New nuclear generation holds promise for the U.S. and its energy sector if its challenges can be overcome, panelists said during a Resources for the Future webinar.

The consensus was that regulatory, financial and policy support are important components of the process by which this can happen.

RFF President Billy Pizer opened the Oct. 21 conversation with John Williams, senior vice president of technical services at Southern Nuclear, which developed Plant Vogtle Units 3 and 4, the only U.S. nuclear construction project to reach commercial operation in decades.

With its delays and cost overruns, Vogtle illustrates the problems facing first-of-a-kind projects, Williams said, but also the benefits that can accrue for second-of-a-kind projects.

The project was plagued with unforeseeable problems such as the Fukushima disaster, the bankruptcy of its contractor and the COVID pandemic, Williams said, but there also were the predictable first-mover difficulties, particularly with Unit 3.

“We had challenges as we were building a new supply chain for a new technology,” he said. “And then workforce — it had been 30 years since we had built a new nuclear plant from scratch in the United States. So our workforce, we didn’t have that muscle memory that they have in other parts of the world, where they have been building on a more regular frequency.”

Unit 4 was in some ways a second mover, and the effect showed, Williams said: It cost nearly 20% less than Unit 3 to build, and commissioning took half as long.

How many more Vogtles would it take, Pizer asked, to reach that “Nth of a kind” balance where things can move fast and predictably, without cost overruns and delays?

Six to 10, Williams estimated.

The momentum has flagged, however. Heavy construction was completed at Vogtle in mid-2023, Williams said, and a workforce now experienced at building nuclear reactor complexes went its separate ways to build data centers and auto factories.

John Williams, Southern Nuclear | Resources for the Future

Williams said Vogtle 3 and 4 cost about $11,000 per kilowatt of nameplate capacity in present-day dollars, but if the next several projects were built in close succession around the same Westinghouse AP1000 reactor, the cost would gradually drop.

“By the time you come down that Nth of a kind curve, now you’re looking at $6,000 to $7,000 a kilowatt,” he said. “By taking a pause, we will absolutely have to do some relearning. The sooner we get started, the better off we’ll be.”

Karen Palmer, senior fellow in RFF’s electric power program, asked when all this nuclear generating capacity in the planning stages might start sending power onto the grid.

Matt Bowen, senior research scholar at Columbia University’s School of International and Public Affairs, ran through a partial list of the many development efforts vying for market leadership positions and said: “I sort of think the better question is, who if any of these entities is going to build something at an acceptable cost that can then be deployed a bunch of times in the 2030s and 2040s to make a sizable contribution to the U.S. energy portfolio, let’s say over 50 gigawatts.

Matt Bowen, Center on Global Energy Policy, Columbia University School of International and Public Affairs | Resources for the Future

“It’s a little too early to say how these are all going to turn out.”

Bowen said he is confident, however, that future gigawatt-scale projects could proceed with fewer delays and cost overruns than the two recent U.S. examples, Vogtle and the canceled V.C. Summer.

Alan Ahn, deputy director for nuclear at Third Way, said small modular reactors are promising because of their smaller footprint, which is expected to lower cost and increase versatility. Lower cost could facilitate financing , which has been a challenge for the nuclear industry.

“I think the reality in terms of hurdles going forward is that we’re still at a first-of-kind stage with these technologies. Matt went over some of those issues at length,” Ahn said. “There’s definitely light at the end of the tunnel. I think the challenge now is maximizing the potential of these technologies by building them at scale, maturing supply chain and reaching commercial maturity.”

Mixing into this crowded environment are a number of states promoting nuclear development, such as New York, whose governor has ordered the New York Power Authority to develop at least a gigawatt of nuclear capacity.

Alan Ahn, Third Way | Resources for the Future

Erich Scherer, director of strategy at the New York State Energy Research and Development Authority, said NYSERDA is not exactly new to the sector, having evolved from New York’s atomic agency.

But that was 50 years ago, and nuclear power has evolved greatly since then.

“So learning lessons is very much at the top of mind, both in terms of learning at the project level, but also in terms of learning from best practice, policy experience,” he said. “I’m also going to recognize that, I think, as a reality check, [there] just aren’t that many lessons to learn yet.”

Vogtle is a treasure trove of lessons, Scherer said, but it is an exception: Only a few of the many other reactor designs and business models being developed have even begun construction, and only a few states have put forth a comprehensive policy strategy.

New York is very aware of the risks involved in being a first- or second-mover, he said. “What’s really important in our mind is the possibility of cooperation between states, and so as we develop our master plan, we are also very much conscious that that’s not an effort in isolation. And New York state is part of initiative called the First Mover Initiative together with 10 other states.”

Erich Scherer, New York State Energy Research and Development Authority | Resources for the Future

This presents the chance to build a multistate order book and a pipeline that spreads the risks more broadly, Scherer said.

President Donald Trump, meanwhile, is roiling the regulatory environment in which all this would take place, demanding faster approvals and streamlined oversight.

Bowen said a lot of regulations are outdated and ripe for efficiency reviews, and there are opportunities to responsibly speed the process. But the Nuclear Regulatory Commission is being blamed unfairly for so few new reactors coming online in the past 30 years, he said.

Ahn addressed another challenge: the fuel supply chain. The U.S. gets its uranium from mines in other countries, he said, and while they can ramp up production, “I think the real challenge and bottleneck is with uranium conversion and enrichment, where producers need to invest in and execute expansions to their industrial capacity.

“In and of itself, that dependency on foreign fuel supply chains is not an insurmountable issue. We’ve operated our nuclear fleet on fuel converted and enriched overseas for very long time.”

The potential problem is that many other nations want to ramp up nuclear power generation, he said, setting up a strain on the supply chain, and that a significant share of the supply chain is still controlled by a potentially uncooperative country: Russia.

“I think particularly on nuclear fuel, there is need for coordinated, cooperative, international actions between the U.S. and its allies and partners,” Ahn said.

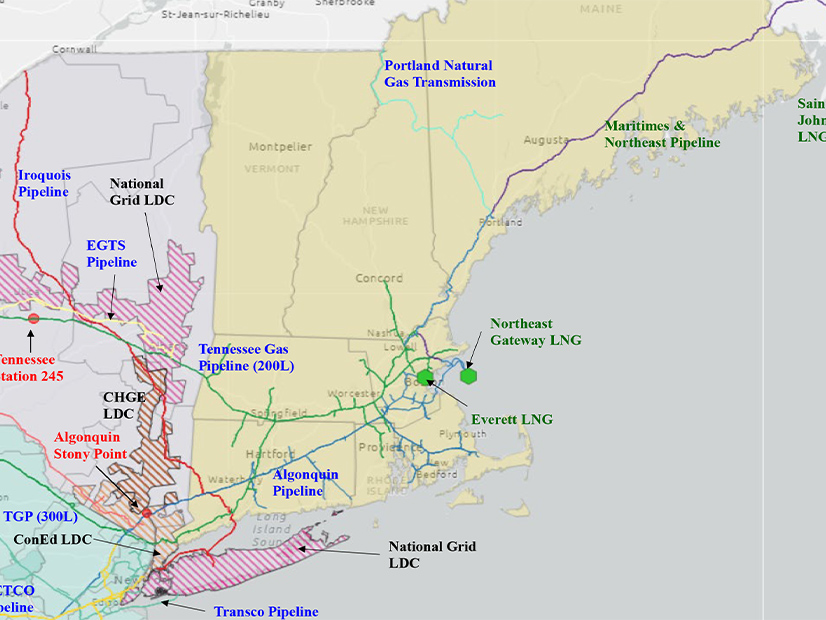

A relatively small project aiming to increase gas pipeline capacity into New England is raising larger underlying questions about how the region will balance gas reliability and affordability with longer-term efforts to transition away from natural gas.

Enbridge’s proposed expansion of its Algonquin pipeline, announced in September, has an estimated cost of $300 million and would increase the pipeline’s capacity into the region by about 2.5%. The company aims to complete the project in 2029.

Algonquin has announced it has reached agreements with seven utilities for the added capacity, including Rhode Island Energy and subsidiaries of Eversource Energy, which submitted a pair of 10-year supply delivery contracts associated with the project to the Massachusetts Department of Public Utilities in September.

Eversource said the contracts are needed to “address a reliability risk related to operational changes” instituted by Algonquin in 2019 reducing flexibility in nominations that previously allowed the company to nominate more than their contracted delivery entitlements in certain areas during cold-weather periods.

The company also said the added capacity would eliminate its “need to extend the G-Lateral supply portion” of its contracts with the Everett Marine Terminal (EMT), a major LNG import facility located north of Boston and owned by Constellation Energy.

By replacing LNG supply with pipeline gas, the project would reduce total gas costs for customers of two subsidiaries by about 5% and 1%, the company said.

“Without the proposed agreement, [Eversource] and its customers risk exposure to inadequate and unreliable supply and high city-gate pricing during peak days for customers served by Algonquin’s G-System, and would need [to] enter into negotiations with Constellation … for gas supplies to serve the G-Lateral from EMT after 2030,” Eversource argued.

However, environmental nonprofits argue the Algonquin expansion project would not eliminate the region’s overall need for the Everett terminal and instead likely would shift its costs to other customers.

In Eversource’s filing, the company appears to acknowledge the Algonquin expansion would not eliminate the region’s reliance on Everett, writing that the agreement would “not resolve regional dependence on natural gas from peaking resources” and adding that the terminal “provides a unique and critical energy resource in New England.”

In joint comments submitted earlier in October, the Acadia Center and the Conservation Law Foundation (CLF) wrote that the DPU must consider how the contracts “will impact not only Eversource customers, but also other gas customers, including National Grid and Unitil, whose contracts with Constellation mirror [Eversource’s].”

The Role of Everett

Until spring 2024, Everett’s main customer was Mystic Generating Station, a 1,413-MW, Constellation-owned combined cycle plant located nearby.

In the months leading up to Mystic’s retirement, local distribution companies owned by National Grid, Eversource and Unitil reached agreements with Constellation to keep Everett open through 2030. The contracts were necessary to provide adequate supply and preserve system reliability, the utilities wrote (DPU 24-25-B, et al.). (See Massachusetts DPU Approves Everett LNG Contracts.)

Everett “is ideally located in the heart of the market” at the back end of the Tennessee and Algonquin pipelines, Richard Levitan, president of the energy consulting firm Levitan & Associates, explained in an interview with RTO Insider.

Levitan stressed the importance of local deliverability to the system. LNG from Everett and Repsol’s Saint John LNG terminal in New Brunswick provides the “oomph to energize the network of pipelines serving gas utilities and generators in New England during cold snaps or some type of outage contingency along the mainlines serving New England,” he said.

He added that Everett “is the primary hub of truck-transported LNG to refill the dozens of satellite LNG tanks in New England that bolster pressure behind the pipeline citygates,” a role that cannot be replicated by the Saint John terminal.

Levitan noted that the Algonquin expansion project “is small in relation to the daily output” of both the Everett and Saint John facilities when the terminals are performing. He emphasized that, unlike conventional forward-haul service from the Gulf Coast or Marcellus Shale, LNG facilities provide operational and scheduling flexibility by enabling injections into the back end of the gas systems.

“When these import facilities are dispatching during cold weather events, it’s beneficial to the bulk electric generation market, and also to the LDCs, who generally look to supplement their pressures via displacement services when there are harsh operating conditions,” he said.

While utilities and gas generators rely on Everett to add supply downstream of New England’s gas constraint during peak periods and to provide backup supply during pipeline outages, the facility again faces an uncertain future after its contracts with the utilities expire in 2030.

The contracts are costly for ratepayers; Eversource estimated in 2024 they would increase rates by 5 to 7% for customers of one subsidiary and 2 to 3% for customers of another. Long-term reliance on Everett also likely would run contrary to Massachusetts’ longer-term efforts to move away from natural gas to reach net-zero emissions by 2050.

When approving the contracts, the DPU required the gas companies to “make significant strides to reduce or eliminate their reliance on EMT in the near-term” and directed them to “fully investigate all possible alternatives to EMT … including energy efficiency, strategic electrification and networked geothermal projects and, to the extent feasible, to coordinate their planning efforts.”

The order also required annual reports about the utilities’ efforts to reduce reliance on the facility, and in fall 2024, the Massachusetts Office of Energy Transformation established a working group focused on moving away from Everett.

Who Pays?

While the pace and trajectory of the gas transition in Massachusetts likely will determine the long-term demand for existing and new gas infrastructure, the fate of Everett, as well as the fate of gas pipeline expansion projects into the region, may be defined in large part by questions about funding.

The Algonquin expansion project essentially is a significantly scaled back version of Enbridge’s previously introduced “Project Maple,” which proposed to increase Algonquin’s capacity by up to 250,000 Dth/d at the eastern end of the pipeline. (See Enbridge Announces Project to Increase Northeast Pipeline Capacity.)

The smaller size of the updated 75,000 Dth/d expansion project appears to reflect the challenges of finding long-term customers for the increased capacity.

“Following the conclusion of the Project Maple open season in November of 2023, we decided to right-size Project Maple to better meet our customers’ specific needs, with a smart, targeted enhancement,” Enbridge spokesperson Melissa Sherburne said in a statement.

While New England relies heavily on gas generation, which hit a record high in 2024, generators’ access to gas is constrained during cold weather when heating demand is high. (See New England Gas Generation Hit a Record High in 2024.) Generators historically have been reluctant to take on long-term gas contracts, largely because of the financial risks associated with assuming these commitments.

Electric ratepayers also appear unlikely to finance new infrastructure; a 2016 ruling by the Massachusetts Supreme Judicial Court prohibits charging electric customers for the costs of new pipelines.

Meanwhile, residential, commercial and industrial gas demand has been relatively stagnant in recent years, and, seeking to decarbonize, Massachusetts lawmakers and regulators have taken significant steps to slow the expansion of the system and push gas customers to electrify. (See Outgoing Mass. DPU Chair Van Nostrand Discusses Gas Transition.)

“As far as who would pay [for Everett] in 2030 if Eversource is not a contracted party, it would have to be other LDCs, conceivably generators if we see the evolution of price signals under accreditation taking form, and marketers,” Levitan said.

As ISO-NE overhauls how it accredits resources in the capacity market, the RTO is poised to increase incentives for resources to procure firm fuel. However, the extent to which this will cause generators to enter long-term firm contracts is unclear.

In ISO-NE’s Capacity Auction Reform project to date, “we’re not seeing the evolution of accreditation principles that will clearly induce the generators to line up firm rights, so I don’t think at this moment in time we can reasonably expect the generators as a cohort group in New England to foot the bill for a major new pipeline push,” Levitan said.

Everett’s funding challenges mirror the challenges faced by any large pipeline project into the region, which are complicated by the state’s push to decarbonize.

Interstate pipelines serving eastern New York (2022) | S&P Global

Climate and consumer advocates have argued that Massachusetts must be careful not to make long-term investments in the gas system that end up becoming stranded assets. Some advocates see the 10-year duration of Eversource’s proposed Algonquin expansion contracts as reflecting uncertainty about long-term gas demand on the distribution system.

Joe LaRusso, senior advocate at the Acadia Center, said he’s skeptical gas utilities will experience enough new demand to support a “a substantial increase in gas capacity into the region.” He added that pipeline companies looking to build major new projects “can’t find the off-takers for this stuff; they can’t get it built.”

Acadia and CLF’s comments on Eversource’s contracts with Enbridge focus on Eversource’s underlying assumptions about its forecasted gas demand between 2029 and 2039. The groups highlight data from the U.S. Energy Information Administration indicating that overall residential, commercial and industrial gas demand in Massachusetts declined between 2019 and 2024.

They wrote that Eversource has provided “no basis to determine what their gas requirement will be over the term of the proposed contracts,” nor data on how “declines in statewide gas consumption in those sectors might ultimately influence either their overall consumption or their design day supply.”

In Eversource’s initial petition, the company wrote it “has not identified other viable alternatives to the proposed agreement,” adding that “the pace, scale and scope of energy efficiency and electrification would be insufficient to address the load requirements for the G-Lateral.”

Decarbonization Challenges

As utilities and regulators work to ensure the reliability of the state’s gas system, an inherent tension exists between investments to bolster the system and efforts to decarbonize.

While the gas industry frequently points to the reduction in carbon dioxide emissions associated with burning natural gas instead of coal or oil, methane is a key driver of manmade climate change and has particularly severe warming effects when evaluated over a more immediate time frame.

In a landmark order in late 2023, the DPU ruled that the decarbonization of the state’s gas system should center around electrification and emphasized the need for a managed transition away from gas and gas infrastructure (DPU 20-80-B). (See Massachusetts Moves to Limit New Gas Infrastructure.)

The state remains in the early stages of implementing this new regulatory framework, and in recent months, utilities and climate advocates have clashed over the LDCs’ legal obligation to serve customers, and whether the utilities could require customers to give up their gas service when decommissioning a section of pipe.

If successful, the electrification push would drive a substantial increase in power demand, which could cause continued growth or reliance on gas generation. While there is almost no proposed new gas generation in the ISO-NE queue, the challenges experienced in the offshore wind industry create significant questions about how the region will meet this growing demand.

“The demise, temporary or not, of offshore wind bodes poorly for certain environmental goals to be achieved in the early and mid-2030s if electrification gets the kind of traction that regional policymakers envision,” Levitan said. “There could be much more work burden on the existing thermal fleet to accommodate a pathway that is all about switching over from a summer to winter peak because of electrification.”

But for grassroots climate activists in Massachusetts, any efforts to expand natural gas infrastructure into the state are a step in the wrong direction.

“The answer is not, and never has been, keeping on with the gas system,” said Cathy Kristofferson, a longtime environmental activist in the state who co-founded the Massachusetts Pipe Line Awareness Network. “Everyone’s trying to figure out the affordability angle of it all, and for us, adding a bunch more steel in the ground is never affordable.”

Rosemary Wessel, an activist with the Berkshire Environmental Action Team, said Enbridge’s recent Algonquin proposal appears to be part of a strategy focused on incremental expansions to increase gas capacity into the region.

At an industry conference in September, Mike Dirrane, director of Northeast marketing at Enbridge, speculated that there may be an additional project after the current Algonquin expansion effort “to meet additional needs further down the road.” (See Gas Industry Sees Political Opportunity in New England.)

“They’re segmenting a larger expansion into small projects,” Wessel said. “We should not be serving that by approving contracts for more gas.”

Following a recent announcement that it plans to withdraw from the Western Resource Adequacy Program, NV Energy said it is discussing a potential new resource adequacy program with other participants in CAISO’s Extended Day-Ahead Market.

Speaking during an Oct. 21 prehearing conference before the Public Utilities Commission of Nevada, Lindsey Schlekeway, market policy director for NV Energy, described the program as “a high-level concept” and said there are no formal agreements yet.

The conference was regarding NV Energy’s energy supply plan update for 2026/27. Tim Clausen, NV Energy’s vice president of regulatory affairs, said the company would file a request with the PUCN to join the EDAM as an amendment to the company’s energy supply plan.

As part of an update on the supply plan, Schlekeway filed written testimony explaining the company’s decision to withdraw from Western Power Pool’s WRAP. She detailed five “critical issues,” including “steep penalties for capacity deficiencies identified seven months before the compliance season.” (See NV Energy to Withdraw from WRAP.)

Another issue is that all load-serving entities in Markets+ will be required to participate in WRAP.

“While expanding participation can enhance regional reliability, it may disadvantage entities that prefer to remain in the Western Energy Imbalance Market … or transition to the Extended Day-Ahead Market,” she wrote.

In contrast to Markets+, EDAM won’t require its participants to belong to an organized resource adequacy program. Instead, EDAM will use a resource sufficiency evaluation to ensure participants’ RA going into the day-ahead and real-time time frames to meet their own needs without depending on others.

NV Energy will continue to watch WRAP’s development and remain open to future participation if the five issues are addressed, Schlekeway said.

“We will continue to follow WRAP, but we will also follow other avenues if others want to discuss resource adequacy in other forums in the West,” Schlekeway told Commissioner Tammy Cordova, the hearing officer in the case.

Schlekeway said that even after submitting a withdrawal letter, NV Energy can remain active in WRAP through participation in WPP’s Resource Adequacy Participant Committee, for example.

Cordova asked what would happen if the PUC directed NV Energy to participate in WRAP. “We can always re-enter the program,” Schlekeway responded.

Contacted after the prehearing conference, Schlekeway referred further questions on a potential Western RA program to an NV Energy spokesperson, who said the company had no further comment.

Rebecca Sexton, chief strategy officer for WPP, told RTO Insider that the organization is “aware of discussions about creating an alternative resource adequacy program.”

Sexton hopes that any entities that choose to leave WRAP will stay involved with the program’s governance during the two-year exit window and later decide to commit to binding participation. With binding-phase commitments from 11 participants and the potential for others to join, she said WRAP will launch “with a significant footprint with substantial load and resources and geographic diversity.”

Critical Time for WRAP

The discussion of an alternative resource adequacy program comes at a critical time for WRAP.

An Oct. 31 deadline is looming for participants to commit to the program’s first binding phase in winter 2027/28. Of the 11 members that have so far committed to WRAP’s first binding season, all but one are expected to join Markets+.

But some members say they need more time. PacifiCorp has asked WPP’s board of directors to allow WRAP participants to defer their decision to commit to the program’s binding phase by at least one year. (See PacifiCorp Asks WPP to Delay WRAP ‘Binding’ Phase Commitment Date.)

Portland General Electric also sent WPP a letter seeking a one-year deferral of the binding season. PacifiCorp and PGE have signed implementation agreements with CAISO to become EDAM’s first participants in 2026.

In response letters to PacifiCorp and PGE, WPP Board Chair Bill Drummond said delaying the binding phase “would have a detrimental effect on reliability for the region, including undermining confidence in WRAP data and modeling, limiting program compliance and preventing us from unlocking the full benefits of the program.”

The Imperial Irrigation District, which is slated to join EDAM in fall 2028, has staff participating in discussions of a potential new Western RA program.

“Momentum has started, communication is active, and kickoff meetings have begun,” IID spokesperson Robert Schettler told RTO Insider.

The district wants to be fully aware of, and ready to use, the full menu of RA options, said Schettler, who noted that IID is a balancing authority that is a net exporter most of the year.

IID isn’t currently pursuing WRAP membership, although it is an option in the future, he said.

When contacted by RTO Insider, a PacifiCorp spokesperson did not directly answer a question about whether the company has been participating in discussions of a new RA program.

“As part of prudent utility operations, PacifiCorp routinely evaluates opportunities to benefit customers, and resource adequacy is a significant focus of that process,” the spokesperson said in an email.

PacifiCorp is considering its participation in the WRAP binding phase ahead of the Oct. 31 deadline, the spokesperson said, and plans to continue its involvement in the program regardless of the decision.

NERC CEO Jim Robb laid out a litany of challenges at FERC’s annual commissioner-led Reliability Technical Conference, warning that the North American electric grid faces “a five-alarm fire when it comes to reliability.”

Speaking in the first panel of the conference Oct. 21, Robb said “an increasing number of small-scale events and near misses” in recent years have raised grid operators’ concerns, despite the fact that — “paradoxically” — grid reliability has remained “extremely high,” with few major outages. While he did not name any specific incidents, he mentioned several familiar concerns for NERC and the industry, including extreme weather incidents, interdependencies with natural gas and other sectors, the growth of data centers and other large loads, and a “toxic soup of security risks.”

Robb was joined on the panel by leaders and executives from several electric utilities, including Tricia Pridemore, president of the National Association of Regulatory Utility Commissioners and a member of the Georgia Public Service Commission.

FERC Chair David Rosner asked Pridemore about the Georgia PSC’s efforts to address the growing burden of data centers on the grid. Her reply focused on the importance of studying, planning and collaboration.

“We saw this load growth coming as data centers started to approach us back in 2019 and 2020. In 2023, we had 63 data centers in the state of Georgia, representing about $1.8 billion in GDP. We expect that to quadruple over the next seven years,” Pridemore said. “One of the things that I’ve been able to share with my colleagues across the country is the … premium that we place on planning — not just planning and writing reports [to shove] in a desk drawer, but an actionable plan that you can give to the utilities, and utilities can operationally build against.”

Pridemore said building out generation has been vital to meeting data center demand in Georgia, and that diversity of generation is another essential element that she promotes through NARUC. According to Pridemore, since 2019, the Georgia PSC has approved 17 GW of capacity additions through 2031. Georgia Power’s new nuclear reactors at Plant Vogtle Units 3 and 4, which came online in 2023 and 2024, respectively, accounted for 3.2 GW of capacity resources. Retiring coal plants have been replaced by natural gas generation and by extending the lives of other coal units.

Commonwealth Edison CEO Gil Quiniones said northern Illinois has become another busy site for data center construction in recent years. Data centers make up about 28 GW of the interconnection applications in process; for comparison, the utility’s all-time peak demand, set in 2011, was 24 GW. Other large loads expected to come online soon include a battery manufacturing facility and a quantum computing center, both in Chicago.

However, he also said operating in a deregulated state leaves “an accountability gap [with] no one in charge making sure that there is adequate generation capacity.” Quiniones told commissioners that ComEd is “trying our best to make sure that we know exactly what the real projects are,” but that “states will have to create new mechanisms, most likely through legislation, to allow … generation [to] get built.”

IESO is asking generation owners what it will take to extend the lives of their units beyond their current contracts as Ontario seeks to meet a projected 75% load increase by 2050.

IESO’s expiring contracts will grow from 5,000 MW/year in 2029 to more than 20,000 MW/year in 2040.

The ISO said it plans to begin soliciting repowering facilities in the Long-Term 2 Window 2 procurement, scheduled for Q2 2026. It will be open to energy and capacity streams, with repowering projects seeking 20-year commitments likely competing against greenfield projects.

“We’re very cognizant as the ISO that we’re going to need a … majority of … these existing facilities to come back and to sign on for an additional term,” IESO’s Ben Weir said during an engagement session Oct. 20. “So we really want to work with everybody to make sure that the framework is tenable.”

Dave Barreca, IESO’s supervisor of resource acquisition, said the ISO’s goal is to “secure the most cost-effective resources available [and] maximize the value of Ontario’s existing generation fleet.”

“As we all know, we forecast continued electricity growth over that period. And so there is a need for that power to come from somewhere, and I think that facilities that already exist — steel in the ground — is certainly as good a place as any.”

Current Practice

IESO has extended some expiring contracts by five years in the Medium-Term procurements (MT1, MT2) but it recognizes that some facilities will need longer contracts and big investments — including large-scale equipment replacements — to continue running.

“These facilities and others like them will continue to age,” Barreca said. “And so the question then becomes … what to do — other than, of course, decommissioning. And as these facilities get older, the five-year term may become … less feasible to keep that facility running.”

Definitions

IESO laid out an initial set of definitions for the program:

repowering: full or partial replacement that results in a “like new” facility and may increase output;

refurbishment: smaller-scale improvements that will extend lifespan for a shorter period and may result in increased output;

upgrades: replacing components such as turbines with more efficient equipment to increase plant output; and

expansions: adding new generating units to an existing facility to increase output.

But IESO also asked generators to help it fine-tune its definitions. “There is likely a range of viable options for existing facilities nearing the end of their current commitments,” it said in a presentation. “IESO is seeking to better understand these options in order to appropriately design repowering rules.”

Contract Term Risk

Barreca said IESO wants to balance certainty for owners with ratepayers’ “contract term risk”— the risk of too many facilities winning repowering contracts — and taking outages — at the same time.

“We’re going to see the retirement — or at least temporary retirement — of the Pickering Generating Station [for its own repowering]. So we can’t really afford to let everyone go off and repower at the same time,” Barreca said.

Gas Repowerings a Provincial Policy Matter

Weir said the ISO’s repowering rules likely will include technology-specific conditions — including those that would apply to repowering of gas facilities. “At the end of the day, whether we are going to allow repowered gas facilities will be a government policy call,” he said.

The Ministry of Energy and Mines’ Integrated Energy Plan calls for “the rational expansion of the natural gas network,” warning that “a premature phaseout of natural gas-fired electricity generation is not feasible and would hurt electricity consumers and the economy.” (See Ontario Integrated Energy Plan Boosts Gas, Nukes.)

Next Steps

IESO requested that written feedback on the repowering concept be submitted to engagement@ieso.ca by Nov. 21. Among the issues on which it seeks input are required contract length, potential regulatory barriers, eligibility and contract design, and the likelihood of generation owners choosing to decommission rather than repower.

The ISO promised a follow-up engagement in early 2026.

NERC has asked FERC to clarify the data it wants to see in biennial informational filings on the ERO’s most recently approved cold weather standard, as well as whether the commission expects NERC to continue submitting the filings FERC ordered with previous versions of the standard (RD25-7).

FERC approved EOP-012-3 (Extreme cold weather preparedness and operations) at its September open meeting. (See NERC Cold Weather Standard Gains FERC Approval.) NERC developed the standard in response to the commission’s directive ordering changes to the predecessor standard EOP-012-2. That standard itself was a revision to EOP-012-1, which FERC approved in 2023 while identifying numerous needed improvements.

Commissioners did not demand further changes to EOP-012-3 but did direct the ERO to submit follow-up filings every other year, beginning no later than October 2026 and ending in October 2034. The filings stem from the standard’s allowance for generator cold weather constraints — situations in which a generator owner may declare that a specific freeze-protection measure would result in a net loss of reliability on the grid — and must include:

The number of cold weather constraint declarations submitted to each regional entity.

The number of declarations approved, and their aggregate megavolt-amperes.

A summary of the rationales provided for approved declarations.

NERC also must submit a narrative analysis in the filing addressing:

Whether reliability coordinators, transmission operators and balancing authorities are notified in a timely fashion of constraint declarations and extensions to corrective action plans (CAPs).

The reliability impact of allowing 36 months to correct freeze-related issues, rather than a shorter time frame.

Whether compliance enforcement authorities interpret and apply the constraint declarations approval process.

Whether constraint declaration criteria are adequately defined and understood by registered entities.

The reliability impact of cold weather constraint declarations and CAP extensions.

In an Oct. 17 filing, NERC said it shared “the commission’s desire to ensure that … EOP-012-3 is advancing generator cold weather preparedness for extreme cold weather conditions,” but expressed uncertainty about two elements of the order.

The first was FERC’s directive that NERC report the aggregate megavolt-amperes for approved constraint declarations. NERC acknowledged that its Rules of Procedure mention megavolt-amperes in the criteria for placing entities on the ERO’s Compliance Registry but observed that it analyzes generating units based only on their real power in megawatts. NERC also pointed out that EOP-012-3 does not reference megavolt-amperes.

To clear up this confusion, NERC requested that FERC clarify whether it must report by megavolt-amperes only, or if reporting the aggregate megawatts of approved constraints would suffice. If the commission insists on megavolt-amperes, NERC requested that commissioners specify why they chose this approach “so that NERC may better understand the basis for such a collection.”

NERC’s other request applied to the annual filings FERC directed in its approval order for EOP-012-1, which were to include a range of information on cold weather constraints and corrective action plans. Observing “significant overlap in some aspects of the information” to be collected in each order, NERC asked whether it could consolidate both reports into the biennial filing ordered for EOP-012-3, and whether this consolidated filing still would sunset in 2034.

VALLEY FORGE, Pa. — Several stakeholders presented proposals for how PJM could address accelerating load growth as the Critical Issue Fast Path (CIFP) process on large load growth wraps up its second phase.

Many of the design components revolved around requiring large loads to bring their own generation (BYOG); pathways for fast-tracked interconnection studies for new resources; allocating capacity and interconnection costs to large consumers; and queues to delay them from coming online until there is sufficient capacity to serve them.

The RTO opened a poll on the proposals following the Oct. 14 meeting to gauge support before moving on to the third phase of the CIFP process, in which the design components will be combined into holistic packages. Manager of Stakeholder Process and Engagement Michele Greening said Phase 3 packages should be designed to resolve all issues identified in the Board of Managers’ letter initiating the CIFP. The first of the Phase 3 meetings is scheduled for Oct. 24.

Eolian BIGPAL Proposal

The bilateral integration of generation portfolios and load (BIGPAL) proposal from Eolian would allow planned large loads to procure their capacity from adjacent resources coming online at the same time.

The resources would qualify for a 90-day interconnection study process and not participate in the capacity market; be assigned capacity interconnection rights (CIRs); or be derated by PJM’s effective load-carrying capability accreditation framework.

While the proposal’s definition of “adjacent” is not yet set, Eolian said siting the resource electrically near the load would reduce the need for transmission upgrades and allow it to perform under emergency conditions. While a performance assessment interval (PAI) is active, the BIGPAL configuration would be required to reduce its net load to zero. Load flexibility would serve as a backstop to resource performance.

The risk of the resource underperforming during a PAI would be shared by the parties to the contract, with penalties if there is a net draw off the grid.

The adjacent resource would be able to participate in PJM’s energy market and would be available to security-constrained economic dispatch. Brattle Group consultant Andrew Levitt, who helped prepare the proposal, said it would make sense for BIGPAL resources to operate as normal PJM resources when PAI risk is low and prioritize being available to serve the adjacent load when an emergency appears likely.

Brattle modeled how BIGPAL would perform in the 2030 delivery year, using PJM’s load and expected resource mix and two RTO scenarios: 6 GW of new unforced capacity and 8 GW of retirements, and 12 GW of new capacity and no deactivations. The firm developed a moderate weather scenario built off 2018 and a more severe weather year based on 2022. The model assumed 25 GW of BIGPAL load paired with 20 GW of storage and 5 GW of gas generation.

The analysis found there would be no load shed in a moderate weather year in the scenario where deactivations outpace new entry and 16 hours of load shed in a severe weather year.

Bruce Campbell, principal of Campbell Energy Advisors, said he’s concerned about any proposals that would create new forms of curtailable load that would be dispatched after demand response customers. Coming out of a summer with a high amount of pre-emergency load management deployments, he said participant fatigue may be a concern going forward with the prospect of substantially more dispatch as reserves shrink. He noted that “fatigue” can mean simply that customers are losing money with each hour of dispatch.

Glatz and Silverman Present Alternative NCBL Design

Abraham Silverman, research scholar at Johns Hopkins University, and Suzanne Glatz, principal of Glatz Energy Consulting, presented several design components intended to minimize the impact large loads would have on existing consumers.

They proposed a bifurcated capacity market in which the first round of the auction would set a clearing price for native and non-large load, followed by a second round clearing large loads and any generation that had not already cleared. The price for the second round of the auction would be inclusive of make-whole payments for resources that cleared in the first round, ensuring that all resources receive the same capacity price.

Building on PJM’s mandatory non-capacity backed load (NCBL) proposal, they recommended a variant that would subject large loads to curtailment in delivery years when the capacity market cleared above the midpoint on the variable resource requirement curve. Curtailments would fall ahead of all DR customers in the stack of emergency procedures. While mandatory NCBL is no longer PJM’s preferred solution, it remains a design component stakeholders can include in their packages.

Load-serving entities would be able to avoid being assigned NCBL allocations by ensuring that large loads can offset 80% of their peak load for at least four hours, 10 times a year. Glatz said this would create an incentive to participate in BYOG models.

NCBL load would be required to pay half of the capacity clearing price each delivery year to capture the benefits it receives from non-firm service when there are no curtailments.

The initiation of the CIFP process would be considered the cutoff point for any NCBL requirement, with existing load exempt.

Another component would exclude large loads from PJM’s forecast unless the relevant utility attests that all distribution and transmission upgrades needed to interconnect the load will be complete before the delivery year; the large load attests that it’s not planning similar new service requests that might result in the project being canceled or modified; and the customer provides evidence of commercial maturity, such as “take-or-pay” agreements for transmission service. If an NCBL model similar to PJM’s initial proposal were to be implemented, participating large loads also would be excluded from the forecast.

NRDC Supportive of NCBL

The Natural Resources Defense Council recommended an NCBL construct in which large loads would not receive firm service unless they were paired with new capacity or resources that did not clear in the capacity market.

Large loads could gain firm service by committing to participate in DR or price-responsive demand programs, or contracting with other consumers to participate on their behalf.

The proposal aims to recognize the jurisdictional questions around PJM defining particular consumers as being subject to NCBL and leaving implementation to the states. The RTO would determine the amount of NCBL needed across its footprint and distribute that figure across locational deliverability areas (LDAs); from there, states and utilities would determine how to assign that to customers.

The proposal would designate curtailment as either the final energy emergency alert Level 1 action or the initiator for Level 2. This would lead to it being instituted either prior to or concurrent with the start of scarcity pricing.

Few planned resources expected to come online in time to participate in the 2026/27 Base Residual Auction (BRA) have submitted offers, which is creating a false tightening in the market, according to the NRDC. Reducing the risk of participation could mitigate that, including by PJM making a commitment that it will not seek to reinstate the minimum offer price rule in place before 2018. (See 3rd Circuit Rejects Challenges to PJM MOPR, Affirms Authority over FERC Deadlocks.)

The NRDC conducted analysis on the cost of the load growth and reliability gap that PJM predicts, finding that consumers would pay $163 billion in capacity costs between the 2027/28 and 2032/33 BRAs. Data centers would pay a small amount of those increased capacity costs, and most of the revenue would flow to existing supply, which the NRDC found would create a scenario where 81% of the $163 billion are “deadweight” payments that existing consumers pay to existing supply.

Monitor Recommends Load Interconnection Queue

The Independent Market Monitor proposed creating an interconnection queue for large new data center loads in which they would be interconnected only when any required transmission upgrades are complete and there is enough capacity and energy to serve them reliably.

Large loads would be eligible to bypass the queue via an expedited interconnection process if the loads brought new generation (BYONG). The new generation would have to be deliverable to the grid, deliverable to the new load, and capable of matching the amount of time the load will be online. Monitor Joe Bowring gave the example of intermittent resources combined with storage, or thermal generation, both qualifying for the duration component.

Participation in DR would not fall under the BYONG model, as Bowring argued it does not match the duration of the load and is not equivalent to bringing new generation capacity online.

Bowring said the proposals to treat large new data center loads as on the demand side would have them interrupted only after existing demand-side resources are interrupted and only if there is a reliability emergency. That treatment would impose significantly increased interruptions on existing demand-side customers and risks those customers leaving the program, he argued. It also would increase the occurrence of scarcity pricing in the energy market, which imposes higher energy costs on all customers.

“Demand side is not generation,” Bowring said in an email to RTO Insider. “If the large new data center loads are going to enter without capacity, they should be interrupted whenever existing capacity is needed by the customers that pay for it.”

Bowring said if PJM is not capable of serving a new load, the RTO should not be obligated to allow it to interconnect. He said the premise of all the other CIFP proposals is that PJM must interconnect large new data center loads when there is not enough capacity to serve them reliably.

“That premise is not correct,” he said. “Allowing the interconnection of large new data center loads without matching capacity imposes costs and risks on all other customers, increasing prices and the risk of blackouts for other customers. That is not consistent with PJM’s stated objective of putting reliability first.”

It also increases the demand for energy without increasing the supply of energy, increasing energy costs for all customers by an estimated $2 billion to $3 billion per year, Bowring said.

Pointing to Part A of the Monitor’s report on the 2026/27 BRA, Bowring said data center load growth has caused capacity costs to increase by $16.6 billion over just the past two auctions — costs that should not be shifted to existing consumers, he said.

Vistra Seeks Penalties for Utilities Short on Capacity

Vistra proposed instituting penalties for utilities that do not cover their own capacity needs with the aim of incentivizing bilateral contracts that take strain off the capacity market.

The proposal includes variants for triggering penalties if the load forecast for a capacity auction signals it may be tight, during emergency procedures or a combination. Assessing the penalties in advance carries the advantage of providing more incentive to get contracts in place before the auction, while implementing them during emergencies creates more flexibility on the amount of risk a utility is willing to accept. Several penalty rates also were presented for each option.

Operational penalties would create incentives for utilities to offer load flexibility products to customers to mitigate the risk the utility might not have enough capacity in place, while planning-based penalties would create more incentives to contract with DR providers.

EKPC Recommends Requirements for Self-supply

The East Kentucky Power Cooperative proposed “significant” penalties for LSEs that enter a BRA without enough owned or contracted supply to cover its capacity obligation. The penalties would be assessed against all deficient LSEs within an LDA if an auction does not procure enough supply for that zone.

Large loads would be required to identify the LSE that will serve them before they are included in the load forecast as a large load adjustment (LLA), which feeds into the amount of load to be served in a given BRA; if an LSE is not identified, it could be treated as being served by the default provider. That is intended to serve as a “reality check” that the load is likely to come into service in that delivery year and reduce duplicative LLA requests. State involvement in the load forecasting process could further advance the reality check. Large loads would be defined as a site with load exceeding 50 MW.

The penalties would be distributed to LSEs that had procured enough capacity for that delivery year as compensation for the price pressure and load shed risk they faced. State regulators would be encouraged to create retail rate structures that allocate penalties to large loads and reduce the impact on existing consumers.

NOVEC Proposes Changes to NCBL

NOVEC proposed modifications to PJM’s NCBL proposal that would remove the load from the capacity market and place its curtailment as the penultimate step in the RTO’s emergency procedures, after all other DR products and just before load shed.

If an EDC or LSE cannot assign enough NCBL to meet PJM’s allocation for its region, it would be assessed a daily deficiency penalty for the amount it is short, which would be refunded to other utilities. If NCBL load does not curtail, it could be subject to FERC and NERC compliance and financial penalties.

NOVEC’s Rory D. Sweeney said that if NCBL is to be implemented, it should be structured as a permanent late-stage emergency procedure.

Maryland OPC Focuses on Load Forecast and BYOC

The Maryland Office of People’s Counsel recommended changes to PJM’s load forecast process, a bring your own capacity (BYOC) model, a large load-specific DR product and assigning more load shed obligation to regions with large loads not backed by new capacity.

The proposal would have PJM develop scenarios accounting for the uncertainty around LLAs coming online when it develops its load forecast, with the modeling tied to the advanced nature of the capacity market and Regional Transmission Expansion Plan (RTEP). The amount of load included in the forecast for each utility could be reduced if they do not establish a tariff for large loads or a dedicated oversight process for their interconnection that includes project milestones and financial commitments.

The BYOC element requires new large loads to either bring enough capacity to meet their own needs or offer the equivalent of their peak load into a load-offset demand response (LODR) product — a temporary program designed for large loads to net to zero either by curtailing or activating behind-the-meter generation. The capacity would have to be deliverable to the load and come online at the same time.

Mainspring Seeks Changes to EIT

Mainspring Energy presented several changes to PJM’s proposals, including shifting the focus of its expedited interconnection track (EIT) to prioritize resources that can be built quickly, rather than prioritizing the size.

The EIT model presented on Oct. 1 would create a 10-month interconnection study process for projects at least 500 MW and capable of being in service within three years.

The revised eligibility requirements would allow projects above 50 MW to participate, including projects to uprate or repower existing generation. It also would make state sponsorship of projects voluntary, removing a requirement PJM said was intended to reduce the risk that a project would be expedited through its queue only to become mired in state siting and permitting processes.

Director of Wholesale Market Development Brian Kauffman said the majority of data centers are on the scale of 50 MW and could be served by comparably sized resources.

It also recommended that PJM include a voluntary NCBL model in its package and for states to develop non-firm or flexible service models for retail load. Kauffman said speed-to-market is the priority for data center developers, who might be willing to accept less firm service in exchange for faster interconnection.

Pa. and Va. Governors Offer Perspectives

Presenting on behalf of Pennsylvania Gov. Josh Shapiro and Virginia Gov. Glenn Youngkin, Pennsylvania Deputy Secretary of Policy Jacob Finkel overviewed their perspective that efforts to streamline the entry of new supply and minimize the impact to residential and commercial ratepayers should be prioritized.

Models that offer a carrot rather than a stick are preferred, particularly those with voluntary short-term flexibility paired with incentives for long-term resource development, Finkel said.

The governors support Eolian’s BIGPAL proposal as a way of reducing delays in getting generation built, though more market design changes would be needed to ensure proper incentives are in place, Finkel said. Load forecast changes would also be welcome, but he noted that would not change the supply and demand challenges PJM faces.

Before he became President Trump’s energy secretary, Chris Wright was CEO of Liberty Energy, a natural gas fracking company, and an avid proselytizer for fossil fuels as the foundation of modern lifestyles, prosperity and security in the U.S. and in emerging nations striving for Western standards of living.

Wright’s typical pitch in Liberty YouTube videos links global progress, from fighting poverty to lowering infant mortality rates, to two key factors: the spread of human liberty and democratic government and “the surge in plentiful, affordable energy from oil, gas and coal.”

Wright’s recent efforts to claw back legally obligated federal funding for clean energy projects ─ many in Democratic-led states ─ speak volumes about his commitment to liberty and democratic government.

His arguments for fossil fuels are at least historically accurate: The social, technological and economic advances made possible by the Industrial Revolution in the 19th and 20th centuries were powered by fossil fuels. But, as much as Wright discounts it, the world is in the midst of a major energy transition, from petrotech to electrotech, which the vast majority of countries ─ with the notable exception of the U.S. ─ are pursuing to promote innovation and economic growth and provide a more efficient, affordable and secure future.

K Kaufmann

This reframing of the energy transition is laid out in The Electrotech Revolution, an extremely detailed, well-documented and provocative report from Ember, a London-based energy think tank.

Rejecting the business-as-usual paradigm of “fossil fuels gradualists” versus “net-zero advocates,” co-authors Daan Walter, Sam Butler-Sloss and Kingsmill Bond stake out electrotech as a third way, focused on “exponential energy technologies revolutionizing how we generate, connect and use electrons … such as solar, wind, batteries and digital solutions.”

This electrotech revolution is “driven by physics, economics and geopolitics,” they write. “After all, the arc of energy history bends toward solutions that are leaner, cheaper and more secure.”

The 112-page report is packed with charts, facts and figures that at every turn demolish Wright’s arguments for grounding U.S. energy abundance and dominance ─ and the welfare of the country’s 342 million citizens ─ in fossil fuels. It depoliticizes the debate and should be required reading for every federal and state policy maker, regulator, electric industry executive and anyone else concerned or just curious about the future of our electric power system.

Chris Wright is a smart, well-informed person, so I am going to presume he knows everything that is in the Ember report but is willfully ignoring and denying the reality of the electrotech transition to advance the political and financial interests of the Trump administration and the U.S. fossil fuel industry.

A handful of charts from the report show why Wright is so wrong. He and Trump may be able to slow the clean energy transition in the U.S, but the electrotech narrative is undeniable and will win out.

Already, China is leading the transition, and emerging economies are leapfrogging over fossil fuels, the report says. What side of history do we want to be on?

The Inefficiency of Fossil Fuels

The Ember report starts with some eye-opening basics. First, the physics: Fossil fuels are an incredibly inefficient way to produce electricity.

One exajoule, or EJ, is about 278 terawatt-hours of power, so the amount of energy and money we lose burning fossil fuels is simply ridiculous. The figures here, and throughout the report, are global, unless otherwise noted.

Further, the report shows, what most of us really care about is not the primary energy (basic fuels like coal and gas) or final energy (the gasoline and electricity delivered to consumers). Our day-to-day lives depend on useful energy that produces heat and hot water for our homes, plus steel and other goods (energy services) that create economic value (GDP).

Renewable energy and associated clean technologies ─ like electric vehicles and heat pumps ─ are two to four times more efficient than fossil fuels for generating electricity, powering our transportation and heating our homes.

At a time of rising electric bills, efficiency and cost savings are top priorities for consumers, businesses and the policy makers and regulators besieged by frustrated and increasingly desperate people, facing critical decisions about which bills to pay first.

The question here is simple: Which side of the laws of physics do we want to be on? We should be planning and building out our electric power system accordingly.

Peaking out

Wright and others often argue that the need for fossil fuels will continue to grow, given the demand for reliable, affordable energy from Europe, China, India and emerging economies.

| Ember using data from IEA WEB

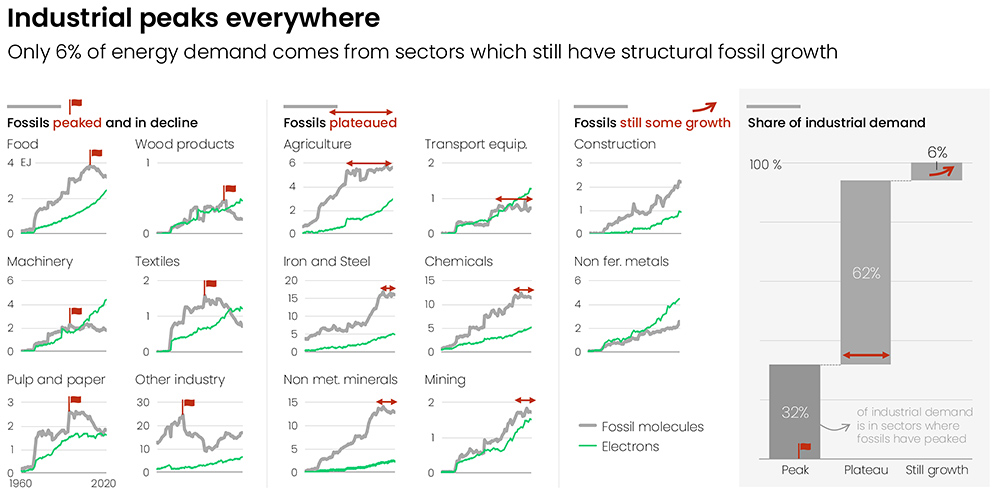

Wrong again. The Ember report tracks how fossil fuel use has peaked or at least plateaued across various industries worldwide. Pulp and paper and textiles peaked decades ago, while even mining, chemicals and transportation have plateaued. Only construction and non-iron metals, accounting for 6% of industrial demand, are still on a growth curve.

Nearly half of the world is past peak fossil fuel demand for electricity generation, Ember says. China almost single-handedly has been responsible for any growth in global demand for fossil fuels over the past eight years, but even there, Ember finds evidence that the country is moving toward a plateau.

Slashing Fossil Fuel Imports

At least one point in Wright’s argument rings true: Many countries remain dependent on imported fossil fuels ─ 50, in fact, where imported oil, gas and coal account for 50% or more of the primary fuels they use to produce electricity and gasoline.

At the same time, the report notes, almost every country in the world has sufficient sources of renewable energy ─ wind, solar, hydro ─ to meet their existing energy demand, in many cases at least 10 times over. A good three-quarters of Africa is classified as “superabundant,” meaning these countries could meet their existing demand 1,000 times over with their renewable resources.

| Ember using data from IEA WEB and World Bank

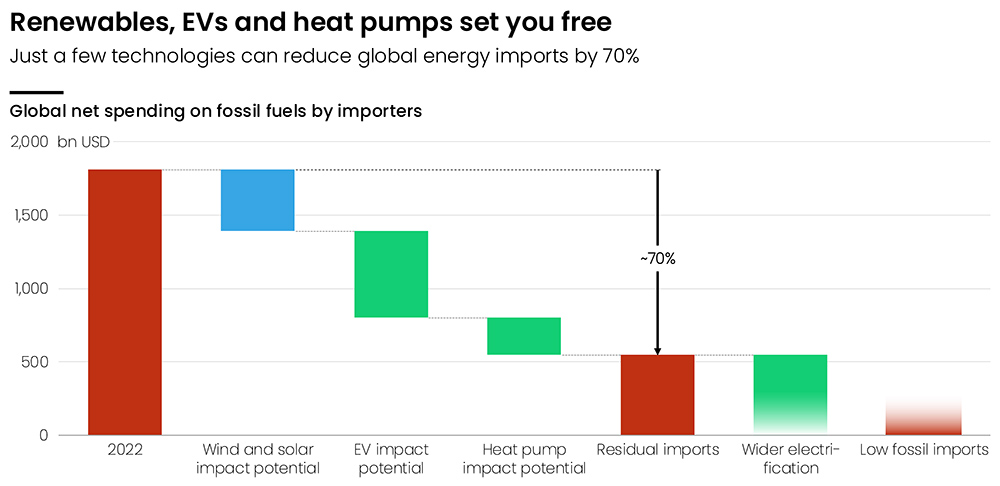

At the same time, the hundreds of billions of dollars spent on importing fossil fuels could be slashed 70% with three existing technologies: renewables in the form of wind and solar, electric vehicles and heat pumps. Wider electrification could shrink fossil fuel imports even further.

While the U.S. is a net exporter of fossil fuels ─ exporting more than we import ─ the country still imports more than 8.4 million barrels of crude oil per day, primarily from Canada. Those imports now come with Trump’s 10% tariff; all the more reason to switch from petro- to electrotech.

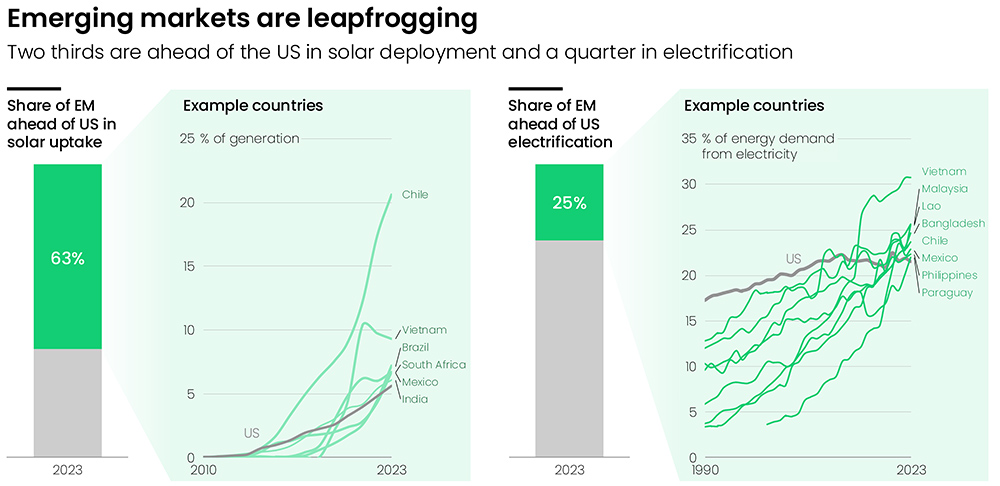

Emerging Markets Leapfrog

One of Wright’s more compelling arguments for fossil fuels centers on energy poverty ─ the 666 million people around the world who live without electricity, 85% of whom live in Sub-Saharan Africa, according to a recent report from the World Bank.

At least, he makes it sound compelling, with fossil-fueled electricity bringing modern, Western lifestyles to emerging economies.

But fossil-fueled power plants require extensive supply chains and supporting infrastructure ─ pipelines, transmission systems ─ which means they may not be the best way to provide power to remote villages in Africa, or anywhere else for that matter. The World Bank notes that “new technologies and business models for decentralized renewable energy (DRE) ─ such as solar home systems and solar mini grids ─ offer flexible solutions for these areas.”

| Ember using data from IEA

Which may be why, according to the Ember report, many emerging economies in Latin America, Africa and Southeast Asia are adopting solar and electrifying faster than the U.S., leapfrogging fossil fuels to build their economies on clean energy.

As noted in the chart above, 63% of emerging economies ─ from Chile to Vietnam to South Africa ─ are ahead of the U.S. in solar adoption, while 25% ─ including Laos, Malaysia and Bangladesh ─ are ahead in electrification.

Those numbers are, at least in part, being driven by direct cleantech investment from China ─ more than $100 billion in emerging economies since 2023, Ember says. China dominates global markets in solar, storage and electric vehicles, while the U.S. under Trump is increasingly isolated by high tariffs and falling further behind in clean energy manufacturing and deployment.

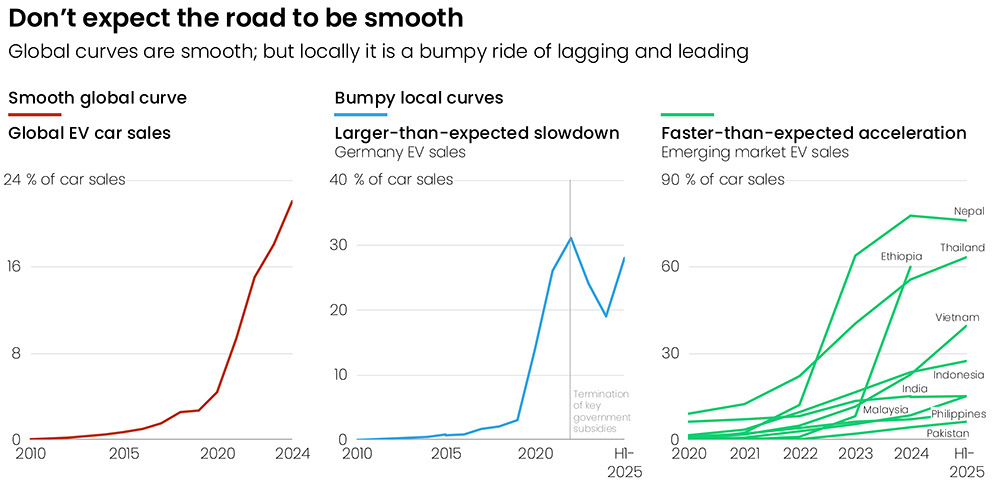

Bumps Ahead

While the physics and economics for electrotech are pretty convincing, Ember knows the real world is rarely as science- and fact-driven as we would like it to be.

| Ember using data from IEA and Segment Y via New York Times

The electrotech transition will be uneven across political and economic landscapes, as seen in Ember’s analysis of EV sales globally, in Germany and emerging economies. Where markets have been dependent on government subsidies ─ in Germany and the U.S. ─ we are going to see some dips and slowdowns, followed by resets and renewed gains.

But such bumps are being offset by faster-than-expected EV adoption in emerging economies, again likely due to China’s high-quality but relatively cheap EVs. You know the ground is shifting when 60% or more of new car sales in Nepal and Ethiopia are electric, driving that steep upward curve in global EV sales.

Certainly, the way forward in the U.S. will be even bumpier with Wright and others in the Trump administration putting as many obstacles as possible in the way of renewables and other clean technologies while setting the country on a path to continuing petrotech dependence and ever-rising electric bills.

One example: On Oct. 16, Wright announced a $1.6 billion loan guarantee to a subsidiary of American Electric Power for transmission upgrades in Indiana, Michigan, Ohio, Oklahoma and West Virginia. According to figures from the Energy Information Administration, all five of these states generate two-thirds or more of their electric power from natural gas and coal. Coal makes up 91% of West Virginia’s generation mix.

Among 321 Department of Energy grants and other awards Wright canceled Oct. 2, 26 were from the Grid Deployment Office.

But one thing neither Trump nor Wright seems to be taking into account ─ all the DOE employees they have let go are now on the ground, starting new businesses and nonprofits, leading corporate, state and local government efforts to decarbonize their power supplies and pushing electrotech innovation and investment forward. They’re ready to ride out the bumps and are not giving up.

Like the Ember report, they know that responding to demand growth in the U.S. and ensuring access to electricity worldwide should not be about politics. Yes, electrotech will cut greenhouse gas emissions, but it is laser-focused on providing the best, cheapest and most dynamic and flexible technology to power our increasingly digital world.

Secretary Wright, come the revolution, what side of history do you want to be on?

Livewire Columnist K Kaufmann has been writing about clean energy for 20 years. She now writes the E/lectrify newsletter.

The North Carolina Utilities Commission held hearings over several days examining how utilities plan to reliably serve large loads including data centers and adapt to the changes they’re bringing to the industry.

“We are experiencing a lot of growth in the Carolinas, and that is not restricted just to large loads; it’s across residential, commercial, industrial and manufacturing sectors,” Jonathan Byrd, managing director of rate design for Duke Energy, told the commission Oct. 15. “And that said, we certainly acknowledge that these large loads present unique challenges and opportunities. The growth we’re seeing reflects the state’s favorable business environment, which includes constructive energy policies and affordable and reliable electricity.”

Duke updates its rules as the new load paradigm has become apparent, and fine-tuning is going to continue as it gains experience serving new customers, he added.

The utility, which serves most of the state, has received inquiries from 420 projects totaling 46 GW in total possible demand. Of those projects, 128 are data centers representing 37 GW of demand, said Andrew Tate, Duke’s managing director of economic development.

“We acknowledge that only a fraction of these will ever progress to actually receive service,” Tate said. “We receive new project inquiries every week, and every week we have projects that advance to either terminate or loss, or successful outcome.”

Large load projects can be a challenge for utility planners, but they bring major economic benefits, including jobs and tax revenues for communities that sometimes have been overlooked in past economic expansions, he added.

“The large load customers that we work with daily value certainty in generation resources, as opposed to the uncertainty that can exist in some markets when it’s uncertain who’s building the generation,” Tate said. “Our customers expect us to provide the load to serve their needs.”

While on-site backup generation is common, Duke has seen relatively few large load customers interested in co-location, and that usually relates to speed-to-market concerns when they want to locate in an area with transmission constraints, he added.

Duke has arrangements with the new large load customers that are designed to hold existing customers harmless while helping the sites get online in the name of economic development, said Alex Castle, the utility’s deputy general counsel.

“Protecting existing customers remains our central priority, but we’re always conscious of the balance that’s required to ensure that the risks and accountability that we’re asking new large load customers to carry are reasonable,” Castle said. “We intend to check and adjust over time in order to refine our approach to right-size these financial and operational requirements.”

Duke starts by studying the project’s impact on its grid and resource adequacy, which are laid out in a “letter agreement” that the prospective load has 30 days to sign once issued. That signals an intent to proceed and comes with preliminary financial commitments. That is followed by an electric service agreement (ESA) that must be signed within 120 days and lays out the long-term conditions for service, Castle said.

Dominion’s Experience with Data Center Alley

The NCUC also heard testimony from Dominion Energy, which has long-term experience with data centers, as its Virginia utility serves the largest market for them in the world.

Data centers make up 25% of the utility’s total demand, which is expected to rise to 50% in 2035, said Vice President of Regulatory Affairs Scott Gaskill.

Dominion has set up an internal “Data Center Practice” to help manage its service of the key customer group, said its director, Stan Blackwell.

“If you add up the next five large U.S. markets — add them together — they’re not as big as our Virginia market,” Blackwell said. “In fact, it’s [just] Loudoun County. It’s about 30 square miles. It’s the largest market in the world.”

Just seven customers make up 72% of that market, and Dominion is able to base its forecast around their future growth individually, while putting the other 28% in an eighth category for forecasting. The main market in Loudoun runs an average of about a 90% capacity factor, and curtail-ability of that load is limited. It serves as a constant baseline of demand while small customers drive the peaks, Blackwell said.

A chart Dominion showed laying out the growth in demand forecasts in recent years and recent peak demand days | Dominion Energy

Dominion is seeing data centers expand beyond Loudoun, which is the wealthiest county per capita in the nation with expensive land. The new wave of data centers built to train artificial intelligence is leading to more sites being located in cheaper areas of Virginia.

“In AI, there’s kind of two modes of it, if you will,” Blackwell said. “One is, you train a model. So, your data center cycles up and down to train a model. Once it’s trained, you take it out of that [and] put it in what’s called an inference data center, and that’s the one that runs like a chainsaw. So, once you have a model train, it runs all the time. You don’t tend to want to curtail that, because that’s what customers access.”

The utility has so much experience with data centers that it is able to build statistical models based on past experience to forecast future demand from the sector.

“We do it statistically by our largest customers and look at their past behavior and then make an assessment whether that will continue in the future,” Blackwell said. “And we haven’t seen a change in the behavior over the whole time period: 2013 to today.”

Dominion has a pending proposal at the Virginia State Corporation Commission to set up a new large load tariff that will separate out the customer class, offering data centers and others transparency while ensuring fair cost allocation, Blackwell said. (See Citing Inflation and Load Growth, Dominion Asks Virginia for Higher Rates.)

Are Large Load Tariffs Necessary?

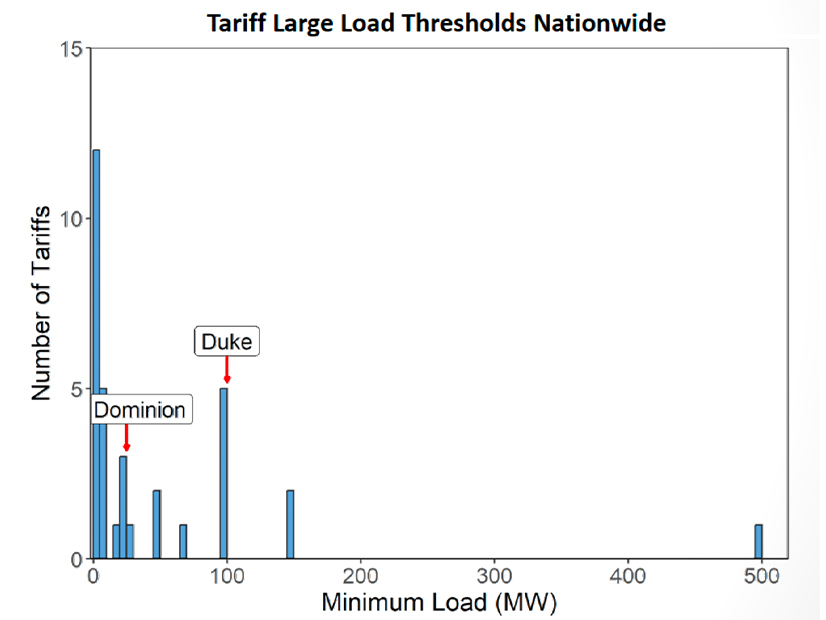

Neither Dominion nor Duke were in favor of setting up similar large load tariffs for North Carolina, but NCUC public staff urged commissioners to get ahead of the issue and start working on constructs for both companies now.

The suggestion comes after staff reviewed 44 tariffs from 28 states, said Dustin Metz, NCUC engineer for public staff.

“Large load has driven electric system growth, but with fewer larger customers than in the past, high-load-factor customers have unique operating characteristics and occupy a different role than traditional large general service or traditional industrial customers,” Metz said. “With careful rate design, reasonable ratepayer protections will allow parties to prosper, support economic development and ensure risks are mitigated.”

Even if large customers do everything right, they still face economic risks that could lead to their early retirement, which risks stranded costs falling to others, said Patrick Fahey, public utilities regulatory analyst for the North Carolina Department of Commerce.

Commissioner Karen Kemerait noted that the utilities do not want specific large load tariffs in North Carolina, arguing their current rate structures allocate costs fairly for any new load, and asked staff members for their response.

“If we decide to do nothing in terms of a new tariff in the next three years, the large load is already going to be here,” Metz said. “They’re going to be under a different tariff design.”

Staff want the commission to start working on large load tariffs now so that they are in place once the new loads start to make a major impact on North Carolina, he added.

NCUC Public Staff’s chart showing the megawatts of demand where different states’ large load tariffs kick in | NCUC Public Staff

“There is this variability in load forecasting that others have touched on — who will and won’t show up — and how that will change even in a relatively short time period means that the earlier we can get ahead of this and establish something that helps set guidelines as to what the large load customers can come in to expect,” Fahey said. “And that gets into potential improvements in forecasting and a better understanding from that customer’s perspective, especially if they’re cross-shopping against different states.”

Lucas Fykes, policy director of the Data Center Coalition, said in testimony Oct. 14 that his group has been involved in the development of large load tariffs around the country, and many start to kick in for customers with demands of 50 to 100 MW, though on the lower end that can start to impact major industrial sites – not just data centers. The main issue is that no group of customers is singled out and that cost allocations are fair to the large loads, he said.

“Certainty is very important for planning and operational purposes,” Fykes said. “We are leaning in as an organization, and many of our members are individually leaning in, in support of taking traditional terms that were usually in ESAs and putting those into tariff requirements that are fair and equitable.”

Large load tariffs vary by utility and states because the facts on the ground are different, but Daymark Energy Advisors consultant Jeffrey Bower (a witness for the Environmental Defense Fund) said some best practices have become apparent.

“Customers don’t want to invest unless they are clear about what their obligations are long term,” Bower said. “Utilities don’t want to invest in new infrastructure unless they’re clear that the customers are going to be there and are going to be contributing meaningfully to the cost of that infrastructure.”

Contract terms need to be shared with prospective customers early in the process, and defined rate classes that acknowledge their specific needs are important for certainty. Termination fees are another important part of the toolkit.

“The next principle, which has been discussed a bit, is the equitable cost allocation,” Bower said. “And so that’s a fundamental principle around cost causation and allocation, which protects existing customers, creates fair rates for new customers and aligns the incentives for efficient utilization of grid resources.”

“Just last week, AEP announced that since enacting the tariff, its pipeline of data centers had fallen from 30 GW down to 13 GW,” Bower said. “And so, this is clearly a big impact of the tariff design. It’s up for debate whether this drop signifies a reduction in economic development, or if it’s a decrease in speculative interconnection requests.”

The Role of Flexibility in Meeting Demand

With speed to market and the industry’s ability to meet demand that is projected to grow faster than new, firm capacity can come online, demand flexibility from data centers has been discussed as a way to square that circle.

“Our goals for this were to support regulators and stakeholders in identifying strategies and tactics to accommodate this load growth without compromising the reliability, affordability or progress on decarbonization,” Norris said.

The study is based on examining the 22 largest balancing authorities in the country, which account for 95% of its total demand for electricity.

“Current expectations are that AI-specialized data centers will represent the single largest share of U.S. electricity load growth over the next five to seven years, and could represent up to 44% through 2028 alone,” Norris said.

Coupled with the need to maintain reserve margins, the highest forecasts indicate national peak load growth of 180 GW by 2030 alone. Norris said that easily could rise from 700 GW today to 850 GW in the next decade, which would exceed the supply chains for new gas turbines.

“We don’t know exactly how many turbines will be available,” he added. “The current estimate suggests 60 to 80 GW by 2030. Mitsubishi says that they are ramping up production.”

An example from the Duke University data center report showing how little demand flexibility is needed to unlock spare capacity | Duke University

Battery storage can help; solar still is economical; and eventually small modular reactors or other new technologies will become available.