Three of the four developers building wind farms in U.S. waters are challenging the Trump administration’s Dec. 22 order suspending all such construction.

Some light soon may be shed on the reasoning for the stop-work order, although not publicly: The federal government said it should, during the week of Jan. 5, be able to provide classified information bearing “secret” or higher classification to a judge hearing the first of the challenges.

Coastal Virginia Offshore Wind (CVOW) developer Dominion Energy sought a preliminary injunction Dec. 23 in U.S. District Court for the Eastern District of Virginia.

Revolution Wind, a joint venture of Skyborn Renewables and Ørsted, challenged the suspension Jan. 1 in U.S. District Court for the District of Columbia.

Empire Wind developer Equinor challenged the suspension on Jan. 2, also in U.S. District Court for the District of Columbia.

Avangrid and Copenhagen Infrastructure Partners have not announced any response to the suspension of Vineyard Wind 1, which is in late stages of construction and already generating power with some of its turbines.

The only other wind farm being built in U.S. waters is Sunrise Wind, which is in earlier stages of construction. Developer Ørsted said it is considering its options for how to respond to the Sunrise suspension.

The direction of the greatly diminished U.S. offshore wind sector rides on these challenges, as no other projects appear likely to start construction during the Trump administration.

The Department of the Interior said the pause would give all relevant government agencies time to work with the leaseholders and state governments to mitigate those risks.

But the pause also will cause the developers to incur millions of dollars in unbudgeted expenses per day.

Dominion was first in line to fight back.

It said it has spent $8.9 billion of CVOW’s projected $11.2 billion cost to date and already begun recovering that money from ratepayers. It called the order by the U.S. Bureau of Ocean Energy Management arbitrary and illegal, as well as inconsistent with BOEM’s previous actions during its “extraordinarily thorough” reviews of the CVOW proposal during a yearslong permitting process.

Interior indicated its Dec. 22 pause came in response to a situation that evolved after the BOEM permitting and said some of the explanation for this was classified.

Judge Jamar Walker on Dec. 28 converted Dominion’s request for a temporary restraining order to a motion for a preliminary injunction and set a Jan. 16 hearing on the motion. He gave Interior until Jan. 9 to provide the classified information that he called critical to evaluating the case.

‘Patently Unlawful’

The complaint filed Jan. 1 by Revolution Wind is another chapter in its running battle with Interior over the stop-work order the department had slapped on it Aug. 22.

Judge Royce Lamberth ordered that stop-work order lifted Sept. 22, and Revolution is asking him to do the same with the Dec. 22 order, saying it too is “patently unlawful” and violates the Administrative Procedure Act (APA), the Outer Continental Shelf Lands Act (OCSLA) and the U.S. Constitution.

In its news release, Ørsted said Revolution is 87% complete, with 58 of 65 turbines installed. It had been set to start generating power later in January.

The Danish company said Aug. 25 that total investment in Revolution and Sunrise was expected to be approximately $15.6 billion.

Empire Wind also is a two-time target of the Trump administration, which slapped a stop-work order on it in April but lifted it a month later without court intervention.

Empire said in its Jan. 2 filing that the April stop-work order cost it $200 million in delay costs and drove the project to the brink of cancellation. It said this new stop-work order likely will result in project cancellation if it lasts 90 days — the developer cannot draw down on construction financing and the complex, highly choreographed schedule would be thrown off.

Empire said the project is approximately 60% complete at a cost of more than $4 billion so far, $1.5 billion of it since the April stop-work order was lifted.

Empire asks the court to vacate the suspension and to declare it unlawful, arbitrary and capricious, an abuse of discretion, and a violation of APA and OCSLA. It seeks a preliminary injunction as the case proceeds through the legal system.

FERC has approved a settlement between Luminant Generation and the Texas Reliability Entity for violations of a regional reliability standard governing primary frequency response in the ERCOT region (NP26-2).

NERC submitted the settlement Nov. 26 in its monthly spreadsheet Notice of Penalty (SNOP); FERC said in a Dec. 23 filing that it would not further review the agreement. The settlement carries no monetary penalty.

Luminant’s settlement concerned violations of BAL-001-TRE-2 (Primary frequency response in the ERCOT region), a regional standard approved by NERC’s Board of Trustees in 2020 and approved by FERC the same year. (See “Standards Actions,” NERC Board of Trustees Briefs: Feb. 6, 2020.) Requirement R9 of the standard specifies the 12-month minimum rolling average value of each generating unit’s initial primary frequency response (PFR) performance, while requirement R10 sets the minimum sustained PFR.

The utility self-reported both violations, the first on Aug. 18, 2022. On that date, Luminant notified Texas RE that it had not set the required initial PFR at four generating units: Unit 1 at the Lake Hubbard gas plant, Unit 1 at the Odessa-Ector combined cycle plant, Unit 2 at the Oak Grove coal plant and the Castle Gap solar plant.

Lake Hubbard was the first to fall below the required value on Aug. 31, 2021. That unit and the Odessa-Ector unit have since been reset and returned to compliance; the other two were still noncompliant at the time the SNOP was filed, although mitigation efforts — including reviews of the plant controller logic and updates to turbine control and distributed control systems for Oak Grove and correcting high sustainable limit telemetry for Castle Gap — were ongoing. The SNOP did not provide an estimated date of completion for the mitigation.

Luminant reported its noncompliance with requirement R10 to Texas RE on June 30, 2023, notifying the regional entity that the average sustained PFR at Lake Hubbard 1, Oak Grove 1 and 2, and Castle Gap had fallen below the required value. Only Lake Hubbard had returned to compliance at the time of the SNOP. Similar mitigation measures to those for the R9 infringements were underway at the affected plants.

Texas RE assessed the root cause of both violations as ineffective detective controls — specifically a failure to “identify and correct issues with [Luminant’s] controller frequency response logic and other settings that affect PFR performance.” The RE wrote that the violation posed a minimal risk, observing that “the overall market frequency response in the Texas Interconnection is robust enough to ensure sufficient frequency response [was] available to respond to” frequency events despite the incorrect PFR settings.

Texas RE acknowledged the duration of the infringement, with some units having the wrong PFR value for several years, but wrote in the utility’s defense that the problem might not have been detected because detection requires frequency events that were rare in the area. For example, the RE observed that the last score recorded for Oak Grove 2 was in April 2023, and Castle Gap’s last recorded score was in June 2024. Texas RE also considered Luminant’s “robust” internal compliance program to be a mitigating factor in the penalty determination.

Finally, Texas RE acknowledged that Luminant has experienced prior noncompliance issues with the same requirements, but it determined that these incidents “should not aggravate the penalty” for two reasons. First, those violations were disposed of as compliance exceptions, which are not meant to be used as aggravating factors for a later violation unless it is considered a serious or substantial risk. Second, Texas RE determined that the mitigations for the previous violations would not have prevented the most recent issues because they affected different settings.

Commissioners also approved a separate SNOP concerning violations of NERC’s Critical Infrastructure Protection standards. Details of that SNOP were not made public in keeping with the commission and NERC’s policy against sharing critical energy/electric infrastructure information.

FERC rang out the regulatory year for SPP by accepting the grid operator’s tariff revisions establishing subregions for the cost allocation of future byway projects under its highway/byway methodology.

The Dec. 30 order decouples SPP’s Schedule 9 (zonal rates) and Schedule 11 (highway/byway) transmission pricing zones and creates five larger Schedule 11 subregions of existing zones (ER26-407).

Two-thirds of the cost of byway upgrades (between 100 and 300 kV) will be allocated to the subregion in which they are connected, with the remaining 33% allocated to the SPP footprint. New base plan upgrades larger than 300 kV will be allocated RTO-wide as highway projects.

SPP plans to group its 18 existing transmission pricing zones into five new Schedule 11 subregions: North, Nebraska, Central, Southwest and Southwest. The subregions will replace legacy pricing zones only to allocate costs for future byway facilities under Schedule 11 and will not affect Schedule 9 zonal boundaries or previously approved cost allocations.

The commission found that the RTO’s proposed modifications to the cost allocation for byway facilities “reasonably reflects that the transmission customers within a subregion use and benefit from these facilities.” It said SPP’s technical analyses demonstrate that the zones within each proposed subregion are significantly integrated based on their “complementary import/export patterns, significant inter-zonal connectivity, similar power-flow patterns and other operational interdependencies.”

FERC disagreed with protests filed by the Louisiana, Oklahoma and Texas regulatory commissions that SPP’s proposal was facially deficient and that it had not satisfied its burden under the Federal Power Act because the RTO failed to identify or quantify the proposal’s future cost impacts. The commission said SPP had met its burden to show the tariff changes comply with FERC’s cost-causation principle.

It also was unpersuaded by an assertion by the city of Springfield, Mo., that SPP did not demonstrate how the Regional Cost Allocation Review (RCAR) process would fairly evaluate cost-benefit imbalances under the proposed modifications. The RCAR reviews the highway/byway cost-allocation methodology every six years to analyze the effects on each pricing zone.

SPP’s proposal was approved by its board, state regulators and members in 2025. Several members pushed back over concerns about unreasonable cost shifts. (See “Members Pass Last of HITT’s 2019 Recommendations,” SPP MOPC Briefs: April 15-16, 2025.)

FERC disagreed, finding that the grid operator had “adequately demonstrated” that allocating two-thirds of byway facility costs to its subregion and the remainder on a regional load ratio share basis “allocates the costs in a manner that is at least roughly commensurate with the benefits of these facilities.”

SPP’s proposal was the last recommendation from the Holistic Integrated Tariff Team (HITT), which was created in 2018 to conduct a comprehensive review of the RTO’s cost-allocation model, transmission planning processes, Integrated Marketplace and real-time operations. After a year of discussion, the 15-person HITT published a report with 21 recommendations. (See HITT Shares Draft Report with SPP Stakeholders.)

The tariff change was hung up for several years by work on another HITT recommendation to adopt a policy creating an appropriate balance between cost assessed and value attained from energy and network resource interconnection service products and generating resources with long-term firm transmission service.

Vistra has signed a deal with Cogentrix to buy 5,500 MW of natural gas units in PJM, New England and Texas for $4 billion, the companies announced Jan. 5.

The deal includes three combined cycle plants and two combustion turbine facilities in PJM, four combined cycle facilities in ISO-NE and a cogeneration plant in ERCOT. Vistra is putting up $2.3 billion of cash, $900 million of stock and the assumption of $1.5 billion in debt, minus about $700 million of net present value in tax benefits.

“The Vistra team is excited to announce the acquisition of the Cogentrix portfolio, marking the second opportunistic expansion of our generation footprint over the past year to support our ability to serve growing customer demand in our key markets,” Vistra CEO Jim Burke said in a statement. “Successfully integrating and operating generation assets is a major undertaking, and our talented team continues to demonstrate that it is a core competency of our company.”

The new natural gas generator portfolio will help Vistra meet the growing demand of its customers, Burke said. He added that the company continues to look for additional opportunities to expand supply that meet its “disciplined investment thresholds.”

Cogentrix is owned by the energy-focused private equity firm Quantum Capital Group. The sale represents “substantially all of its portfolio,” Quantum CEO Wil VanLoh said.

“We are excited to become shareholders of Vistra and have much confidence in Vistra’s ability to deliver long-term value through its industry-leading portfolio and operational excellence,” VanLoh said in a statement. “Quantum thanks the Cogentrix team for their partnership and looks forward to seeing the business continue to grow as part of Vistra.”

Two of the plants — the Patriot and Hamilton Liberty combined cycle generators in Pennsylvania — are only majority-owned by Cogentrix, but Vistra is buying 100% ownership in them.

The plants are modern and efficient and add baseload capacity that complements Vistra’s existing units, the company said. The portfolio averages a heat rate of 7,800 Btu/kWh, while the Patriot and Hamilton Liberty plants are just 10 years old and more efficient at 7,000 Btu/kWh.

The capacity is in three of the most attractive and fastest-growing markets in the country, and once the deal closes, Vistra’s U.S. fleet will total 50 GW.

The deal needs approvals from FERC, the Department of Justice under the Hart-Scott-Rodino Act and some state regulators. Vistra hopes to close in 2026.

The Bonneville Power Administration has executed new long-term wholesale electric power contracts with more than 130 public utility customers under the agency’s Provider of Choice (POC) initiative, according to an announcement.

The new 16-year power purchase agreements with Northwest public utility customers were signed throughout the fall and are the product of a four-year effort to get contracts in place before existing agreements expire in 2028, according to a Dec. 23 news release.

“This is a watershed moment for BPA and our ratepayers,” agency Administrator and CEO John Hairston said in a statement. “With these contracts in hand, we have the continuity and certainty necessary to continue building and expanding the value of the federal power and transmission systems that deliver vital, low-cost and reliable electricity to millions of residential, commercial and industrial consumers and serves as a cornerstone of the Pacific Northwest’s economy.”

A recent study by Energy and Environmental Economics (E3) found that accelerated load growth and aging power plant retirements in the Northwest could create a resource gap starting around 1.3 GW in 2026 and expanding to almost 9 GW by 2030. (See 9-GW Power Gap Looms over Northwest, Co-op Warns.)

The news release did not mention the E3 study, but BPA said the contracts would provide a “sturdy financial base for Bonneville as it works to ensure the region is ready to meet the increasing energy demands in the near term and the future.”

With the contracts signed, the agency enters a three-year implementation period to begin power sales in October 2028. The implementation period includes calculating Contract High Water Marks, drafting Resource Support Services contract provisions and standing up associated systems and processes identified in the POC contracts, BPA spokesperson Kevin Wingert told RTO Insider on Jan. 5.

BPA will use the new Public Rate Design Methodology to establish rates under the BP-29 Rate Case expected to launch in fall 2027, according to the news release.

Bonneville delivers power to regional public power customers under contracts executed in 2008. The agreements provided approximately 76% of BPA’s power services’ revenue requirement in 2022, according to a concept paper. (See BPA Preparing to Deliver Power Under New Multiyear Contracts.)

The long-term contracts by statute cannot exceed 20 years, and BPA initiated the POC effort in 2021 to begin contract discussions with stakeholders before agreements expire in September 2028, according to the paper.

POC contracts are for BPA’s preference customers only, and no IOUs have signed an agreement. However, BPA developed the New Resource Rate Block Policy in August 2025, which outlines how an IOU could request service and what an agreement would include, according to Wingert.

The agency has launched other initiatives aimed at meeting the Northwest’s growing energy demand, the Dec. 23 news release noted.

For example, the agency is working to improve the power output for the Columbia Generating Station, a nuclear power plant. The agency said the modifications could result in additional output of approximately 160 MW by 2031.

Other efforts include investments in the Federal Columbia River Power System, such as high-efficiency turbine runners, generator rewinds and two new turbines, which the agency hopes could provide up to 330 aMW of additional energy for BPA customers.

The agency’s Grid Access Transformation initiative aims to make it easier for power producers to access the grid and shorten the construction time of new transmission lines. BPA is investing “up to $25 billion in transmission projects and reinforcements across the Northwest,” according to the news release. (See Utilities Back Some BPA Transmission Updates, Hesitate on Others.)

MISO is re-examining its longstanding policy that forbids stakeholders from recording meetings and is considering the possibility of some form of AI notetaking or transcription.

Counsel Jacob Krause told a Jan. 5 meetup of the Stakeholder Governance Working Group that MISO is investigating “tools” that would create a record of stakeholder meeting content. He promised more details after the RTO gathers its stakeholders’ opinions on the issue. It’s not clear if MISO would allow stakeholders to make their own recordings of meetings.

The grid operator prohibits anyone from recording meetings, save for a few self-recorded workshops throughout the year. In 2024, it banned the use of AI notetaking, and its Stakeholder Relations division has periodically expelled AI bots from meetings.

Multiple stakeholders voiced support for MISO’s re-examination.

Tyler Bergman, a senior manager of Clean Grid Alliance, said granting stakeholders the ability to review meeting discussions after the fact would help stakeholders balance their work and personal lives with MISO’s “very active stakeholder schedule.” He pointed out that CAISO records its meetings and makes the recordings and transcripts publicly available in a temporary archive on its website.

John Liskey, of the Citizens Utility Board of Michigan, said it’s difficult for his fellow members of the consumer advocate sector, including state attorneys general, to keep up with MISO meetings.

“It’s one thing to take notes, but it’s another thing to listen to a recording and really understand the dialogue,” Liskey said.

Mississippi Public Service Commission consultant Bill Booth said “several commissions in the South” would be interested in accessing transcripts of MISO meetings.

“We all take notes, but we don’t capture everything, so transcripts would be helpful,” Booth echoed.

But ITC Holdings’ Cynthia Crane said she has “strong concerns about changing historic practice” at MISO. Crane said conducting meetings with a recording device could have a chilling effect on discussion and lead to self-censoring and diminished participation in discussions. She said stakeholders could develop a “fear of misrepresentation and the use of sound bites” without context.

The Sustainable FERC Project’s Natalie McIntire disagreed that recordings would suppress discussion. She pointed out that MISO’s meetings are already open to the press, and reporters aren’t infallible and can misrepresent someone’s point. McIntire said stakeholders for years have been aware that they could be quoted while expressing their stances in meetings.

Liskey suggested MISO introduce a “trial period” of allowing recorded meetings and see if the practice dampens conversations.

WEC Energy Group’s Chris Plante said there’s perhaps a “middle ground” where, after MISO investigates notetaking tools, it allows summaries of meetings instead of verbatim transcripts. Plante said that way, stakeholders who inadvertently unmute themselves during meetings don’t have their embarrassing gaffes chronicled.

As if to illustrate the point, the teleconference was later interrupted several times by someone speaking in French.

MISO and stakeholders plan to again address the possibility of recording or allowing AI to summarize meetings at the April 20 meeting of the Stakeholder Governance Working Group.

The first time I heard an energy industry official mention the word “flexibility” was back in the early 2010s, when I was a fledgling energy reporter at The DesertSun in Palm Springs, covering the permitting and construction of an 800-MW natural gas power plant to be located north of the city. The Sentinel plant and its eight, 90-foot-tall emission stacks were needed for system flexibility, a representative from CAISO told me.

As more and more variable renewables came online ─ like the hundreds of wind turbines also located north of Palm Springs and the first utility-scale solar projects on federal land east of the Coachella Valley ─ flexible power that could come online quickly was critical, the official told me. And back then, fast and flexible meant natural gas.

Sentinel was a peaker ─ ideally used only to fill gaps in power supply at times of high demand ─ and was licensed to operate only one-third of the time. It could fire up in about 10 minutes, and according to an environmental impact report that I read in detail, could put up to one million tons of carbon dioxide per year into the region’s already polluted air.

(Despite its status as a major resort area ─ and home to one of the country’s largest music festivals ─ the Coachella Valley has notoriously poor air quality, due in part to the hundreds of diesel-powered 18-wheelers rolling through it daily on the Interstate 10 highway.)

CAISO ran its first demonstration projects using energy storage for system flexibility between 2014 and 2016 ─ after I left Palm Springs ─ but the results were impressive. I was in D.C. at the Smart Electric Power Alliance by then and remember another conversation with a contact at CAISO, who told me the storage was faster and more flexible than a natural gas peaker.

Ten years on, California has 17 GW of energy storage online, allowing the state to ride out summer heat waves ─ just one sign that flexibility has gone from marginal to mainstream. It also is a core attribute of the various scenarios and solutions being discussed to meet the snowballing estimates of U.S. electric power demand that drove headlines in the industry and mainstream media in 2025.

K Kaufmann

2026 is going to be all about how to further integrate flexibility as part of a clean, reliable and affordable electric power system. The technology is available, with prices going down and advanced capabilities expanding at speed and scale, powered by artificial intelligence. The lag, as ever, is on the policy and regulatory side.

The questions will be about what kind of new or different market mechanisms and regulatory guidelines will be needed to ensure the U.S. power system can take full advantage of all the different value and revenue streams flexibility can offer.

Specifically, regulators have yet to figure out how to fully integrate and compensate distributed technologies, like storage, which do not fit into traditional categories of supply and demand ─ generation and load, charge and discharge ─ and how these different technologies are rated on the grid.

But the typically glacial pace of regulation ─ with endless pilot projects and decisions often years in the making ─ is no longer tenable. Demand growth, rising electric bills and the need for system reliability and resilience are converging to accelerate the pace of change, with big tech hyperscalers ─ companies like Google building gigawatt-scale data centers ─ pushing all the various envelopes involved.

What is ahead will be exciting, uncomfortable and unavoidable for all stakeholders, including President Donald Trump and his supporters, who, despite all evidence to the contrary, are stubbornly clinging to fossil fuels as the primary solution for all the challenges of demand growth.

The Flex Front 2025

Any discussion of grid flexibility probably should start with a working definition. In grossly oversimplified terms, we know that our electric power system is overbuilt to handle periods of high demand that may occur only a handful of times each year, which means it often is grossly underused. That excess capacity can be optimized with grid-enhancing technologies ─ like advanced conductors and dynamic line ratings ─ which in turn can allow for the flexible integration of different forms of carbon-free generation and storage.

Further, electric power can be “flexed” at all levels of the system, from residential, commercial and utility-scale to distribution and transmission.

That flexibility in and of itself framed new and innovative views of the grid in 2025, beginning with a Duke University study, released in February, suggesting that if data centers were willing to curtail their electric use even .25% of the time, it would open up space on the grid for 76 GW of new generation. A curtailment rate of 1% could mean enough headroom to add 126 GW of new power.

The study has been widely cited, and Tyler H. Norris, its lead author, quickly became a much-sought-after speaker at industry conferences and webinars. In November, Google hired Norris to lead its market innovation and advanced energy initiatives.

Other key developments on the flex front included:

The July 29 virtual power plant demonstration in California: More than 100,000 residential batteries simultaneously discharged for two hours, from 7 to 9 p.m., pumping out 539 MW of electricity, or the equivalent of a mid-sized power plant. An analysis of the demonstration by The Brattle Group concluded that the aggregation of behind-the-meter solar and storage “can deliver reliable, utility-scale capacity at a significantly lower cost than traditional solutions.”

Energy Secretary Chris Wright’s Oct. 23 directive to FERC: Wright proposed new rules for the interconnection of “large loads” ─ that is, data centers ─ which would allow expedited approvals for co-location of centers and generation if power at such facilities could be curtailed or dispatched by a grid operator. FERC received more than 200 comments on Wright’s proposed rules, with hyperscalers in particular opposing any rule that linked expedited interconnection to curtailment controlled by grid operators or utilities.

The Electric Power Research Institute’s DCFlex initiative: Significantly, EPRI launched this new program in 2024, with the goal of developing data centers as flexible grid assets. A heavy-hitting list of project collaborators includes Google, Meta, Microsoft, Nvidia and Schneider Electric, along with major utilities, RTOs and ISOs. An interactive map on the DCFlex website shows that utilities in 41 states already have some kind of flexible load or demand management programs.

Clearly, everyone ─ even Chris Wright ─ knows that change is coming; flexibility will be a critical must-have, and those who are not ready or willing to innovate and invest will be left behind.

Above Politics

The physics, economics and politics of the next few years are well known. Estimates of the amount of new power the United States will need by 2030 increase with almost every new report. Back in February, the Duke University study estimated that data centers alone would drive 65 GW of new demand by 2029.

An ICF report from May called for 80 GW of new power to come online per year for the next 20 years, while in November, Grid Strategies upgraded an earlier estimate of 128 GW needed by 2030 to 166 GW.

The turbines that will power new natural gas plants could take years to deliver due to material and labor shortages and leave consumers vulnerable to the turbulence of natural gas prices. Renewables are cheaper and faster to build ─ and according to interconnection.fyi, still make up about 88% of projects sitting in interconnection queues nationwide ─ but face a virtual obstacle course as the Trump administration, RTOs and some utilities prioritize natural gas and nuclear.

Natural gas and renewables also will require new transmission and streamlined, accelerated permitting, all of which, including new data centers, are likely to face local opposition.

And electric bills are going nowhere but up ─ period. The ICF report estimates that residential rates could rise 15 to 40% by 2030, depending on the region.

Flexibility redefines everything and, again, is available immediately with existing technologies, which will get cheaper and smarter with speed and scale. This is why it will be essential for system evolution at all levels in 2026.

Flexibility turns grid-edge renewables from variable or intermittent to flexible and dispatchable resources that can shave peak demand, as seen in California’s VPP demonstration. Homes, businesses and data centers all can serve as flexible grid assets, which can help cut electric bills and drive behavioral change.

Consumers increasingly will see the value of adopting technologies that combine energy efficiency with flexibility ─ like solar and storage ─ so they can participate in even more sophisticated demand management programs.

In addition, upgrades that make existing transmission and distribution systems more flexible could allow for more distributed renewables, while triggering less local NIMBYism and reducing the need for new fossil-fueled generation.

In other words, flexibility is a no-brainer. It is above politics, and it just makes sense.

Fail and Scale Fast

President Trump notwithstanding, clean energy will continue to grow ─ though at a slower rate ─ in 2026 because it is faster, cheaper, cleaner and more flexible than fossil fuels. But the more significant paradigm shift this year will be toward policies, again at all levels, that promote the adoption of flexible technologies, ensure they are valued and compensated appropriately and accelerate permitting.

While Trump and some major players in the industry frame the current crunch in demand growth as an “energy emergency,” it actually is a long overdue and extremely cool opportunity for the electric power sector to reinvent itself. It has been dragging its feet on a 21st-century makeover, while its customers increasingly move at the blistering speed of AI.

High-tech hyperscalers are setting the pace. They want power, speed and flexibility for their data centers. They have the technology, the experts and the money to invest in system change; they know how to fail and scale fast; and they do not like waiting for regulators or utilities unless they absolutely must.

Interconnection policies have become the front line of change, where expedited approvals for projects turn on their ability and willingness to flex their power. Texas pioneered this kind of “conditional interconnection,” now codified via SB6, signed into law in June. California followed suit in August with its Limited Generation Profiles policy, which limits the amount of power distributed projects can export to the grid at times of system stress.

What is particularly exciting here is the implicit acceptance of flexibility as a central attribute of the grid and how that in and of itself redefines reliability and resilience.

PJM will provide the acid test of this approach as it works to comply with FERC’s recent order requiring an overhaul of the RTO’s interconnection policies for new generation co-located with data centers. In particular, the order requires PJM to adopt rules and the associated tariffs for co-located generation that can self-curtail or flex its demand on an interim or regular basis. (See FERC Directs PJM to Issue Rules for Co-locating Generation and Load.)

Any final rules from FERC promoting flexible interconnection should send a signal to other grid operators, states and utilities. Wright’s directive called for the federal regulators to complete work on his proposed rules by April, which would be warp speed for the commission, especially given the many concerns raised by stakeholders.

Demand management also is going to move fast. With Tyler Norris on board, we can expect to see new initiatives in this area from Google, which has signed flexible demand agreements with the Tennessee Valley Authority and Indiana Michigan Power. Meanwhile, Amazon is promoting grid-enhancing technologies as a way to get more renewables online.

Building on California’s demonstration, 2026 will see a ramp in VPPs. A recent article in Energy Storage News details three new VPPs being launched by a range of developers and utilities in California, as well as in Texas, Washington, Arizona and the Tennessee Valley. One example is a new partnership between software developer Leap and independent power producer Enel North America that aims to connect commercial distributed resources to utility demand management programs.

Why is any of this important? As flexibility becomes the new normal, it makes us think about electric power differently. It redefines our relationship to how we produce it, how we use it and what we can do with it. It makes us aware that we as consumers have an active role to play here, and that we can do more than complain about rising electric bills and then pay them.

Let us also remember that when we talk about flexibility and renewables, we are talking about climate change and reducing greenhouse gas emissions, whether we use the actual words. We have shifted from an environmental to a practical, business case for climate action, which is equally if not more effective.

Coming full circle, in 2024, the Sentinel plant was approved for a 17.18-MW, 34.36-MWh battery storage system to provide black start capability, so the plant can restart itself even if it goes offline.

When peakers need extra flexibility, we are way past the point of no return; 2026 is going to be a good year.

PJM enters 2026 amid several efforts to ward off a reliability gap attributed to accelerating data center load, sluggish development of new capacity and resource deactivations.

The risks were laid bare in December, when the 2027/28 Base Residual Auction cleared 6.6 GW short of the reliability requirement. Of the 5,250 MW of load growth included in the auction, the RTO attributed nearly 5,100 MW to data centers. (See PJM Capacity Auction Clears at Max Price, Falls Short of Reliability Requirement.)

With six months remaining before the 2028/29 BRA is to be conducted in June, PJM’s Board of Managers is considering how to proceed in the wake of a Critical Issue Fast Path (CIFP) proceeding focused on large load interconnections. Stakeholders brought forward a dozen proposals, none of which received sector-weighted support from the Members Committee on Nov. 19. During the committee’s meeting Dec. 17, board Chair David Mills pushed the target for a FERC filing to January to allow more time to go through the packages. (See PJM Stakeholders Reject All CIFP Proposals on Large Loads.)

The rejection of the proposals puts the board in a similar position to when the RTO conducted a CIFP in 2023 focused on resource adequacy, when 20 packages were rejected. Because the committee’s vote is only advisory, the board could choose to proceed with any of the options, cobble together elements of them or arrive at its own solution. PJM staff’s recommendation included a request for a second phase of the CIFP to evaluate changes to the reliability backstop and incentives for load flexibility.

The board is weighing its options against the backdrop of a FERC order directing PJM to revise its tariff to include at least four options for large loads co-located with wholesale generation to receive transmission service. It also directed the RTO to provide a report on the CIFP within 30 days of the Dec. 18 order. PJM has scheduled a workshop to discuss the co-location order Jan. 9. (See FERC Directs PJM to Issue Rules for Co-locating Generation and Load.)

Proponents of co-location have argued it allows for more efficient siting of load, reducing the need for transmission upgrades, while skeptics say it would push transmission and ancillary service costs, such as black start, onto other consumers. Independent Market Monitor Joe Bowring and several other stakeholders have argued that if loads are considered critical national security interests, it’s unlikely they actually would be required to curtail or accept non-firm service.

Further complicating the board’s deliberations is a complaint the Monitor has filed with FERC arguing that PJM has the authority to delay large load interconnections that would jeopardize transmission security or resource adequacy (EL26-30). It argued that the recommended CIFP proposal — and PJM’s statements throughout the process — are based on an untested theory that the jurisdictional contours that RTOs operate within do not allow them to require that a load can be served reliably before it is permitted to enter service. (See Market Monitor Files Complaint Over PJM Large Load Interconnections.)

Several Design Changes for June Auction

Several design changes are to affect the 2028/29 auction, including the elimination of a price collar established by a settlement with Pennsylvania Gov. Josh Shapiro (D); the implementation of FERC Order 2222 requiring RTOs to facilitate the participation of distributed energy resources; and the expiration of a measure allowing PJM to model some deactivating resources operating under reliability-must-run agreements as providing capacity. The 2029/30 BRA is scheduled for December 2026.

The price cap was effective for the 2026/27 and subsequent auction, limiting prices to between $175 and $325/MW-day, with adjustments before each to account for shifting accreditation values for the combustion turbine reference resource. The temporary nature of the agreement was intended to avoid high prices while several market changes are implemented. Supporters argued the RTO’s backlogged interconnection queue would prevent developers from responding to high prices.

During a press conference following the posting of the 2027/28 auction results, PJM Executive Vice President of Market Services and Strategy Stu Bresler said staff plan to proceed with the 2028/29 BRA with the auction parameters proposed in the RTO’s Quadrennial Review filing. (See PJM Board of Managers Approves Quadrennial Review Proposal.)

A joint proposal from the Data Center Coalition, Exelon and PPL, as well as the governors of Maryland, New Jersey, Pennsylvania and Virginia, would extend the collar by one year, in addition to adding financial requirements for large loads, creating a demand response product with limited annual run hour restrictions and loosening the participation requirements for the expedited interconnection track proposed by PJM. (See “Data Center Coalition, Utility and Governor Proposal,” PJM Stakeholders to Vote on Large Load CIFP Proposals.)

The governors, along with those of Delaware and Illinois, signed a letter encouraging the board to include an extension of the collar in the CIFP solution it accepts.

The commission’s approval of PJM including the 1,289-MW Brandon Shores and 397-MW H.A. Wagner in the capacity supply stack is also to end prior to the 2028/29 auction. Its temporary nature was similarly intended to allow resources that consumer advocates argued can operationally serve as capacity to be modeled as such while stakeholders pursue a more holistic approach to how RMR resources are reflected in the capacity market. PJM has said it intends to request a one-year extension of FERC’s approval. (See “PJM Plans to Request 1-year Extension of RMR Resources Participating in Capacity Market,” PJM MIC Briefs: Oct. 9, 2025.)

The Deactivation Enhancements Senior Task Force is continuing discussions on a pro forma RMR agreement that would allow the RTO to dispatch relevant resources during a capacity emergency.

The proposal would rework the design of the variable resource requirement (VRR) curve to set the maximum price at the larger of either 20% of the gross cost of new entry, or 115% gross CONE minus 75% of the net energy and ancillary services (EAS) offset. The formula establishes a floor meant to prevent high energy market revenues from lowering the maximum capacity price to zero. The curve approved by the commission in 2023 set the maximum at the greater of gross CONE or 1.75 times net CONE, which subtracts the EAS offset from gross CONE.

Jointly proposed by PJM staff and Pennsylvania Public Utility Commission Vice Chair Kimberly Barrow, it is meant to improve the stability of the VRR curve by reducing reliance on multipliers of the CONE parameter. The curve defines the clearing price to be procured in a BRA and at what cost.

The reference resource would remain a combustion turbine, though PJM’s initial proposal would have shifted to a combined cycle generator for all regions except in ComEd, where a four-hour battery electric storage system would be the reference. (See “Stakeholders Divided on Reference Technology,” PJM Stakeholders Discuss Quadrennial Review Proposals.)

The filing has been opposed by the Monitor, which took issue with PJM’s VRR curve shape, and the Maryland Office of People’s Counsel, which sought a Federal Power Act Section 206 investigation into the functioning of the RTO’s capacity market.

The Monitor disputed PJM’s calculation of gross CONE for the reference resource and argued the proposed VRR curve would inflate capacity costs by $6.7 billion, instead recommending a steeper curve.

The OPC argued that PJM’s filing would result in uncompetitive market outcomes so long as developers cannot respond to high prices because of a confluence of the compressed auction schedule, the amount of time it takes projects to clear the interconnection queue and national supply chain shortages. It argued the commission should investigate the capacity market and extend the maximum price set by the proposal until it determines “new entry imposes constraints on the potential exercise of market power.”

Transition to Cluster Cycles to Complete

PJM is about halfway through processing projects being studied in Transition Cycle 2 of its interconnection queue, which is in the second of three phases. Interconnection service agreements are to be negotiated between December 2026 and February 2027.

The cluster-based approach for studying the network upgrades needed for new resources and how costs are allocated is to begin with its first cycle once the April 27 application deadline expires. Reviewing the applications will take a few months, and models are to be posted in June. The total cycle is expected to continue through April 2028.

The shift is intended to allow projects to proceed through the queue more quickly and give developers more certainty about the costs they may face. The backlogged queue has been blamed for holding back new resources, particularly renewables, contributing to the imbalance of supply and demand. Since it implemented its transitional process, PJM has said it is processing more projects than ever — including 306 interconnection requests when Transition Cycle 1 was completed in 2024. (See PJM Reaches Milestone on Clearing Interconnection Queue Backlog.)

Leadership in Flux

PJM leadership is in a moment of transition going into 2026, with two new board members appointed in September and Chair Mills assuming the interim CEO position for “several months” as the search continues for a long-term executive. (See PJM Members Confirm 2 Board Nominees; States Call for Governance Overhaul.)

Speaking during the Dec. 17 MC meeting, Mills said PJM was “incredibly fortunate” to attract outgoing CEO Manu Asthana in 2019, as the leading indicators of the challenges the RTO would face began to emerge. (See PJM Taps Ex-Direct Energy Exec as New CEO.)

Asthana recalled being gifted a firehose at his first MC meeting, which he called a fitting sign of what was to come. He said Mills is more than ready to take over and has his full confidence.

Several governors of PJM member states have pushed the RTO to rework its governance structure to provide more of a voice for the states in its decision-making. Following a multistate technical conference in September, they issued a statement of intent to form a PJM Governors’ Collaborative to “promote greater state and consumer representation in the governance and decision-making processes of PJM.” (See Governors Call for More State Authority in PJM.)

The participation of governors’ offices and state legislators in PJM’s stakeholder process deepened throughout the CIFP, and Pennsylvania separately sponsored an issue charge to explore a sub-annual capacity market design. The Analysis Group presented the preliminary results of its report on such a design to the Sub-Annual Capacity Market Senior Task Force at its Dec. 12 meeting. Monthly task force meetings are scheduled through June.

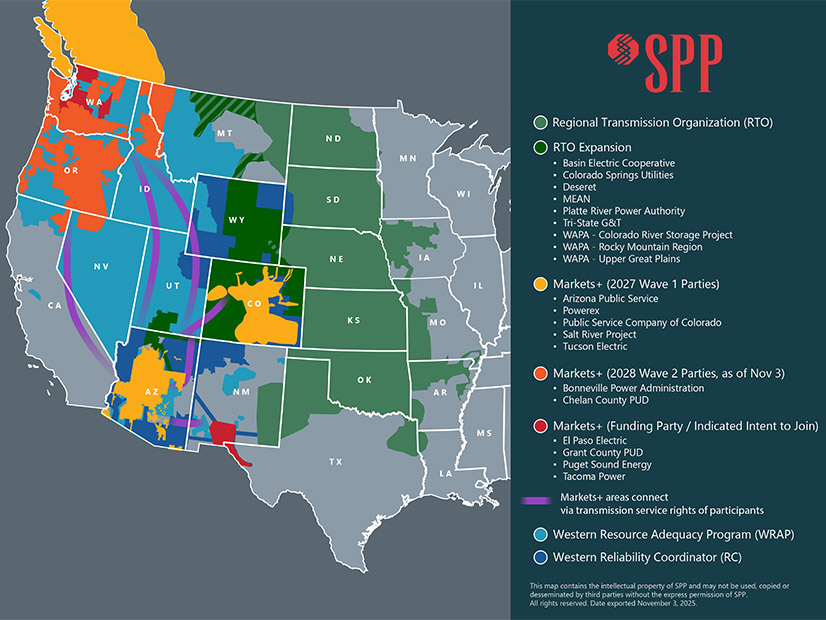

SPP has made it official: The operator of the sprawling Midwestern grid technically is in the Western Interconnection.

That means it has office space in downtown Denver that includes a sizeable meeting room, a break room and several offices with three workspaces. That allows SPP to boast a “physical presence” in the West, as one staffer said.

In April, it’s scheduled to become operational. That’s when the grid operator’s 14-state footprint will increase by three. Utilities from Arizona, Colorado and Utah will place their facilities under SPP’s tariff. It will make the grid operator the first to provide full market services in the U.S. system’s two major interconnections, thanks partly to three DC interties totaling 510 MW.

The expansion comes little more than a year after FERC approved an amended tariff that adds the western members to the RTO and drew praise from several commissioners. Judy Chang said the approval is “another major milestone for the market evolution in the Western part of the U.S.” (See FERC Approves Tariff for SPP RTO West.)

All seven members of RTO Expansion — as SPP refers to its new market on the other side of the Rockies — currently participate in SPP’s Western Energy Imbalance Service market; four of them (Basin Electric Power Cooperative, Municipal Energy Agency of Nebraska, Tri-State Generation and Transmission Association, and the Western Area Power Administration’s Upper Great Plains-East Region) are members of the legacy RTO in the East.

A 2022 Brattle Group study for SPP determined the expansion will produce between $68 million and $81 million in annual Westside adjusted production cost benefits and wheeling revenue. Eastside members will see between $3 million and $8 million of those benefits.

SPP says it will decide Feb. 2 whether to launch the market April 1 as planned.

“Right now, everything seems to be on track,” CEO Lanny Nickell told his board in November.” We’re looking forward to working with our new members in the West.”

The RTO expansion has been somewhat overshadowed by the noise surrounding SPP’s Markets+ day-ahead offering, which is providing Western utilities an alternative to CAISO’s Extended Day-Ahead Market.

The grid operator’s staff and Markets+ stakeholders are well into the initiative’s second phase, working together to build the market’s operating systems and conduct market trials and parallel operations. SPP says 41 entities have committed to covering the market’s $150 million in development expense; the costs will be recovered through future operations. (See SPP Markets+ Cruising Through Early Development.)

Interested market participants have until April 1 to register. They will have about 45 days to complete their registration workbook.

Arizona Public Service, Powerex, Public Service Company of Colorado, Salt River Project (SRP) and Tucson Electric Power are moving forward as balancing authorities. The Bonneville Power Administration will join the secondary market launch in October 2028, along with four other Pacific Northwest BAs.

SPP is targeting October 2027 as the Markets+ go-live date. When the Northwest BAs join in 2028, it will consist primarily of the Pacific Northwest, Desert Southwest and along the Rockies.

The series of complicated seams that will result have caught the attention of FERC, which has asked Western stakeholders to get ahead of seams issues before the markets launch. SPP, experienced in managing seams with MISO, ERCOT and WECC, is hosting a Western Seams Symposium open to western stakeholders at SRP’s Tempe, Ariz., headquarters Feb. 26. (See FERC Report Urges West to Address Looming Market Seams Issues.)

SPP’s western expansion effort is just one of its three overarching goals. The others are accelerating its generator and large load interconnection processes and mitigating its resource adequacy risk.

The grid operator will begin transitioning in 2026 to its Consolidated Planning Process, which combines its transmission planning and GI studies into a three-year process that aligns system modeling, planning assumptions and cost allocation across load and generation needs. The CPP’s “ready-to-go” construct replaces the current “request-then-analysis” framework by identifying system needs and costs before the generator asks to connect. (See SPP ‘Blazes Trail’ with Consolidated Planning Process.)

A transition study is underway and will result in a 20-year assessment in November 2026. The 2027 study will sunset the current process and integrate RTOE transmission needs before the first full CPP 10-year assessment in 2028.

The studies will be run in parallel with a strategic partnership announced during the summer between SPP and global tech giant Hitachi. The two organizations are collaborating to accelerate the GI process by reducing study times 80% through end-to-end industrial AI and advanced computing infrastructure. (See SPP, Hitachi Partner to Use AI in Clearing GI Queue.)

Several other 765-kV projects were set aside as SPP, like other grid operators, prepares for a future projected to be dominated by data centers, crypto miners and industrial electrification. A more recent Brattle Group study found the RTO will require at least $88 billion and up to $263 billion of generation investment to support load growth through 2050. (See SPP Study: $88-263B in Generation Needed by 2050.)

Naturally, affordability is a concern for regulators and other stakeholders. SPP has created the Cost Control and Allocation Review and Evaluation (CARE) Team, a cross-functional leadership body to review and recommend refinements or alternatives to the current transmission cost controls and cost-allocation methodologies. The team met once in December 2025 and took a deep dive into SPP’s various cost mechanisms; it has set a meeting schedule that lasts into November 2026.

“As I’ve been saying now for five years, PJM is heading for a reliability crisis, and now we’re there,” former FERC Chair Mark Christie said in an interview. “It’s no longer over the horizon. It’s right on the street with us, and the latest capacity auction results just drive home how bad the crisis is, when they fall short 6 GW of meeting the reliability requirement.” (See PJM Capacity Auction Clears at Max Price, Falls Short of Reliability Requirement.)

The primary driver for that crisis is the demand from new data centers, which has so far not been met with new generation to match it, he added.

“Really the problem is financing more than anything else,” Christie said. “We’re not getting large baseload generation built. We’re not getting combined cycle gas, which is the baseload generator of choice.”

Coal plants are not feasible at this point, and nuclear is not going to be ready at scale in time to meet the demand from data centers plugging into the grid soon, Christie said. Wind and solar, which dominate the queue, add much needed electricity to the grid, but they cannot be counted on to serve demand from data centers that want 99.999% reliable power, he said.

Christie’s home state of Virginia is a major contributor to the issue because it is home to the largest data center market in the world, Data Center Alley, and has contributed to the demand growth recently by plugging in new facilities that are ultimately served by imports from elsewhere in PJM.

“The Dominion zone was a big contributor to the deficit,” he added. “And we’re going to see whether the new governor and the new legislature are going to take action to try to get large baseload generation built.”

The supplies being added to the grid are either wind and solar or combustion turbines, and Christie is skeptical that the market on its own can add new baseload plants.

“I don’t know how high prices have to go to get large baseload generation built, but politically, you’re already getting a huge backlash because we’ve hit three all-time highs in the capacity market,” Christie said. “And we’re not getting large baseload generation announced.”

Virginia is one of the vertically integrated states in PJM, which means its political establishment needs to support the construction of new baseload, Christie argued.

“When I was on the Virginia commission, we approved four combined cycle natural gas generation units for Dominion, and every one of them got built,” Christie said. “Every one of them was ratebased, but the political leadership was supportive.”

PJM sits on top of huge supplies of natural gas in the Marcellus and Utica shale fields, which could power a new wave of combined cycle units.

“In the deregulated states, where they do not allow utilities to own generation, the question becomes: Who is going to build the large new combined cycle gas?” Christie said. “Are the [independent power producers] going to build it? We haven’t seen announcements of that.”

The Paradise Combined Cycle Plant in Drakesboro, Ky. | TVA

When states restructured their industries a quarter-century ago, PJM had excess supply, and the generators in those states were forced to sink or swim in the market, Christie recalled. Many sank, and it brought the reserve margins down for demand growth to return in a way no one expected.

“Now we’re in a perfect storm that, frankly, at the beginning of capacity market 20 years ago, nobody saw,” Christie said. “Nobody saw the explosion of demand coming from data centers 20 years ago.”

The capacity market was put in place at a time of wide reserve margins and slow, steady load growth. Ultimately, Christie thinks the states will have to address the issue on both sides of the supply and demand equation.

“The answer is really at the state level, not FERC,” Christie said. “The states have to deal with the demand side, with how they interconnect these large new data centers, and the states have got to deal with the supply side and getting generation built.”

Will the Market Respond?

Electric Power Supply Association CEO Todd Snitchler said the market will respond because PJM has now had three capacity auctions in the past year that have cleared at high prices.

“We’ve seen almost 12,000 MW of new generation that’s expected to be added to the PJM grid between now and roughly 2030,” he said.

EPSA and a fellow IPP trade group, the PJM Power Providers, created a chart showing all the projects, including uprates and new builds, that have been committed to serve load in the market. They argued that market participants should continue responding to the higher market prices seen in the last auctions, even though they have been muted by a cap that the RTO agreed to after a complaint from Pennsylvania Gov. Josh Shaprio (D). (See PJM, Shapiro Reach Agreement on Capacity Price Cap and Floor.)

“I think the compressed timeline of the auction has made it appear that the market is slower to respond,” Snitchler said. “But you know, you don’t drop a $2.5 [billion] or $3 billion investment in six months, or even maybe 12 months. And so, I think you’re going to see people who have had some time to digest the auction results lead to outcomes that are going to include that new generation that everyone wants to see.”

Before the July 2024 auction, the previous three cleared at low prices that were effectively signaling generators to retire just before the issue of meeting demands from new large loads like data centers started to become a reality, Snitchler said.

“As you see real load growth for the first time, really in probably 30 years, it’s triggering a response, and that response takes a little time to develop,” Snitchler said. “You’re already starting to see where there is incremental investment and new investment being made in PJM, but also in other parts of the country.”

The issue of rapidly rising demand leading to narrowing reserve margins is not unique to restructured markets, with vertically integrated states in MISO and SPP facing the same issues, he noted.

“It’s really a systemic issue that we’re all trying to address and resolve because everybody wants to make sure that we ensure, first and foremost, a reliable system that is also cost-effective and affordable,” Snitchler said. “I mean, if those two tenets aren’t met, then the rest of this is academic. We have to be sure that we’re meeting those two objectives.”

The load growth the industry is facing is different from that of the past, which was driven by economic and population growth. The new large loads are clustering in specific submarkets like Arizona, central Ohio and Loudoun County, Va.

Data centers might have plans to ultimately consume the same amount of power as a major city, but generally they do not immediately plug into the grid seeking to consume a gigawatt.

“There’s a construction ramp where they start from zero, and then you have that first tranche where you need to power it up,” Snitchler said. “Then they add the next phase until they’re finally complete.”

That gives the industry some time to respond to the load forecasts, which Snitchler argued are overstating future demand. While the power sector has limited supply chains for components like combustion turbines, the tech industry has a limited capacity to build the advanced chips needed for artificial intelligence-related data centers springing up around the world.

“If you look at the number of chips that are available from Nvidia and the fact that they’re sold out for the next couple of years, and there’s only 60 GW of new energy demand from those chips globally, [and] if you look at what is being projected in PJM and Texas, it would require every chip that Nvidia is going to sell for the next two years and more, and that’s not how that’s going to work.”

Utilities have also issued optimistic load forecasts that reflect plans for data centers that are not going to be built, Snitchler argued. When AEP Ohio put in place a new tariff for large load customers, it saw a pipeline of 30 GW of data centers cut down to 13 GW, and it’s not clear if all those will come to fruition, he said.

“They’re clearly an effective advocacy tool if you want to secure the ability to ratebase new generation, because ‘nobody’s moving as fast as a utility could.’ … I’ve never heard anyone say [that], but that’s the story that’s being told,” Snitchler said. “Then you need to have as big a number on your load forecast as possible, because that means you’re the solution to the problem that you’re creating.”

Multiple utilities have pushed for restructured states in PJM to change their laws and allow them to ratebase new generation for the first time in 30 years, which is an idea that EPSA is opposed to, arguing it would spoil the markets its members rely on.

“I understand they have a target earnings goal that they have set for Wall Street,” Snitchler said. “But that doesn’t mean that we should reverse 30 years of policy to help them achieve it when there are more cost-effective and more efficient ways to do that, and by putting the risk where it’s been for the last 30 years on shareholders and investors of competitive power suppliers.”

The Slippery Slope of Re-regulation

Ultimately if states change the laws and guarantee rates of return for new utility-owned generation, that would cut into the revenues of market generation owned by IPPs who would eventually ask for their own guaranteed rates — unwinding markets altogether, PJM Independent Market Monitor Joe Bowring said in an interview.

“If PPL builds power plants and puts them in rate base, then all customers are paying for them,” Bowring said. “There’s nothing stopping PPL from directly working out a bilateral agreement with the data center and building a power plant for them. But that’s not what they’re asking to do. They’re asking to put in rate base and charge everybody for it, and that’s just a way of making everyone else bear the costs and risks of the data center load.”

PJM’s markets have been slow to add generation in part because of overhanging issues from the interconnection queue and unstable market design in the capacity market, Bowring said.

“The developers who were caught up in all those delays had delayed getting some of their basic milestones,” Bowring said. “They’re now trying to catch up, but they’re behind, and that’s part of the reason we haven’t seen a lot of new additions.”

On top of the lingering issues from the queue, the capacity market has seen its rules change often, and Bowring is also skeptical of how the RTO has implemented effective load-carrying capability ratings for power plants.

“If data centers want to come online quickly — which is fine, we want them to come online quickly — they should figure out how to bring their own generation,” Bowring said. “That doesn’t mean you’re turning data centers into power plant operators. You sign a bilateral contract with a developer; they build the power plant. They manage all that for you, but you have power, and that’s the quickest way to get things going, because the data centers have a huge incentive to get power quickly.”

Some of the hyper-scalers in the data center world can build their own power plants. Google parent Alphabet announced Dec. 22 that it was buying Intersect, which develops power plants for new large loads. But not every data center developer is among the largest companies in the world by market capitalization.

“The market is going to take a little while to react, and I’m hoping that in a few years that will restore equilibrium,” Bowring said. “But at the moment, as you know, we’re something like 6,600 MW short.”

While meeting new load has always been a key part of the business, the scale of the new demands from data centers is unprecedented.

“We’re talking 30[,000] to 60,000 MW of demand,” Bowring said. “That is absolutely unprecedented,” and it’s amid “a time when PJM was getting tighter for other reasons. That confluence is, I think, absolutely unique. I mean, PJM has been long for almost forever.”

The last time the PJM region faced a major shortage was decades before it was an RTO, and the power pool was dealing with the aftereffects of the accident at Three Mile Island in 1979, he added.

The issues data centers present to the grid are unique, and they need to be handled differently than load growth was in the past, Bowring said.

“The whole notion of just plugging in is naive, almost willfully naive, in some cases,” Bowring said. “I understand why the data centers imagined a few years ago [that] they could just plug into the grid and everything would be fine, but everyone knew at least a couple years ago that that was not going to work longer-term; that it was simply overwhelming the grid. So, it has to be dealt with in special and targeted ways.”