Ratepayer Protection Pledge,” committing the AI giants to providing their own data center power, little more than an election-year ploy aimed at co-opting and taking credit for the hard, innovative work being done on the ground.

Electricity Value vs. Cost

And, as the consumer advocates are saying, it is too early to gauge the impact of the state-level initiatives, let alone a vague federal effort.

“Once there is a large load tariff in place, the load projections kind of drop,” North Carolina’s Ayers said. “It’s because now you’re able to quantify impact; now you’re going to have to start putting money where your proposal is … and that has an inherent heightening effect in terms of our need to sharpen our pencils and get to that number. … There’s also a perception amongst the consumer advocate community that large load is still running around from jurisdiction to jurisdiction, trying to find the best deal.”

The bottom line is that, at least for the near term, electric bills are going up, and definitions and perceptions of affordability will have to evolve.

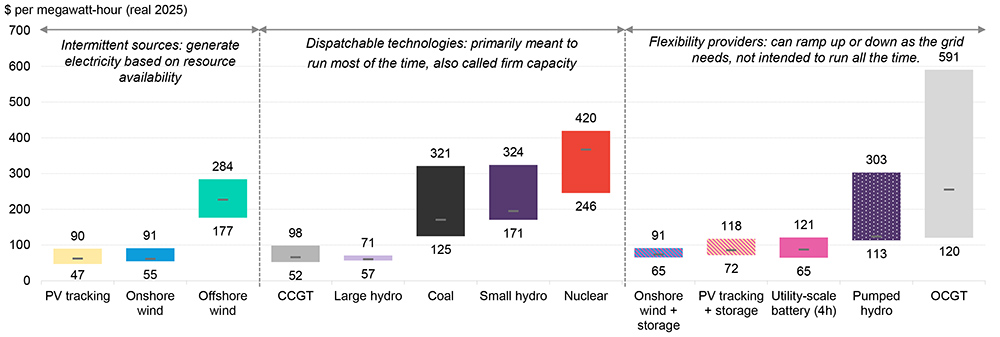

U.S. LCOEs: Again, what’s high and what’s low? | BloombergNEF

Morgan Scott, vice president of global partnerships and outreach at the Electric Power Research Institute, said that as the cost of electricity goes up, so does its value, which should be a key theme in industry messaging to customers.

The bring-your-own-power imperative for hyperscalers may be a first step, but it raises some tricky questions.

Ayers has a major concern about long-term risk and costs shifting back to consumers. If we’re building 40-year assets ─ like natural gas or nuclear plants ─ what happens after a data center’s 15- or 20-year contract runs out, he asked. Will consumers be left to pick up the tab for the remaining 20-plus years?

That’s a rabbit hole the industry has yet to go down, he said.

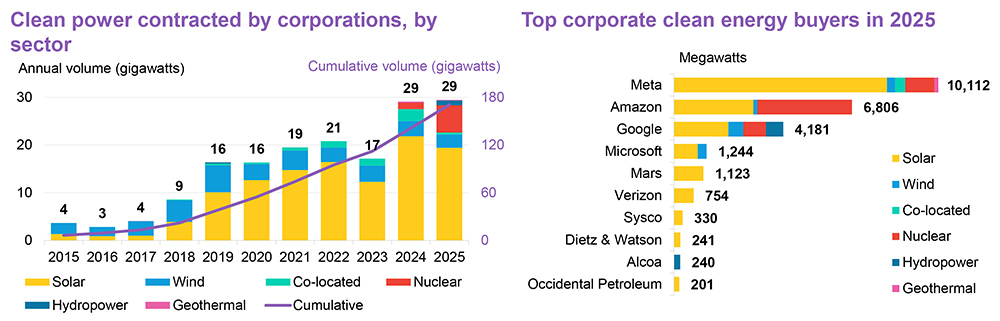

Look who’s buying clean energy | BloombergNEF

The way forward for both affordability and transparency will involve figuring out what combination of technologies ─ generation, transmission and flexible demand response ─ are going to deliver the highest value and reliability for consumers, while raising rates the least.

While it is by no means the only or most reliable measure of affordability, the levelized cost of electricity remains a useful marker. On that basis, the BCSE factbook shows that renewables remain the most affordable, which is likely at least one consideration for the corporations and investors still betting heavily on them.

Not surprisingly, Meta, Amazon, Google and Microsoft are leading the pack. Corporations are all about affordability.