Discussion about potential changes to the NYISO demand curve reset (DCR) process dominated a recent Installed Capacity Working Group meeting and will likely take up more oxygen in stakeholder meetings throughout the coming year.

“This project has the potential to deliver transformational changes to the market in the face of evolving grid conditions,” Michael Ferrari, NYISO market design specialist in capacity and new resource integration, told the working group Nov. 17 in presenting the project’s kickoff.

The Capacity Market Structure Review project identified the DCR as an area that needed improvement. The improvement project was prioritized for 2026, meaning NYISO has budgeted resources and labor hours for it.

Stakeholders have long complained that the DCR does not provide adequate price signals for new investment, value reliability contributions or provide sufficient consideration of long-term reliability impacts. During the latest DCR, stakeholders debated whether NYISO’s preferred proxy unit, a two-hour battery system, was appropriate or reflective of what might enter the market. In addition, stakeholders said the DCR has a steep learning curve, requires a lot of stakeholder engagement and provokes contentious debates during working group meetings.

Though Ferrari’s presentation noted all these concerns, “it doesn’t seem like the concerns expressed by Con Edison are in here,” a representative of the company said. “There have been multiple conversations on our end about concerns of higher costs to customers.”

Ferrari said stakeholder feedback highlighted in his presentation was “not a comprehensive list,” though the omission of price considerations was indeed an accident.

The presentation indicated NYISO would study how to improve or refine the definition of the proxy unit used to undergird the DCR process. The ISO also would look at restructuring the development of the net cost of new entry of the proxy unit, which sets prices for the curve; look at alternative curve slopes; and possibly develop a technology-agnostic approach to net CONE.

Stakeholders asked what a “technology-agnostic approach” meant with respect to net CONE. Ferrari said it meant NYISO was considering not choosing one specific unit to serve as the proxy for new generator entry to the market.

The ISO plans to issue a draft Issue Discovery Report at the ICAP Working Group’s Dec. 16 meeting. It will present the group with a detailed proposal of initial market design enhancements for consideration at a later meeting.

In New England, increasing winter reliability concerns are driving questions about how long the region’s aging fleet of oil-fired power plants can, or should, remain on the system.

Power generation from oil has declined dramatically in New England since the start of the century. The oil plants that have remained on the system have run less frequently, mostly during tight winter periods when gas generators have limited access to pipelines.

Several high-profile oil units have already retired, and the large oil resources that remain face significant retirement risks.

Continued reliance on aging oil generators has real consequences: The units are among the dirtiest in the ISO-NE resource mix, both in terms of climate-warming emissions and local air pollution that can have significant health effects on nearby residents.

But ISO-NE forecasts that growing winter demand, coupled with obstacles to offshore wind development and limits to the region’s gas supply, will increase the need over the next decade for dispatchable generators with fuel storage capabilities. This may force the region to keep the units online longer than many policymakers hoped, or to invest in adding dual-fuel capabilities to existing gas-only units.

Uncertainty remains, however, around when a significant spike in winter demand will materialize. And changes in the wholesale markets — including ISO-NE’s ongoing capacity market overhaul, evolving Pay-for-Performance risks and the introduction of longer-duration reserve products — could also have significant effects on plant revenues, making it difficult to predict how long the resources will remain online.

“You see a lot of the owners of some of these oil facilities caught in between and not being able to see a clear picture as to whether the ISO, the states and other policymakers want to try to preserve those facilities or drive them into retirement,” said Dan Dolan, president of the New England Power Generators Association.

“A lot of them have been driven into retirement or been driven into a place in which they are right on the cusp of financial viability,” he said. “I, at this point, don’t have a clear line of sight as to how some of those standalone large steam units are going to function.”

Changing Economics

The New England oil fleet is old: Most of the oil-fired steam units were built in the 1970s. As cheaper, cleaner and more efficient sources of energy have come online, oil generation has declined dramatically, dropping from 18% of the total energy production in 2000 to 0.3% in 2024, according to ISO-NE.

The steepest decline occurred between 2000 and 2010. Over the past 10 years, annual oil generation has fluctuated, often following the severity of winter conditions.

But the region has continued to see retirements and a declining amount of oil capacity on the system. Between Forward Capacity Auctions 15 and 18, capacity supply obligations for generators running on distillate and residual fuel oil declined from over 4,700 MW to about 3,500 MW.

“Many of these units are at risk of retirement,” ISO-NE noted in its draft 2025 Regional System Plan. “They run infrequently, are less efficient and are nearing the end of their economic life.”

As the resources have run less frequently, they have become more reliant on capacity revenues, while low capacity clearing prices have pushed higher-priced generators out of the market, according to ISO-NE’s Internal and External Market Monitors.

Potomac Economics, ISO-NE’s External Market Monitor, wrote in its 2024 annual report that “the sustained low prices led to 760 MW of retirement bids from units with on-site fuel supplies clearing in FCA 18,” which applies to the 2027/28 capacity commitment period (CCP).

With essentially no dispatchable generating resources in the region’s interconnection queue, “it will be critical to retain a large share of the existing dispatchable generation and avoid mandating retirements of fossil fuel resources,” Potomac wrote.

ISO-NE analyses have “made it clear that we need dispatchable resources, and we need a fairly significant quantity of readily available fuel for those dispatchable resources,” said Brian Forshaw, principal at Energy Market Advisors and a longtime NEPOOL participant. He emphasized that his comments are not on behalf of any of his clients.

“The challenge is going to be how to identify what the value of retaining that capability is, and then developing some kind of a market mechanism, or a reserve product or whatever else to compensate them enough to keep them around,” he added.

ISO-NE’s Capacity Auction Reform (CAR) project, a major multiyear effort, is intended to help better align capacity procurements with actual reliability benefits.

The project proposes transitioning the RTO from a forward, annual capacity market, with auctions held three years prior to the relevant CCP, to a prompt, seasonal market, with auctions held about a month prior to each CCP, which would be divided into winter and summer seasons.

The effort also includes significant changes to how much capacity value ISO-NE assigns to different resource types. Under the current rules, the capacity market typically accredits resources based on an audited value intended to capture the maximum output they can provide. The methodology does not account for outage rates and maintenance requirements, which ISO-NE instead factors into its calculations for the installed capacity requirement.

Under the proposed CAR changes, resources would be accredited based on their marginal reliability impact value, which is intended to capture contributions to reducing energy shortfall during extreme model scenarios. Accreditation values would account for a wider range of factors, including resource outage rates, maintenance requirements, stored fuel and intermittency.

The changes could have major implications for the capacity revenues available to different resource types, though it is still early in the process to predict how the project will affect various resource classes.

“It is vitally important that the ISO-NE markets accurately signal which resources effectively support reliability and how much capacity is needed,” Potomac wrote in its annual report. “This is necessary to avoid premature retirement of fuel-secure resources, incentivize generators to acquire inventory or firm fuel arrangements, and avoid overpaying for capacity that does not support reliability.”

The changes to accreditation will likely be both positive and negative for oil generators.

Accounting for fuel storage appears likely to increase the accreditation values for oil units relative to other resources, and multiple participants involved in NEPOOL discussions also said the shift to a seasonal market may push prices up in the winter, providing an additional boost.

However, oil-fired steam resources tend to have higher outage rates and greater maintenance requirements, which will likely limit their accreditation values, regardless of their stored fuel capabilities or potential winter benefits.

The shift to a prompt market would also allow resources to submit retirement notifications much closer to each CCP; it would reduce this notification deadline from about four years to about one. This would enable participants to make retirement decisions based on more up-to-date information about the conditions of the market and their resources.

“There’s so many variables and moving pieces to that design — it’s going to be hard to get a clear picture until we see more about how all those pieces fit together,” NEPGA’s Dolan said.

Some stakeholders also expect future capacity prices to reflect a perceived increase in PFP risk. Capacity scarcity events trigger the PFP rules, which penalize resources with capacity obligations that fail to perform and reward resources that deliver more than their obligations.

Some oil-fired generators have racked up significant penalties during PFP events in recent years. The resources generally require significant advance notice to ramp up and come online, making them ill-suited to perform during unexpected scarcity periods.

“I think it’s fair to assume that the higher Pay-for-Performance risk that people are now starting to perceive will work its way into the supply offers that will get submitted into the market,” Forshaw said, adding that this will likely put “some upward pressure on prices.”

New Mechanisms

Taking all factors into account, “the expectation is: Some of the older resources that do maintain significant inventories of residual oil are going to face challenges going into [the 2028/29] time frame and may consider submitting deactivation notices one year prior to the start of the delivery period,” Forshaw said.

With looming retirement risks and ISO-NE’s forecast that winter reliability risks will rise in the mid-2030s, it is important to begin discussions on potential solutions and new mechanisms, he said.

In a statement, ISO-NE noted it is evaluating “the potential addition of a longer response reserve product, such as a 60- or 90-minute reserve, to help manage uncertainties caused by the increasing variability of renewable generation and real-time system demand,” which may provide additional opportunities for oil resources.

The RTO also recently established a new Regional Energy Shortfall Threshold (REST), which is intended to define an acceptable amount of shortfall risk in the region. It plans to use the threshold to evaluate risks prior to each winter and summer season, as well as in long-term assessments. (See ISO-NE Proceeding with Shortfall Threshold After Positive Feedback.)

It has yet to determine how it would select and develop solutions to mitigate risk if the threshold is violated.

Data from long-term assessments “will guide evaluation of whether the possibility of exceeding the REST in those time frames requires development of regional solutions to mitigate modeled risks and, if so, when to begin to develop solutions; these efforts would be signaled in future annual work plans,” ISO-NE wrote in a statement.

The RTO has yet to deploy the threshold in long-term, forward-looking studies. ISO-NE’s probabilistic modeling for the upcoming winter indicates the region is well short of the risk threshold. (See ISO-NE Forecasts Minimal Shortfall Risk for Upcoming Winter.)

Forshaw emphasized the importance of establishing the process for addressing REST violations well before they occur, noting that major market reform frequently is a multiyear process.

If studies show high risks of energy shortfall because of a lack of fuel, it could make sense to procure fuel, or another type of energy, that would “only be used when we’re facing load shedding, rather than in the normal course of dispatch,” he said.

Interest in Dual Fuel

Regardless of potential new mechanisms or the specifics of the accreditation changes, some of the region’s aging oil generators may be nearing the end of their useful life. Resource owners that are willing to keep units online, waiting for a spike in capacity prices, may be unwilling to make large capital investments in the case of major mechanical failures.

This long-term outlook, coupled with the region’s winter gas constraints, has driven some increased interest in adding dual-fuel capabilities to existing gas plants, enabling them to burn oil during winter periods when gas prices spike or the units are unable to access gas.

“Given the slowdown on offshore wind and the other changes at the federal level that have really slowed down the scale and the pace of other clean energy entry, there’s been a lot of interest from state policymakers, ISO New England and others about exploring what capabilities exist out there for adding more dual fuel to make up this megawatt-hour gap that may be in front of us,” Dolan said.

Potomac wrote in its report that adding on-site fuel storage to gas-fired resources is “likely the lowest-cost strategy for addressing winter reliability concerns in the near-term in light of the issues with offshore wind development.”

However, there is uncertainty as to whether the states would allow the facility changes, or if the market would support the investments, Dolan said. He added that dual-fuel investments likely would require “over a decade of payback … and years of development to put it into place.”

He noted that the tensions and contradictions between state and federal policy have created significant development challenges for a broad range of resource types.

“It’s a really tricky environment, and I don’t have a clear answer of what to do about that,” Dolan said.

Clean Energy Solutions and Environmental Impacts

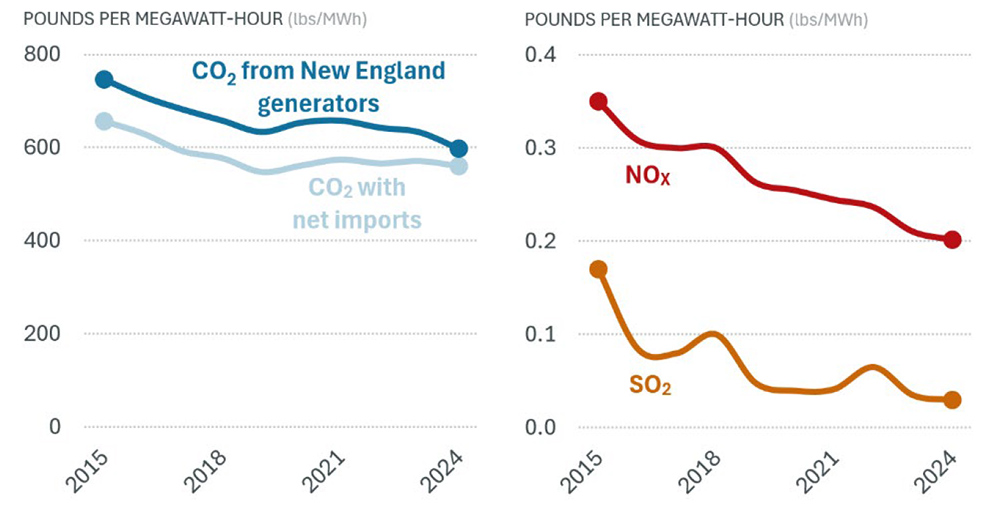

The decline in oil generation, and the replacement of inefficient oil and coal units with cleaner gas plants and renewable energy, has coincided with significant reductions in emissions from nitrogen oxides and sulfur dioxide, according to ISO-NE’s 2024 emissions report.

The RTO notes that between 2015 and 2024, sulfur dioxide emissions declined by 82% and emissions from nitrogen oxides dropped by 42%. This compares to a 15% decline in carbon dioxide emissions.

New England annual average emission rates, 2015 to 2024 | ISO-NE

Oil-firing power plants “are among the highest-polluting resources that we have,” said Joe LaRusso, manager of the clean grid program at the Acadia Center. “Many of them are located in communities that are overburdened with air pollution as it is.”

Nitrogen oxides and sulfur dioxide, along with fine particulate matter, are air pollutants associated with a range of heart and lung issues, child asthma, cancer, autoimmune diseases and neurological harm, according to the American Lung Association.

In Massachusetts, these pollutants were responsible for 2,780 excess deaths in 2019, according to Boston College researchers.

While it is difficult to attribute deaths to specific generation types or plants, the study notes that stationary sources, which include power plants, industrial facilities, and heating and cooking, were responsible for about 30% of fine particulate pollution in the state.

Concerns about health effects have motivated grassroots movements to block the development of new peaking plants. In Peabody, Mass., residents fought bitterly and, ultimately, unsuccessfully to stop the construction of a dual-fuel peaker, which came online in 2024.

Any efforts to add oil capacity in the region, or to implement market mechanisms propping up these units, would likely be met with opposition from environmental groups.

LaRusso said he is optimistic that three large projects nearing completion — Revolution Wind, Vineyard Wind and the New England Clean Energy Connect (NECEC) transmission line — will reduce the need for oil peakers, potentially pushing additional units into retirement.

NECEC is intended to supply the region with a consistent source of baseload power, while offshore wind performs best in the winter, when oil units run the most. Clean energy and consumer advocates also hope that aggressive demand-side initiatives will cause load to grow at a slower pace than is projected by ISO-NE.

In the long term, LaRusso said the resumption of offshore wind development in New England, the start of offshore wind development in Nova Scotia and increased bilateral power exchanges with Quebec could help the region meet growing winter demands while eliminating most of the remaining need for oil-fired generation.

“It seems that oil is going to follow the same path as coal, unless the demand curve starts rising so fast that batteries can’t keep up,” he said. “There are so many factors in play, but none of it appears to provide a rosy picture for an oil-firing plant.”

SEATTLE — The longstanding links among U.S. and Canadian electricity grid operators won’t be fractured easily by the tariff-driven political rift between Washington, D.C., and Ottawa, industry participants on both sides of the border say.

“The grid really recognizes no political boundaries,” NERC Vice President of Government Affairs Fritz Hirst said Nov. 10 at the Annual Meeting of the National Association of Regulatory Utility Commissioners in Seattle. He was speaking during a “Northern Exposure” panel discussion moderated by Nevada Public Utilities Commissioner Tammy Cordova.

“Like any other region anywhere on the grid, we have a natural complementarity north and south of the border where different regions depend on each other for energy transfers when needed,” Hirst said. “It’s probably one of the purest examples of the energy partnership we have between Canada and the U.S.”

Hirst noted that while Canada accounts for 10% of North American electricity load, it represents “a critical piece of the pie,” with 30 U.S. states trading power with their northern neighbor to the tune of 70 million TWh per year — enough to power about 6 million homes.

Maine Public Utilities Commission Chair Philip Bartlett pointed to a concrete example of that cross-border relationship: Residents in the northern part of his state receive all their power from either local resources or transmission coming out of neighboring Canadian province New Brunswick.

“For us, this is particularly important, and when we started hearing news of tariffs and concerns about the relationship between the United States and Canada, we got pretty nervous, because these customers are really wholly dependent on the very positive relationship that we’ve built over the years,” Bartlett said.

Bartlett pointed to the lines connecting New Brunswick with the larger ISO-NE system and noted that the New England Clean Energy Connect (NECEC), a 320-kV HVDC line capable of delivering 1,200 MW of Québec hydropower output to Massachusetts, is expected to be completed by the end of 2025.

New England’s relationship with Canada is expected to grow in importance, Bartlett said, in part because of the region’s lack of natural gas pipeline capacity to support new gas-fired plants and the Trump administration’s halting of offshore wind projects. (See Feds Pile on More Barriers to Wind and Solar.)

“Maine and the region had been really expecting to rely on offshore wind as a really important way for us to meet increased load, and also to deal with the expected retirement of some of our older oil plants,” he said. “So given that offshore wind is delayed in the United States, to the extent there are opportunities in Canada to move faster, that is something that could be a real reliability benefit to the region.”

Canada’s Internal Strains

“Yes, it’s hard to be a neighbor to the U.S. right now,” said Francois Emond, a commissioner with Régie de l’énergie du Quebec (part of the Canada Energy Regulator), referring to the tariffs Trump imposed on Canada earlier in 2025.

In laying out the top three challenges he thinks Canada faces now, Emond pointed first to the impact of the trade dispute with its southern neighbor.

“Canada’s economic health is highly susceptible to global political and trade shifts, a vulnerability that’s rooted in its heavy reliance on the U.S. market, with two-way trade accounting for about 65% of the GDP,” Emond said.

Tariffs and other global disruptions — such as supply chain issues — drive up costs for consumer goods and construction materials, including those needed for transmission lines and other energy infrastructure, he said.

The second challenge is the “regional and political divisions” that threaten national unity, with parties in Alberta — and Québec — reviving talk about separating from Canada.

“Tensions persist between regions like Alberta and Ottawa, and Quebec and Ottawa, fueled by disagreements over resource allocation, federal fiscal policy and differing approaches to the energy development and climate actions,” Emond said.

The third challenge has to do with the intersection of climate policy and energy affordability. Emond said that while Canada is committed by law to getting to net zero carbon emissions by 2050, the nation’s carbon tax “has become a lightning rod for political contention, with some provincial leaders calling for its removal, citing its impact on the cost of living and business competitiveness.”

“The priority for the country right now is to build resilience across its trade networks, critical infrastructure and the national unity to prevent increasing domestic and global volatility,” he said.

But even in light of that priority, Emond acknowledged the reality that, from an electricity standpoint, Canada’s provinces are more interconnected to their U.S. neighbors than to each other, a state of affairs he attributes to the country’s internal politics and lack of a national energy policy.

“If any provinces in Canada are saying we’re going to cut power to the U.S. because we don’t like what they’re doing, it’s not possible … the grid is integrated, you cannot do that, and we need also the power coming from the U.S.,” he said.

‘Giant Battery for the West’

Amy Sopinka, director of market policy for Powerex, the power marketing arm of Vancouver-based BC Hydro, said the British Columbia grid is connected to the neighboring province of Alberta and to the Bonneville Power Administration system in Washington, but that 90% of its power trading is with U.S. entities.

Sopinka pointed to the B.C. grid’s contribution to the broad geographical diversity of load and resources in the Western Interconnection: It’s a winter-peaking system compared with the summer-peaking systems in the U.S. Southwest, so its periods of highest demand complement much of the rest of the Western Interconnection. Also, BC Hydro controls about 19 GW of generating resources, including 16 GW of hydroelectric capacity, much of which are storage dams that “can act like a giant battery for the West,” Sopinka said.

“We’ve been both net importers and net exporters over the years,” she said.

Sopinka noted Powerex’s commitment to participating in Western Power Pool’s Western Resource Adequacy Program (WRAP) and SPP’s Markets+, the latter of which is to launch in 2027.

“The Western Resource Adequacy Program is a tool for formalizing the relationship of that resource diversity and demand diversity” for ensuring and accrediting RA, while Markets+ “will allow for the transactions” that support that diversity, Sopinka said.

‘Continental Interconnection’

Cordova asked panelists to share their hopes for the future of the U.S.-Canada electricity relationship.

Bartlett said he hopes for “more integrated analysis” of certain benefits and needs on both sides of the border, as well as “additional partnerships” and the identification of new transmission lines that serve both countries.

“I think the magic wand is we need the [U.S.] federal government to be more encouraging in this effort, because I think it really would benefit the United States in terms of the economic development, [and] the ability for us to build out the renewable resources and other resources that we need, but also do it in a way that is much more reliable and probably a much lower cost, if we can have effective interconnections,” Bartlett said.

But Bartlett also expressed concern that if the U.S. “were to go through two or three administrations like this one, that’s going to make it very difficult for Canadian governments.”

Emond said those in the electric sector might have to look beyond the current challenges to adopt “a more pragmatic way of thinking” that moves beyond politics to identify real needs and “keep discussing,” “making deals” and “do what’s needed for the consumers.”

“We need more generation in North America; that evidence is quite clear as we confront our economic needs [and] the AI race,” Hirst said. “So, I think I would just underscore the need to continue uplifting the North American relationship and truly think of us as a continental interconnection.”

“We have advantages, and it’s best if we can share them all, and then the system becomes more reliable,” Sopinka said.

The Independent Market Monitor has filed a complaint asking FERC to determine that PJM has the authority to hold off on large load interconnections if they would jeopardize transmission security or resource adequacy (EL26-30).

“The question is clear. If PJM has an obligation to provide reliable service to all PJM loads, is it just and reasonable for PJM to add new loads that it cannot serve reliably? The answer to that question is no,” the Monitor wrote in the Nov. 25 complaint.

It argues the proposals PJM and stakeholders made in the recent Critical Issue Fast Path (CIFP) process rest on the faulty assumption that the RTO does not have the ability to turn away large loads even when there is not sufficient capacity to serve them.

The Monitor’s proposal, which received the second-greatest amount of support out of a dozen, would establish a queue for large loads, preventing them from coming online until they could be served reliably. The queue could be bypassed by loads bringing their own generation, with an expedited study process for those resources. (See PJM Stakeholders Reject All CIFP Proposals on Large Loads.)

“The solutions offered by PJM and most stakeholders simply assume that PJM must agree to add large loads to the system when the loads cannot be served reliably because PJM does not have the required capacity resources. From another perspective, the position of PJM and market participants assumes that PJM does not have the authority to require that large new data center loads can be served reliably before those loads are added to the system,” the Monitor wrote.

The Monitor wrote that data center load is the primary driver of a reliability gap that is expected to grow over the coming years. It states that the 2026/27 Base Residual Auction (BRA) was short of the reliability requirement by 200 MW; those tight conditions also caused a $7.3 billion, or 82.1%, increase in auction revenues which would not have occurred without that load growth. (See PJM Capacity Prices Hit $329/MW-day Price Cap.)

PJM spokesperson Jeff Shields said the RTO is reviewing the complaint and does not have any comments before it submits a formal response.

“We have said that higher pricing is being driven by a supply and demand crunch, with the dominant driver on the demand end being data center electricity needs,” Shields added.

Monitor Joe Bowring told RTO Insider the complaint would clarify PJM’s authority to its Board of Managers before it decides on how to proceed with filing governing document changes in the wake of the CIFP.

The complaint makes the case that Order 2000 requires RTOs to maintain a reliable transmission network, which PJM has accomplished through its capacity market and Regional Transmission Expansion Plan (RTEP). If a large load cannot be served while maintaining the reserve margin, PJM should be able to deny interconnection until that can be accomplished.

“Interconnecting large new data center loads when adequate capacity is not available is not providing reliable service. The obligation to provide service is the obligation to provide reliable service. The obligation to provide service is not met if customers are simply interconnected without adequate resources to meet their demand,” the Monitor wrote.

The Monitor made similar comments on a transmission security agreement between Amazon and PECO, arguing that utilities should be required to demonstrate there is sufficient capacity and transmission capability before bringing large loads online. The commission’s Nov. 21 order determined such a demonstration is not needed for agreements between customers and utilities (ER25-3492). (See FERC Approves PECO-Amazon Transmission Agreement for Pa. Data Center.)

The West-Wide Governance Pathways Initiative could lead the charge on developing an alternative to the Western Resource Adequacy Program that would integrate with CAISO’s Extended Day-Ahead Market, according to Pam Sporborg, Pathways co-chair and director of transmission and markets at Portland General Electric.

PGE continues to engage with the Western Power Pool on WRAP’s development. But if the program cannot be aligned with both SPP’s Markets+ and EDAM, Pathways’ Regional Organization for Western Energy (ROWE) could step in as an alternative, Sporborg said in an interview with RTO Insider.

ROWE was created to assume governance of CAISO’s Western Energy Imbalance Market and the soon-to-be-launched EDAM. Some stakeholders have expressed an interest in building the program to offer additional voluntary market services. (See Pathways Initiative Exploring Funding Options, Issues RFP to Staff ROWE.)

An RA program could be one of those offerings if EDAM participants’ concerns about WRAP are not resolved, according to Sporborg.

“An alternative would be to have an RA program that was governed solely by the Pathways’ new regional organization that would be more integrated into the EDAM,” Sporborg said. She noted the alternative must “provide enhanced value for PGE and PGE’s customers and other Western utility customers.”

Her comments came after the Oct. 31 deadline for entities to commit to WRAP’s first financially “binding” season covering winter 2027/28. The final WRAP commitments showed the program has mostly been divided along the line of participants in CAISO’s EDAM and SPP’s Markets+.

Among the five utilities withdrawing from the WRAP, four — NV Energy, PacifiCorp, PGE and Public Service Company of New Mexico — have committed to joining the EDAM, while Eugene Water & Electric Board will be participating in Markets+ by virtue of its location within the Bonneville Power Administration’s balancing authority area.

Of the 16 committed to the first binding season, 11 are slated to join Markets+, two are leaning to EDAM and three are uncommitted to either day-ahead market. (See WRAP Wins Commitments from 16 Entities.)

The divide and the fact that WRAP is a program requirement for Markets+ has raised concerns about the program’s governance structure, Sporborg said.

Markets+ will gain a larger share of the voting power, “and we need to see and understand how that governance will evolve to ensure that we can be confident that the program will remain equitable for EDAM entities,” she said.

Another issue is that WRAP was conceived before day-ahead markets in the West, and the program was intended to work within a different footprint from the one emerging under Markets+ and EDAM, according to Sporborg.

WRAP is realigning its operations program to reflect the day-ahead market reality. This will “fundamentally change” what the planning reserve margin is and what the diversity savings are, Sporborg said.

“We don’t have enough information right now to make a financially binding decision based on that realignment,” she said.

PGE listed its concerns in an Oct. 29 letter to the Oregon Public Utility Commission. The utility pointed to efforts by the WRAP’s Planning Reserve Margin Task Force to evaluate new methodologies for setting planning reserve margins for program participants, as well as concerns about the technology underlying the program.

“Before we can commit to a financially binding program that has financial penalties for withdrawal; financial penalties for noncompliance; and the risks that that would put our customers on, we want to actually see how those design evolutions materialize,” Sporborg said.

Talk of an alternative RA program has been ongoing since at least Oct. 21, after NV Energy said during a hearing before the Public Utilities Commission of Nevada that it is discussing the option with other EDAM participants.

“It’s a consistent and expected result that the bigger your footprint, the more connected your footprint, the more savings that you can achieve through that diversity,” Sporborg said.

But the study also suggested there are savings to be made in a separate EDAM-aligned RA program, according to Sporborg.

“So, that gives us the confidence that we can continue to work with the [Western] Power Pool on the market alignment but also help us understand that if we can’t find a solution that is equitable to the EDAM, we could pursue this alternative and not be worse off than we would from that geographic WRAP perspective,” she added.

Pathways’ potential RA role was suggested by Spencer Gray, executive director of the Northwest & Intermountain Power Producers Coalition, during an Oregon PUC meeting Nov. 25 about the state’s RA program and WRAP. (See related story, Oregon PUC Votes to Waive RA Penalties for Independent Suppliers.)

Gray noted Pathways eventually could offer several “new solutions and services in the West.”

“There’s a good regional solution here that takes advantage of both load and resource diversity in multiple time zones and multiple latitudes,” Gray said about Pathways. “And that was the value proposition of WRAP. That’s the value proposition of both Markets+ and EDAM.”

When asked how WPP is working to address EDAM entities’ concerns about WRAP, organization Chief Strategy Officer Rebecca Sexton said, “With the commitments for 2027/2028, we are focused on binding operations and have a lot to do to get ready for that.

“The results of that work should improve the program and benefit our committed participants, as well as any participant who chooses to return,” Sexton told RTO Insider in an email.

The grid was never designed for the world it’s being asked to serve. Electrification is accelerating faster than planners expected; extreme heat is swelling peak demand; and climate-driven disasters are smashing records while breaking infrastructure.

Yet the electric industry is expected to build a grid that can deliver reliable power to regions that may succumb to, survive or even thrive in a future further affected by climate change.

Planning for the grid of the future requires increasingly sophisticated prognostication, and the industry needs to look to new data sources for modeling. Climate scientists and economists have become as important as engineers, and traditional peak-demand forecasts and resource-adequacy models cannot capture the compound stresses facing today’s grid.

Wayne Gretzky famously said he “skate[s] to where the puck is going to be, not where it has been.” That’s all very well if you know where it’s going to be — difficult for a puck, even more so for a grid being expanded in an environment some call a polycrisis.

Dej Knuckey

Utilities and regional planners no longer can rely on models built for a more stable, predictable climate, one that no longer exists. To build a grid that is both reliable and resilient, planners now need modeling tools that integrate growth patterns and climate risk. The next generation of modeling — probabilistic, scenario-based, climate-informed — is not simply an upgrade. It’s becoming the minimum requirement for any utility, regulator or investor hoping to keep pace with the world in which the grid must operate.

A new measure launched in November by the First Street Foundation may prove a critical tool for understanding the intersection of climate risk and economic growth.

Understanding Resilience Spread

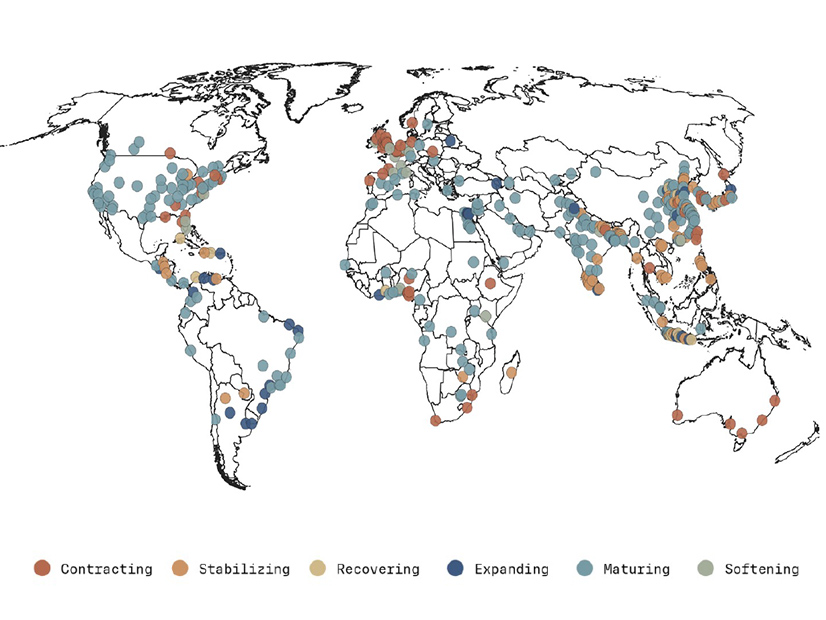

Resilience Spread, a concept coined by First Street, captures the intersection of two opposing forces, like Dr. Doolittle’s fictitious Pushmi-Pullyu, a double-headed llama that tries to move in two opposite directions at once. In one direction, there are positive market forces, reflected in population growth, economic strength and amenities such as housing and transportation. In the other direction, there are negative climate risks.

Resilience spread growth trajectories across global cities with 1 million or more residents | First Street

The Resilience Spread quantifies the gap between a region’s climate exposure and its ability to adapt. It’s a gap that is widening in many areas, creating a patchwork of vulnerability. Looking at 400+ of the world’s major cities, First Street determined that economic strength is outweighing climate risk by a massive $1.8 trillion globally, which “illustrates that, on average, strong macroeconomic conditions and consumer confidence continue to offset the drag of climate hazards,” the report said.

But the average is meaningless for planners. What’s important is how individual cities are expected to perform, and that ranges widely. And there’s also the factor of time. While today’s global spread is net positive, “this cushion is not permanent. Without significant adaptation, the spread is projected to erode steadily, tipping negative before the end of the century as climate pressures intensify faster than foundational macroeconomic conditions.”

The speed at which we lose the economic buffer depends on how we invest in adaptation. The firm predicts that unless those investments are substantial, the global spread will be eroded fully by 2085, “as intensifying hazards outpace resilience.”

The Many Faces of Climate Risk

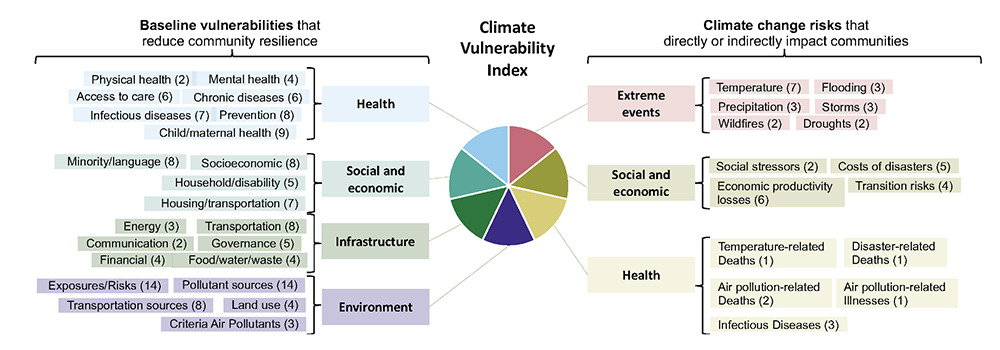

Climate risk comes in many flavors. The U.S. Climate Vulnerability Index map, developed by the Environmental Defense Fund and Texas A&M University, drills down on the various climate risks and impacts in each county or census tract. It maps extreme events, such as storms and droughts (see our series on the effects of extreme climate events on the grid: fire, flood and heat), as well as impacts such as heat-related deaths and other factors such as air pollution and socioeconomic stressors.

Climate vulnerability is a function of both community resilience and climate change risks. | U.S. Climate Vulnerability Index

The index accounts for an essential piece of the resilience equation: If an area already is struggling, it is less likely to withstand the challenges posed by climate change.

First Street distinguishes between chronic and acute risks: “Chronic risks reflect long-term, gradually intensifying physical climate stressors such as heat, drought or sea level rise, while acute risks capture short-term, high-intensity events like floods, storms or wildfires.”

For grid planners, chronic risks are easier to plan for, and the grid can be hardened to resist them in advance, but acute risks are more likely to damage significant portions of the grid, providing the opportunity to rebuild in a more resilient way.

Growth in All the Wrong Places

Why, in a world where we’ve known for a few decades that climate change will adversely affect major economic centers on the coasts, are some of the biggest economic centers also the most at risk of climate damage? Because many of the biggest cities were located at trading hubs, which historically were at deep ports. First Street found what it called a “striking paradox.” Of more than 400 major global cities, “over half of global urban GDP is concentrated in places facing the highest levels of acute climate risk.”

A city’s attractiveness as a place to live and do business can survive high climate risk, according to First Street. “Many of the world’s most economically productive cities remain hubs of growth despite sitting in the top quartile of acute risk.”

Miami is an example of a city that is both one of the world’s most productive, high-growth cities and among the most exposed to climate events, such as sea-level rise, heatwaves and hurricanes. Despite being in the top percentile of climate risk, its economic strength is buoyed by amenities ranging from a strong labor market to the desirability of living near wide sand beaches.

In cities like Miami, where the market effect outweighs the climate effect, First Street’s resilience spread is positive.

“These positive spreads imply that markets potentially undervalue their opportunities relative to climate risk, highlighting a hidden upside, as capital inflows remain strong and long-term attractiveness endures.” For planners, that resilience spread can be used as a factor to adjust growth models upwards.

They also caution that the spread today is looking forward from one point in time. “Resilience is not fixed. Cities that thrive today may falter tomorrow if climate risks intensify … and begin to outpace the economic foundations that support their growth.”

When the Resilience Spread is Negative

On the other end of the spectrum, a negative resilience spread occurs when the negative climate effect exceeds the positive market effect. “Climate risks’ impact on location desirability already outweighs local economic strengths in roughly 30% of global cities today,” First Street found.

New Orleans is an example where its role as a strategic port and its cultural significance fail to counterbalance the impact of its exposure to acute climate risks, most notably hurricanes and the resulting flooding.

Repeated extreme storms, including Hurricanes Katrina in 2005 and Ida in 2021, “have driven steady population decline, unaffordable insurance rates and insurer withdrawal, resulting in a deep negative resilience spread of -10.3%,” First Street said.

New Orleans is an example of a U.S. city where the market effect is lagging the climate effect, leading to a negative resilience spread. | Dej Knuckey using data from First Street

For cities such as New Orleans, grid planners face a difficult calculation: how much to invest in the grid’s resilience where climate threats are substantial and population is declining.

There is a risk that a deep understanding of climate risk modeling will lead to inequity. When there are so many competing capital investment demands, it can be tempting to deprioritize regions with weak adaptive capacity where any investments face greater risks from climate damage or economic decline. Yet those areas may depend most on investments today to withstand future challenges. Until there are discussions about managed retreat from the most climate-vulnerable areas — a topic few political leaders are willing to touch — policies must support the vulnerable communities as well as the well-resourced areas.

System Strength and the AI Demand Growth Wild Card

The market effect and climate effect are just two of the plethora of factors that planners need to consider. Infrastructure fragility — the ability of each part of the grid to withstand acute and chronic climate risks — is another key variable that will be the topic of a future column. And population trends also are key in a time of increased climate migration.

Perhaps the largest factor outside of climate change that is complicating grid planning is the rise of data centers, especially AI data centers, which weren’t foreseen only a decade ago. It has moved forecasts that had been flat to negative into positive territory. S&P Global Commodity Insights anticipates U.S. electricity consumption “to grow at a compound annual growth rate of more than 3% from 2025 to 2030, with generation in tow.”

That demand is not spread evenly throughout the country but is lumpy with intense localized demand in the areas where they are being built. Northern Virginia is the poster child for unexpected load growth, with 70% of global internet traffic carried by the more than 200 data centers in the county, according to Oxford American. As RTO Insider columnist Peter Kelly-Detwiler pointed out recently: “These facilities are large (often well over 100 MW), disconnected from the general macroeconomic environment and extraordinarily difficult to forecast.”

Investing in Foresight

With so many competing factors shaping the grid of the future, utilities, ISOs and regional planning entities will need to invest in data infrastructure and modeling capabilities, building internal capabilities and accessing external expertise as needed. A key part of this will be ensuring acute and chronic climate risks are understood and accounted for, both in cities and rural areas, and in high-risk and high-growth areas.

The competing forces of market strength and climate vulnerability vary within any territory served by each utility, grid operator or policy body, and there’s no single approach to planning that serves communities at opposite ends of the resilience scale. But all areas will be served better by industry and policy leaders who insist on, and invest in, advanced modeling.

Without smart, sophisticated modeling, planners will be flying blind—and costs, blackouts or inequities will be the price.

Power Play columnist Dej Knuckey is a climate and energy writer with decades of industry experience.

El Paso Electric again is seeking regulatory approval for its New Mexico renewable energy plan after resolving tariff-related cost uncertainty of a solar-plus-storage procurement proposed in the plan.

The New Mexico Public Regulation Commission rejected the plan in October based on concerns about the cost of energy from the proposed 150-MW Santa Teresa solar project. EPE reported in August that developer DE Shaw Renewable Investments (DESRI) had told it the project had been “materially and adversely impacted by recent changes in law, in particular related to the imposition of tariffs by President Trump.”

The tariffs were expected to “result in millions of dollars worth of unplanned cost increases for construction of the generating facility,” the developer said. In an Oct. 16 order, the PRC said it could not approve EPE’s plan because the cost of the Dona Ana County-based project was unknown.

But since then, EPE has worked out a deal with DESRI calling for the utility to pay the same rate for energy from the project as in their previous agreement but with the contract terms extended to 25 years rather than 20.

The plan the commission is being asked to approve covers the first 20 years of the agreement; EPE would bear the risk of the five-year extension, PRC staff said in a filing.

The expected cost of the project’s energy assigned to New Mexico for 2026 is $45.67/MWh. That is below an inflation-adjusted renewable cost threshold of $74.14/MWh.

The PRC on Nov. 25 granted EPE’s motion for a rehearing, which could take place as soon as Dec. 11.

EPE and DESRI did not respond to RTO Insider’s request for more details on the tariff impacts.

RPS Challenges

New Mexico’s investor-owned utilities file a plan each year on how they will meet the state’s renewable portfolio standard in the following year.

The required percentage of zero-carbon resources supplied for retail electricity sales increased to 40% in 2025, after sitting at 20% since 2020. It will continue to rise through 2045, when it reaches 100%.

In 2023, EPE supplied about 16% of retail energy sales to New Mexico customers with renewable resources, a figure that grew to just over 20% in 2024.

EPE’s 2026 plan includes renewables and renewable energy certificates from an approved portfolio as well as the proposed Santa Teresa procurement.

Santa Teresa will be built at the former site of the Hecate solar project, which at one time was expected to be in service by 2022 but never was built. DESRI took ownership of the project. EPE’s power purchase agreement for Hecate was terminated in 2024, and the utility received $14.9 million in liquidated damages, according to the 2026 plan.

EPE, which serves customers in New Mexico and Texas, noted in its plan the challenges of providing electricity in jurisdictions with different renewable energy requirements. The utility previously received PRC permission to adjust the amount of renewable energy allocated to New Mexico, rather than Texas, to meet New Mexico’s RPS targets.

For the Santa Teresa project, EPE asked to buy all the solar energy generated in 2026 and allocate it to New Mexico, starting when the project comes online midyear. That allocation would be needed to meet the 40% RPS target in 2026, but it likely would be a short-term arrangement.

“EPE would not expect to propose allocation of the total annual energy output of the [Santa Teresa project] in 2027,” the company says in its proposed plan.

Of the project’s 150 MW of battery storage, EPE wants to purchase and include 50 MW in its RPS portfolio.

The California Department of Water Resources and other parties have asked CAISO to restart a transmission access charge initiative that was put on hold in 2018 due to the development of the ISO’s Extended Day-Ahead Market.

CDWR, along with the Bay Area Municipal Transmission Group and the State Water Contractors, want CAISO to bring back a drafted final proposal regarding the ISO’s Transmission Access Charge (TAC) rules in order to possibly reduce the amount of new transmission needed in the state.

CAISO’s current TAC rules measure transmission use with a “volumetric-only” approach, which “fails to reflect cost causation and utilization of the transmission system, resulting in inequitable allocation of costs,” the CDWR group said in Nov. 13 comments on CAISO’s draft 2026-2028 policy initiatives road map.

“Costs should reflect that transmission networks are built to handle peak demand when the grid is strained the most,” the group said.

CAISO instead should recover a larger portion of fixed electric transmission costs through a demand-based rate structure, and less from volumetric rates, the group said. Doing so would incentivize better load management practices and reduce the need for new transmission that is driven by peak demand requirements, they said.

Current TAC rules send inefficient price signals to behind-the-meter battery storage resources operators, the group said. If price signals were accounted for more specifically, CAISO might find it needs to plan for less new transmission infrastructure, the group said.

In February, CDWR proposed to restart the TAC initiative and bring back the 2018 proposal. However, CAISO dismissed CDWR’s request because the “levels of behind-the-meter solar have stabilized, rendering these changes unnecessary and overly complex in today’s market,” CAISO said, according to the CDWR group’s Nov. 13 comments.

CDWR is concerned about CAISO’s “misunderstanding of the substance and need” for the TAC proposal and are “frustrated by the process used to date,” they said.

“CAISO infrastructure staff have dismissed the need for this initiative, without any stakeholder meetings to discuss the issues that motivated the initiative in 2016-2018, or to consider input from stakeholders on the current need for the TAC structure changes that were fully vetted and proposed to be adopted in 2018,” the group said.

The 2018 TAC initiative was supported by CAISO’s Department of Market Monitoring, California’s three largest investor-owned utilities, municipal utilities, independent transmission developers, retail marketers and the California Public Utilities Commission, the group said. The proposal supports CAISO’s resource adequacy capacity program for required contributions to coincident peak demand and DMM’s support for allocation of natural gas transmission infrastructure costs, they said.

The current TAC rules started in 2001, and the structure has remained “relatively stable” through the intervening years, CAISO staff said in the 2018 draft final proposal.

CDWR’s comments were filed in CAISO’s annual policy initiatives road map process, which determines the policy initiatives for the following three years. CAISO plans to release a final policy road map in December for the 2026-2028 cycle.

NV Energy Requests Policy Review Changes

NV Energy filed comments about CAISO’s policy road map, asking CAISO to evaluate the frequency, length and content that is reviewed in stakeholder policy meeting sessions.

The ISO’s policy meeting sessions have become longer but have been held less frequently. This approach to policy development with stakeholders has caused certain meeting materials to be condensed or skipped altogether, NV Energy representative Lindsey Schlekeway said in comments to CAISO. The long gaps between meeting sessions have made it difficult to track and follow issues raised by stakeholders, Schlekeway said.

“It would be helpful for CAISO to be mindful of the resource constraints considering the activities that are underway in the West,” Schlekeway said. “The stakeholder process may have large impacts to the market design, and NV Energy would like to dedicate sufficient time to each initiative in order to provide the most informed and helpful comments to CAISO.”

NV Energy recommended CAISO hold three-day meeting sessions, rather than one meeting per month, to review complex issues with stakeholders.

New Jersey should continue to pursue a strategy of heavy reliance on clean energy to head off the state’s looming energy shortage, with no increase in natural gas generation, says a new plan released by outgoing Gov. Phil Murphy (D).

The governor’s 2024 Energy Master Plan pays little heed to critics who say the state’s pending energy shortfall requires renewed consideration of new natural gas plants. Instead, it outlines a future that is heavily dependent on clean energy, along with building electrification and enhanced use of electric vehicles.

The plan says the “pillars of planning and decarbonization” should provide the state with stability in the face of a future in which the PJM region — which includes New Jersey — faces annual demand increases “for the first time in two decades.” That includes a forecast of 32 GW in additional peak demand in the PJM region by 2030 and a 58 GW increase by 2035.

“Any future aligned with the state’s economic, energy, and climate goals will require accelerated clean energy generation — solar, wind, advanced nuclear, green hydrogen and battery storage,” according to the plan. “Doing so will reduce electricity imports, boost in-state generation, grow clean energy jobs, increase resource diversity and support long-term cost stability.”

The clean energy recommitment by Murphy, who leaves office in January 2026, comes amid heated debate about how to speedily increase the state’s affordable energy generating structure to meet accelerating demand from artificial intelligence companies and data centers. Some politicians argue that the potential electricity crisis is so severe that the state should adjust its carbon emission commitments and consider expanding its natural gas generating fleet.

Former Gov. Chris Christie (R) said at an Oct. 28 energy conference organized by the New Jersey Business & Industry Association that the winner of the November gubernatorial election should look to “open two or three new natural gas generation plants as quickly as possible” (See N.J. Forum Explores Solutions to Looming Energy Shortfall.)

U.S. Rep. Mikie Sherrill (D), the eventual winner, said during a debate in October that she would “improve our gas generation in the state.” In a Nov. 20 television interview, she said: “We need to make sure our gas generation, which is about 40% of our production right now, is more, is modernized, so we can drive down carbon emissions while driving up much of the generation from gas generation.”

The New Jersey League of Conservation Voters released a statement calling the plan “an affordable energy road map at exactly the right moment.”

No Plans for Gas Plant Construction

Murphy, releasing the plan, called it the “culmination” of his two-term effort to tackle “the challenges of energy affordability, supply and demand, and climate change.”

Murphy’s staff, in a briefing on the plan, said it considers gas generation to be important as a “dispatchable resource” but contains no prescription to build more gas generators in the state.

Annual energy balance by scenario | New Jersey Energy Master Plan

The state “is projected to rely on investments in solar, battery storage and offshore wind to support growing demand” and meet its goal of zero emissions by 2035, the plan says. “Total gas generation declines by 2050 across all [the plan’s proposed] mitigation scenarios … driven by the expansion of renewable and nuclear capacity.”

The plan adds that the strategy will reduce the amount of imported electricity as battery storage, nuclear, wind and solar — utility-scale and distributed — expand to meet the new demand.

Changing Energy Landscape

What effect the master plan will have is unclear given that the transition from Murphy to Sherrill will take place in January. A Murphy staffer said the plan offers a “compendium” of what the state has done under his tenure, and it is up to Sherrill whether to incorporate the suggestions into her own strategy.

Sherrill’s transition team did not respond to a request for comment.

Murphy has come under criticism that his focus on developing a robust wind sector — he set an offshore wind goal of 11 GW — left the state short on new generating sources when the bet on wind failed. The state has no active wind project after developer Ørsted abandoned its two Ocean Wind projects in 2023 due to logistical issues and rising costs. A third, Atlantic Shores, withdrew amid the Trump administration’s opposition to offshore wind. (See Developer Shelves Atlantic Shores, Seeks to Cancel ORECs.)

A release from Murphy’s office said the master plan offers a “flexible, adaptive framework of ‘no-regrets’ strategies and policies” that can adapt to the “changing energy landscape.” Murphy’s staff said the concept means the state can pursue them, and any investment, without wholly committing the state to the strategy if the environment changes and a direction shift becomes necessary.

The strategy includes “doubling down on the state’s successful solar programming, while at the same time expanding programming to deploy battery storage projects, clean firm generation options, virtual power plants, as well as exploring the potential for advanced nuclear resources in the state,” the plan says.

Reliable and Modern Grid

The master plan was compiled by Energy + Environmental Economics (E3) through research, modeling and stakeholder input. A draft plan outlined three different scenarios that varied in how aggressive their pursuit of the state’s emissions reductions goals would be, and compared them with the scenario if the state did nothing. That comparison evaluated the effect on electricity rates.

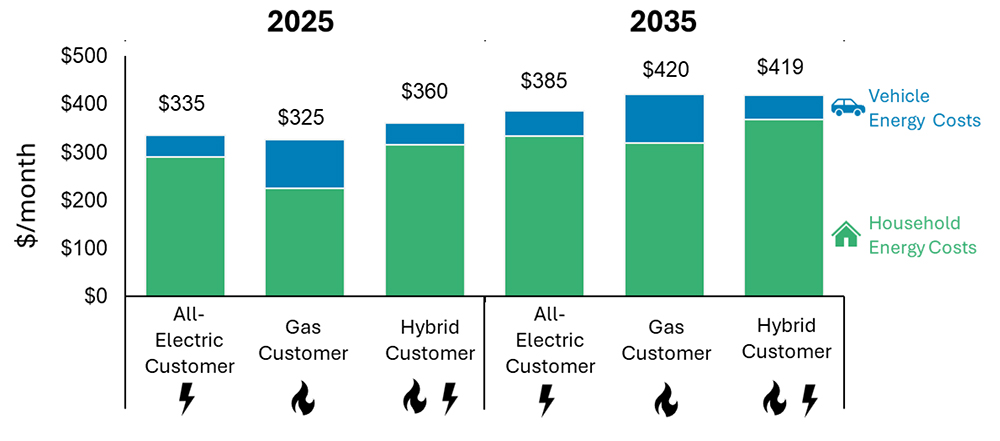

The plan predicts that electricity use will increase by between 66 and 109% by 2050, depending on which scenario is pursued. It reports that customers wholly using electric appliances and vehicles will see a $50 increase in their monthly energy costs from 2025 to 2035. Customers using mainly gas would see a $95 increase, while those using a hybrid of both would see a $59 increase.

Average monthly energy bills projected by the plan | New Jersey Energy Master Plan

The completed plan does not recommend which of the three scenarios the state should adopt but instead makes a series of recommendations for strategies and policies.

They include “accelerating clean energy deployment” and “expanding decarbonization and efficiency programs.”

“Not only does more efficient equipment provide lower bills for program participants, it reduces overall electric demand, thereby taking pressure off the wholesale power market and reducing emissions from both the power and buildings sectors,” the plan states.

The plan calls for moves to ensure a “reliable and modern grid,” and for the state to continue pursuing transportation electrification. Although the state, with 260,000 EVs on the road, is nearly 80% of the way to reaching its target of 330,000 EVs, the plan does not suggest a new one.

The plan also calls for the state to enhance “regional coordination and advocacy.”

“New Jersey must continue to actively engage with PJM and neighboring states to ensure grid reliability, affordability and accelerate clean energy integration,” the plan says. “Additionally, the state should continue to take steps to have more formal involvement in the PJM decision-making process to ensure that its policy objectives are reflected in PJM’s market rules and policies.”

Higher prices under Ontario’s renewed market are causing heartburn for mines and greenhouse growers, stakeholders told IESO on Nov. 26.

During the ISO’s quarterly market briefing, IESO officials said the market is performing well, with “intuitive price formation,” and that no new “high-priority defects” have been discovered since their last briefing in August. (See Ontario Nodal Market Nearing ‘Steady State’ After Nearly 4 Months.)

“We’ve now got about six months of operating in the renewed market behind us and … I think everybody’s learning and building their understanding of the new market dynamics that we’re seeing as we shift through each season,” said Candice Trickey, IESO’s director of market readiness and customer experience. “Overall, [based on] everything I hear from you and that I see internally, we are all making, collectively, really good progress in working in this new system.”

However, several stakeholders said they are facing challenges from higher prices since the new market launched May 1.

Alain Cote of Vale Canada — whose five mines and other operations use about 200 MW per hour — said Ontario Zonal Prices in November have risen from about $50/MWh to about $80/MWh in November.

“I’m just having a hard time … forecasting that,” he said. “It’s a big swing.”

Consultant Stephanie Freund, who advises commercial greenhouse companies in southwest Ontario, said her clients have seen increasing price spikes since October, when they turn on their grow lights to nurture winter crops.

“They are really struggling … trying to keep up with the day-ahead [market] in order to manage their lighting schedules … to avoid the spikes,” Freund said. “They’ve never seen such high electricity prices as now. … They won’t be able to afford running” the lights. She asked if IESO had tools to help them manage the volatility.

Darren Matsugu, IESO’s director of markets, said Ontario is seeing higher prices because it is the peak of the fall maintenance outage season. “We are definitely in the period where we have the most resources on outage to make sure that we have that availability before the winter,” he said. He suggested Freund talk to the ISO’s customer relations team about ways to manage the high prices.

Cal Brooks, of FirstLight Power, said that — even accounting for inputs like gas prices and system load — prices appear to be higher than under the Hourly Ontario Energy Price (HOEP), which the ISO used before the Market Renewal Program introduced nodal pricing and a financially binding day-ahead market.

“Do you see that as … something good in that maybe real supply and demand signals are now being reflected in a way they weren’t under the old market?” Brooks asked.

Matsugu noted that the HOEP uniform clearing prices did not include congestion and losses, which now are reflected in LMPs.

“The structural changes that we put in place are to better align the price signals we’re sending with the underlying system conditions,” he said. “Those system conditions are continuing to change. We are getting into tighter and tighter conditions than we have before, and so certainly we would expect that … the underlying prices [would] be higher.”

The ISO says the new market will produce net cost savings for consumers by reducing out-of-market payments and improving the efficiency of scheduling resources.

“I think we are seeing the benefits, particularly when we talk about our intraday unit commitment and our day-ahead commitment,” Matsugu said.

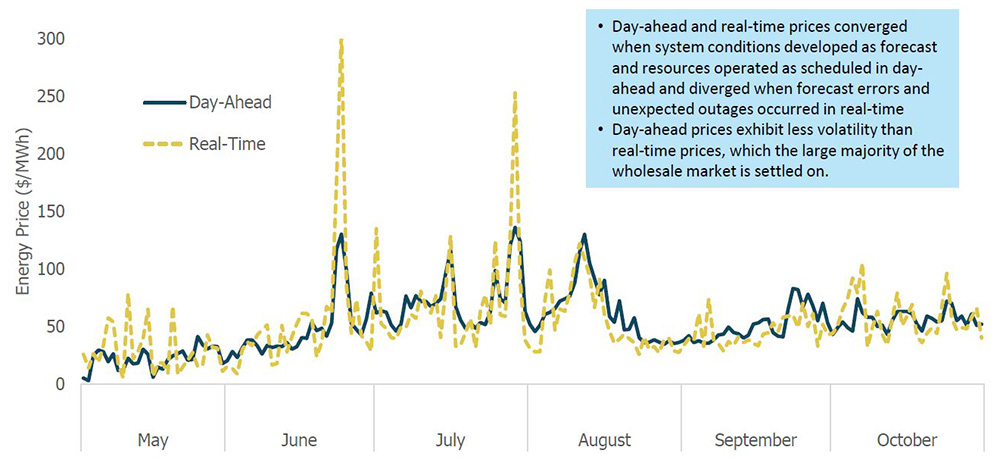

IESO officials said market prices have reflected system conditions, with real-time and day-ahead prices converging when actual conditions match forecasts and varying with deviations in real time.

Jennifer Jayapalan, of Workbench Energy, said her company has seen big changes in how some resources are being used. “We’ve seen a lot more demand response activations, not just in peak conditions, but also into the fall and as recently as the last week or two,” she said. “And we’re seeing a lot more operating reserve [OR] activations across this period as compared to really all years prior to MRP. And neither of these two actions are really publicly reported anywhere by IESO, and both are quite expensive.”

Matsugu said scheduled generation outages contributed to the DR and OR activations and that the ISO will consider whether it can provide more transparency on such actions. “We don’t have, necessarily, all the same resources available that we had during our peak of the summer, but we do that outage planning to correlate with the expected levels of demand.”

Defect Caused Demand Fluctuations

Trickey said the ISO investigated whether a defect that was causing demand fluctuations had an impact on hourly DR activations and concluded it did not create any inappropriate activations.

The defect caused the Ontario demand values published in IESO’s Realtime Totals Report to change by hundreds of megawatts for only a few five-minute intervals.

Because of the unpredictable nature of variables such as supply disruptions, sudden increases in heating or cooling demand, and neighboring system conditions, there often are changes in demand from one interval to the next. But “swings of several hundred megawatts for only a few intervals have historically been quite rare,” the ISO said in a presentation.

The summer brought higher demand, higher prices and greater price separation between day-ahead and real-time markets. | IESO

IESO said it identified a calculation that overstated demand when hourly DR resources are on standby. The ISO has implemented a manual workaround to counter the defect pending a permanent fix.

Without the workaround, the defect could result in incorrect prices for impacted intervals and incorrect peak demand hours for the Industrial Conservation Initiative if they occur on a potential peak day. ICI participants pay their share of Global Adjustment charges based on their peak demand factor, which is calculated based on their contribution to the top five peak hours over a year.

IESO identified 38 intervals with incorrect prices and corrected them with administrative prices. It confirmed that the top 10 peaks posted on the Peak Tracker webpage were not affected.

Settlements, Defects

IESO officials said they have improved settlement processing times, and that statements and invoices issued in October and November were delivered ahead of the ISO’s 5 p.m. goal.

Trickey said the new market is producing much more data “and that was taking longer to process than ideal. So we’ve been working on improvements.”

Of the settlement disagreements that have been resolved, the ISO said about 30% have been attributed to defects that have been corrected, with the remaining 70% of disputed statements confirmed as correct.

IESO continues to work through a backlog of disagreements, some of which are related to pending defect fixes. The ISO is notifying participants if there are delays in correcting settlements because of the pending fixes.

IESO officials said they had discovered several minor defects since August, including scenarios in which non-quick-start resources operating in combined cycle mode are receiving after-the-fact settlement mitigation calculated using the single cycle mode reference level.

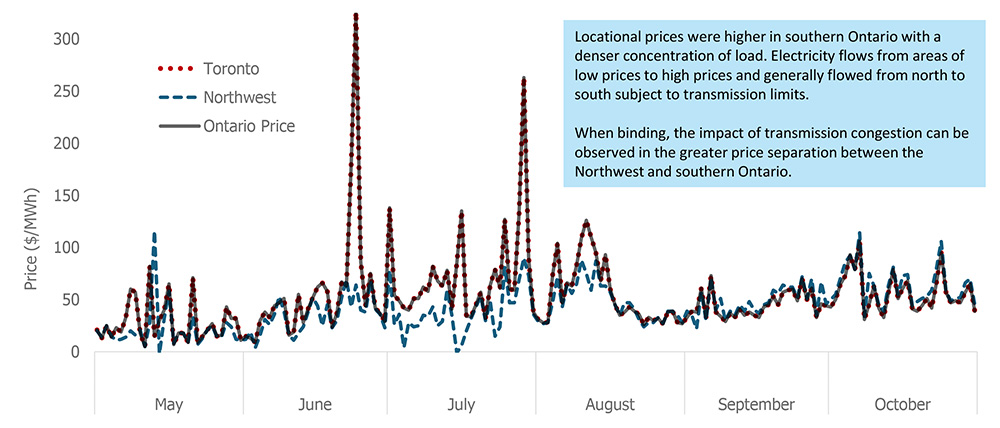

LMPs are similar throughout Ontario when there is little congestion. When demand — and congestion — is higher, as in summer, prices separate between the Northwest and the rest of Ontario. | IESO

The ISO also disclosed economic operating point (EOP) errors that may result in adjustments to real-time make-whole payments (MWPs) in resettlement statements posted on Nov. 17 and Dec. 12. EOPs reflect the output a resource could have achieved based on its physical capabilities and LMP, under actual market conditions.

The impact of the resettlements will be small, “because they’re all fairly specific scenarios impacting just certain types of resources,” Trickey said.

Trickey said IESO will continue its quarterly briefings on the Renewed Market’s performance for the first year of operation.

In response to requests from market participants, the ISO is creating a new group, the Renewed Market Advisory Forum, to discuss ways to improve the market.

Trickey said the group will focus on incremental improvements, not “long-term, evolutionary” changes.

“We’ve implemented this new market. Is everything working the way we thought it would, or as effectively as we hoped?” Trickey explained. “And if we’re seeing some gaps — whether it’s information that people need, or some parts of the system that aren’t working as well as we hoped — this is where we would like to have those kind of conversations with participants that are really engaged in the market.”

Candidates interested in participating should submit expressions of interest by Dec. 19 to engagement@ieso.ca.

{kind=link}