The Massachusetts Department of Energy Resources (DOER) and the state’s investor-owned electric utilities have issued a request for proposals to procure up to 1,500 MW of mid-duration energy storage, a key step toward the state’s goal of contracting 5,000 MW of energy storage by mid-2030. The procurement marks the largest energy storage solicitation issued to date in New England.

The state also outlined its expected timeline for future storage solicitations, noting that it plans to issue additional 1,000-MW mid-duration storage procurements by July 31, 2026, and July 31, 2027, and wrote that “all remaining energy storage systems capacity shall be procured by July 31, 2030.”

The Massachusetts Legislature in 2024 passed a law requiring electric distribution companies to enter long-term contracts for 5,000 MW of energy storage by mid-2030, including 3,500 MW of mid-duration storage (between four and 10 hours), 750 MW of long-duration storage (between 10 and 24 hours) and 750 MW of multi-day storage (greater than 24 hours).

The RFP is intended to procure projects “that have a strong likelihood of being financed and constructed and that will provide a reliable and cost-effective source of beneficial, reliable energy storage systems to the Commonwealth,” the DOER and the utilities wrote.

In the first solicitation, the state seeks only to procure the environmental attributes associated with storage projects. This includes credits for the state’s Clean Peak Standard, which incentivizes emissions reductions during peak demand periods.

The bid submission deadline is noon on Sept. 10, 2025. Bidders are allowed to propose projects at or above 69 kV that can supply between 40 and 1,000 MW and can propose long-term contracts running through the end of 2050.

The RFP requires projects to have a scheduled in-service date earlier than Jan. 1, 2030, and directs each bidder to “demonstrate that its proposal can be developed, permitted, financed and constructed within a commercially reasonable timeframe.”

Projects must commit to achieving capacity interconnection rights and qualifying for the ISO-NE capacity market. The RFP requires bidders to “include a realistic and specific plan to implement any transmission system upgrades or other work anticipated to be needed to achieve CCIS-equivalent interconnection.”

Developers also must provide a nonrefundable bid fee of $500/MW of proposed nameplate capacity, which is intended to cover the cost of evaluation.

Projects will be evaluated based on quantitative and qualitative criteria. They will be graded on a 100-point scale, with 80 points for direct and indirect costs to ratepayers and 20 points for qualitative factors, including project viability, climate and environmental benefits, grid reliability and resilience effects, and stakeholder engagement.

The DOER, working with an independent evaluator, will select winning bids. The utilities will be responsible for executing contracts, which will be subject to the approval of the Massachusetts Department of Public Utilities (DPU).

The DPU approved the procurement framework in late July, writing that it “represents a reasonable balancing of interests and demonstrates progress toward achieving the Commonwealth’s statutory energy storage systems requirement as well as seeking to contract for low-cost energy storage systems.”

Under the current solicitation timeline, winning bids are to be selected by Dec. 9, and long-term contracts are set to be executed by March 27, 2026.

The D.C. Circuit Court of Appeals has remanded to FERC an order rejecting a mitigation plan LG&E and KU Energy filed to replace its longstanding obligation to de-pancake rates for wholesale customers (23-1196).

The court ruled Aug. 8 that FERC did not adequately consider whether the utility’s transition mechanism provided ratepayers protection from the removal of the rate schedule the utility instituted in 2006 when it left MISO. Schedule 402 ensured customers would not pay duplicate rates across its territory after Louisville Gas & Electric and Kentucky Utilities merged in 1998 while also reimbursing them for MISO’s charges because the grid operator did not agree to reciprocally de-pancake its own rates.

After more than a decade of using Schedule 402, the company asked FERC to end its obligation, which the commission did in 2019, on the condition the utility institute a transition mechanism. But the commission reversed itself on remand from the D.C. Circuit in 2023 and directed the utility to reinstitute 402. (See FERC Upholds De-pancaking Provisions in LG&E/KU Rates.)

In its decision, FERC declined to use the pre-merger status quo — which would have rates pancaked between MISO, LG&E and KU — as a point of reference. The utility argued that FERC should have used that as a baseline and that its retail customers were picking up the costs of de-pancaking rates with MISO for wholesale customers. The utility also proposed a transition mechanism that would have continued de-pancaking some rates for wholesale customers for decades, which it argued would fully mitigate any impact on wholesale rates.

“We are not satisfied that the commission adequately addressed this important issue: that the transition mechanism agreements would have protected each customer with a reliance interest, thereby mitigating any concern that customers continue to need Schedule 402 to protect their reliance interests,” the court said. “In fact, during oral argument, counsel for FERC suggested that the transition mechanism agreements could be a potential protection offered to mitigate or end the need for de-pancaking.”

Eighteen municipal customers benefit from the de-pancaking, and 12 of them would be covered by the transition mechanism or some other agreement. The other six do not take service from MISO.

FERC needs to consider whether the transition mechanism is enough to get rid of Schedule 402, the court ruled.

“We do not make that determination for the commission but simply remand the case back to the commission so that it can weigh the evidence and determine whether the transition mechanism agreements would adequately protect ratepayers,” the court said.

New Jersey faces tough decisions on how to balance the risk of blackouts against the cost of reducing their frequency, speakers said at a resource adequacy forum organized by the state Board of Public Utilities.

Any plan to combat the expected surge in demand from data centers, they said, likely will be fraught with uncertainty because the emerging situation is unprecedented.

Possible strategies mentioned at the Aug. 5 forum include asking data centers to curb their use at high-demand moments, enhancing energy efficiency strategies, going outside of PJM for power and better coordinating distributed energy resources and storage.

In each case, a proper allocation of costs and a benefit-cost analysis will be critical, speakers said at the forum, conducted at The College of New Jersey in Ewing, N.J. The challenge is multiplied by the sheer size of the problem.

“The loads are very difficult to plan for, and they appear very, very quickly,” said Tim Gallagher, CEO of ReliabilityFirst. “These things bring very unique and significant challenges to both the planning and the operation of the bulk power system.”

Higher Prices Needed

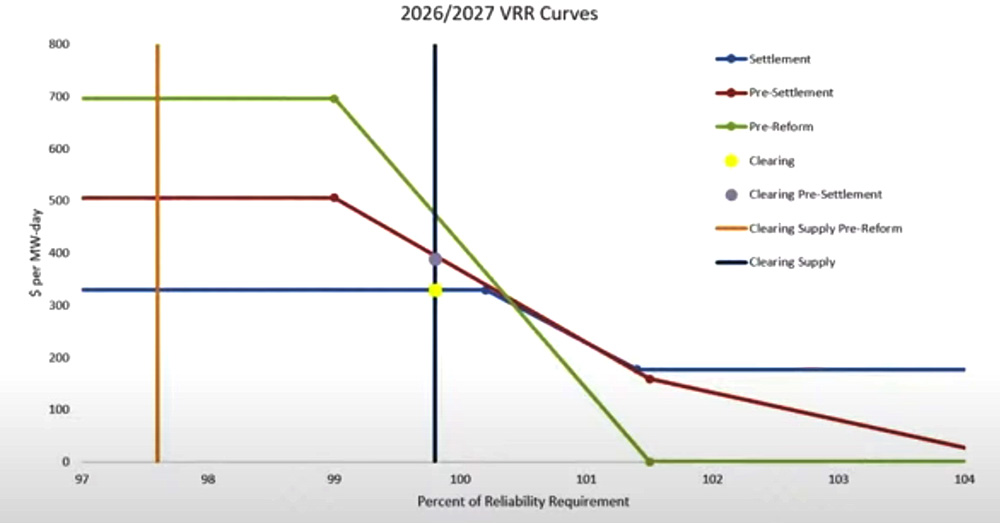

The conference came two weeks after PJM revealed that prices at its July capacity auction soared to $329.17/MW-day (UCAP) RTO-wide for delivery year 2026/27. Prices in the 2024 auction jumped to $269.92/MW-day, the result of load growth, generation deactivations and changes to risk modeling that shrank reserve margins. (See PJM Capacity Prices Hit $329/MW-day Price Cap.)

While New Jersey officials have voiced outrage at the auction prices, and a 20% hike in the average electricity bill, the prices still don’t stimulate new generation development, warned Richard Levitan, president of Levitan and Associates, an energy management consulting firm.

“We have to be realistic about clearing prices continuing to ascend in order to get price signals to developers for new build,” he said. “We could be looking at price signals that are much, much higher, closer to $700 per MW-day.”

Acceptable Power Loss Level

Paul Youchak, of the BPU’s office of federal and regional policy, said PJM sets its reliability levels at the commonly held standard of “1-in-10,” meaning only one event every 10 years in which the RTO could not meet demand for at least 24 hours.

States that want to lower that risk can invest more in new generation, pushing up costs, he said. He questioned whether “reliability and affordability today … are diverging in a way that hasn’t diverged before?”

PJM demand curve | NJ BPU

Gallagher explained that at present, “ratepayers emphasize costs more than reliability,” in large part because “we’ve enjoyed 99.9% reliability for most of our lives.” If the state continues on the current path as demand rises, “reliability starts to suffer,” he said.

That may trigger calls for a new standard, he said, adding that NERC is moving toward a new standard of “energy adequacy, which is actually studying every hour of the year to make sure you have enough electricity for every one of those hours.”

Unified Load Forecast

Whatever standard is in place, the state faces a difficult challenge predicting future load.

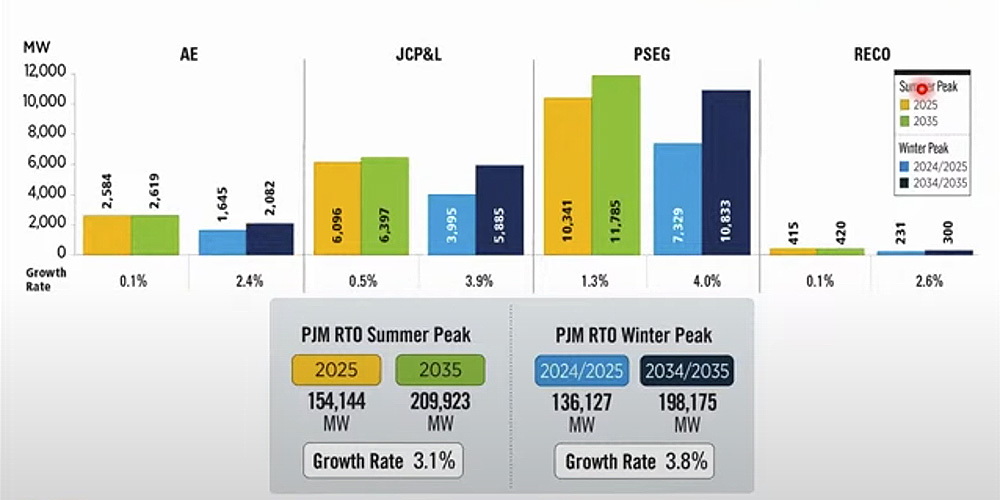

Youchak emphasized how suddenly the demand picture has changed. In 2023, he said, PJM predicted that by 2038 the region would have load of about 165,000 MW. By 2025, the RTO predicted the 2038 load would be around 220,000 MW, an increase of more than one-third.

“It is an order of magnitude difference from the type of volatility we’ve seen in the past,” Youchak said.

New Jersey, with 100 data centers at present, ranks only 15th in the nation, Gallagher said. And they typically aren’t the kind of heavy-load artificial intelligence facilities that present the biggest challenges, he said. Instead, New Jersey data centers work to “support government services, public health systems, emergency and disaster response” and other functions, he said.

But because New Jersey is an energy importer, it will be impacted by the arrival of big data centers elsewhere in the RTO region, and “must plan for this rise in demand,” said Margarita Patria, a principal of Charles River Associates.

“What’s needed is a clear understanding of data center load trajectory going forward,” she said. “We need a unified approach in assessing data central load and move to perhaps probability-based forecasting tools that more accurately reflect the state of affairs and will enable more informed decision making.”

Yet the unique element of hyperscalers, the largest data centers, makes that difficult, said Tom Rutigliano, senior climate advocate for Natural Resources Defense Council.

Traditional statistical methods of basing predictions on past performance have difficulty accounting for the dramatic influx of data sector loads that have no precedent, he and other speakers said. And forecasts may include data center projects that may never come to fruition, speakers said.

Andrew Gledhill, senior analyst for resource adequacy planning at PJM, said the organization is working on “implementation guidelines, talking about the key criteria” that should be included in forecasts, such as “the uncertainty of data center development when you start looking at five to 10 years.”

One way to address that is to produce “accuracy metrics on these projections,” including after-the-fact scrutiny of data center forecasts to determine “what came to fruition, how did the numbers match up with what they were expecting at the time?” Gledhill said.

The shifting demand profile of the region has added to the importance of getting the forecasts correct. Part of the challenge is that the highest peaks are now in the winter. A loss of power can plunge residents into darkness and cold and create much more severe consequences than in the past, when summer peaks dominated and the main impact was loss of air conditioning.

New Jersey load forecasts | NJ BPU

“If we don’t have electricity for a sufficient period of time today, people actually die,” Gallagher said, citing the dozens of deaths that occurred during power loss triggered by the severe winter storm in December 2022.

In addition, peaks triggered by data centers are more sustained, and so more challenging to handle than the relatively brief demand surges resulting from a cold spell or a heat wave, Gledhill said. Of the 32 GW of demand increase expected in the PJM region by 2030, 30 GW will come from data centers, he said.

“That’s generally flat load,” he said. “So the load profile, as we move into time, is getting flatter and flatter, which means that there’s going to be more hours of risk that pop up.”

Managing Demand

Sam Newell, principal with the Brattle Group, said the state should “foster energy efficiency demand response programs,” essentially asking users at a “mass market level” to reduce their load at peak times. The state, for example, can set up virtual power plants to manage a network of distributed energy resources, such as solar panels, batteries and electric vehicles, to handle load at peak moments.

Speakers also suggested that big energy users be asked to cut energy use when the overall load gets heavy. But big data centers are reluctant to take that step, in part because “it’s difficult for them to predict when an AI-related data center is going to go into learning mode, and that’s when their electric demand ramps up significantly,” he said.

In addition, Newell said, “a lot of the data centers are not hyperscalers. But they might have 400 to 600 tenants in the data center, and it’s difficult for them to pick exactly which ones of those tenants” should take part in demand-response load cuts, he said.

One audience member asked if New Jersey should continue the current level of subsidies for solar when the availability factor — the percentage of its full name plate capacity that it can generate electricity — for solar is only about 11%, due to the limited time in which panels generate electricity. In contrast, PJM rates a nuclear generator at 93%, offshore wind at 69% and a gas combustion turbine at 60%.

Rutigliano said the benefit of solar is it’s cheap and clean. But he acknowledged that “it doesn’t give you a lot of reliability value.”

“I’ll confess, NRDC’s modeling says that the most cost-effective way to a low-carbon grid is a fossil fleet that’s around the same size as what we have now; it just doesn’t run very often,” he said. “Since the reliability or research adequacy issue is the clear and present one, subsidies now in PJM should be flowing to storage, to wind. Offshore wind actually brings more value than a combustion turbine.”

In a surprise move, President Donald Trump will tap Democratic Commissioner David Rosner to become FERC chair, multiple news outlets have reported.

Axios first reported the development Aug. 8, citing an unnamed White House official as the source, with the story also being picked up by Bloomberg.

Rosner, a FERC staffer who had been detailed as an aide to the Senate Energy and Natural Resources Committee under the leadership of former Sen. Joe Manchin (I-W.V.), was appointed to the commission in 2024 by President Joe Biden to fill the seat left by former Chair Richard Glick — whose renomination was quashed by Manchin.

The Senate approved Rosner’s appointment on a vote of 67-27, with most opposition coming from Republicans. He also lost backing from Sens. Ed Markey (D-Mass.), Bernie Sanders (I-Vt.) and Elizabeth Warren (D-Mass.) and was opposed by environmental group Friends of the Earth. (See Rosner, See Clear Senate to Fill out FERC.)

“David Rosner was a paid cheerleader for the LNG boom before it was fashionable,” Lukas Ross, climate and energy deputy director at Friends of the Earth, said at the time of Rosner’s nomination. “Letting Joe Manchin control FERC from beyond his political grave should be a nonstarter for every other Democrat in the caucus.”

In addition to supporting fossil fuels, the Trump administration also favors co-location of data center loads with nuclear power plants.

“David Rosner has committed to executing President Trump’s America First energy policy agenda,” Axios quoted the White House official as saying.

The official also told the publication that Rosner has been “instrumental” in working to “accelerate the building of power data centers to win the AI race” and that the choice “emphasized the president’s desire to work with action-oriented people who will deliver positive results for Americans.”

In June, President Trump nominated Laura Swett of Vinson & Elkins to replace Christie, a development Christie said he learned about through a media inquiry about his replacement. (See Trump Replacing FERC Chair Christie with Laura Swett.)

While commissioners appointed by Democrats currently control FERC 2-1, Senate confirmation of nominees Swett and David LaCerte would put Republican appointees in the majority, possibly putting the chairmanship back in play. (See LaCerte Nominated to Complete Phillips’ Term at FERC.)

Meantime, power industry stakeholders and watchers are sure to speculate about the motives behind Rosner’s appointment.

Posting on X late Aug. 8, former FERC Chair Neil Chatterjee wrote:

“Theory — the WH is doubling down on data center co-location and is looking to seat a @ferc majority that will support a framework moving forward. Christie was an outstanding Chair. See has been a conservative commissioner… but they both voted against Talen-AWS. My best guess.”

Chatterjee was referring to the commission’s rejection last November of a proposed amendment to Talen Energy’s interconnection service agreement with PJM and utility PPL that would have allowed Amazon Web Services to expand its co-located load at its Susquehanna nuclear plant in Pennsylvania. (See FERC Rejects Expansion of Co-located Data Center at Susquehanna Nuclear Plant.)

FERC Chair Mark Christie officially stepped down at the close of business Aug. 8, leaving the commission with a quorum of three until the Senate considers two pending nominees from President Donald Trump.

He posted his last letter outlining FERC’s work over the previous week, which he started writing after Elon Musk emailed all federal employees asking them to send emails doing the same in February.

On Aug. 7, Christie posted on Musk’s social media site X that he had filed his last dissent as a FERC commissioner, in which he sided against the majority who partially granted a complaint Savion filed against PJM (EL25-63).

In the order, the majority sided with Savion, which argued it should have gotten an extension on an interconnection construction service agreement (ICSA) for a 66-MW solar development it was building at the same site, with the same point of interconnection, as an existing 111-MW solar plant it previously built. The project was built on a former surface coal mine in Martin County, Ky.

Savion argued PJM violated its rights under the ICSA, saying the RTO should have let it suspend work on the second part of the Martin project for 18 months after a construction firm building withdrew from the project unexpectedly and tariffs on solar panels were changed in 2024.

PJM said it was not eligible for suspension of the ICSA because the transmission infrastructure had been fully constructed.

FERC sided with Savion, finding that PJM improperly denied the suspension and saying that the 18-month suspension should be effective on Dec. 14, 2024, when Savion first requested it. Some work is left to be done on the interconnection facilities, which means the suspension still can go into effect, the majority reasoned.

Christie dissented, saying the order would let interconnection capacity go unused and further disrupt and delay PJM’s queue. AEP had finished building the transmission, and 111 MW of the Martin solar facility already was connected to the grid.

“The ICSA permits a project developer to suspend work ‘associated with the construction and installation’ of the transmission owner interconnection facilities,” Christie said. “Here, the record demonstrates that ‘construction and installation’ is complete.”

AEP has a couple of tasks to do, but the project is injecting power over the interconnection point. So just because some adjustments might be made, that does not mean there is remaining work that can be “suspended,” he said.

“The majority’s expansive reading of Section 3.4 would allow a customer to ‘suspend’ work through and including the time at which the project is operational and injecting power to the system and any time in the future,” Christie said. “This reading is illogical. It is plainly at odds with the purpose of suspension, which is to stop work on interconnection facilities when the generating facility is delayed (not when the generating facility is operational).”

Christie said PJM “hits the nail on the head” in its argument that the complaint is seeking to delay completion of the project and in the process “hoard the interconnection capacity” in a way that is unfair to other projects that use the capacity.

“The resulting delays and uncertainty hinder development of new generation and stifles competition, which harms PJM at a time when it desperately needs that new generation; instead, today’s order benefits a single developer to the ultimate detriment of consumers,” Christie said.

KANSAS CITY — SPP state regulators have approved a policy that establishes criteria for developing joint transmission projects with other RTOs to cost-effectively address persistent market-to-market (M2M) congestion.

SPP intends to use the targeted market efficiency projects (TMEPs) to resolve M2M congestion that has resulted in millions of dollars of charges on its seam with MISO. SPP’s neighbor already uses TMEPs on its PJM seam.

The cost of each project would be allocated between SPP and MISO based on the ratio of historical congestion costs, adjusted for M2M settlement effects. The interregional cost allocation would be recovered through the regionwide annual transmission review requirements.

Louisiana and Texas voted against the policy over cost-allocation concerns during the SPP Regional State Committee’s Aug. 4 meeting. Attorney Dana Shelton, proxy for Louisiana Public Service Commissioner Mike Francis, expressed concern about “the allocation on a regionwide basis in the absence of showing a regionwide benefit.”

Minnesota Public Utilities Commissioner John Tuma questioned the reluctance to talk about market efficiencies, saying TMEPs will benefit only SPP’s ratepayers.

“This concept is about creating market-to-market benefits for our ratepayers. I think exploring it is only in our best interest at this stage,” he said. “Minnesota has joined this organization because we are one of those seams organizations, and we do see the benefit of these [M2M] efforts. Is this a big one? No … but it’s the kind of thing that will help us out in the long run.”

The TMEPs would apply only to M2M flowgates along the MISO seam with a minimum of at least $1 million in historical congestion costs. Staff are proposing a $20 million project cap with an in-service time frame of three years and a four-year payback of avoided congestion costs.

SPP’s Clint Savoy told the RSC that RTO staff is trying to filter the list of constraints they want to fix as part of the biennial joint system study with MISO. He said staff will use historical market data to find operating days when constraints bound in the day-ahead market. They will calculate the production cost for the entire market, remove the constraint and rerun the production cost analysis.

“The change in production cost is essentially the benefit that SPP receives, so it’s a reduction in the production cost for the market as a whole,” Savoy said.

The committee agreed with staff’s recommendation to stop moving a tariff change (RR681) that allocates costs of seams projects outside the FERC Order 1000 interregional process. Instead, it remanded the issue back to the Cost Allocation Working Group to address stakeholder concerns and asked it to provide an update during the RSC’s November meeting.

The Markets and Operations Policy Committee rejected the proposal during its July meeting with only 54.9% approval. Members were uncomfortable about whether the projects would be subject to the grid operator’s competitive process screening. (See “Seams Cost Allocation Rejected,” SPP MOPC Briefs: July 15-16, 2025.)

The RSC also granted CAWG’s request to delay the annual stakeholder review of the Safe Harbor Limit, which sets designated resources’ eligibility for base-plan funding at costs less than or equal to $180,000/MW. The working group said the delay was necessary because of “significant changes in SPP processes.”

Bylaw Change for Western RTO

The RSC approved an amendment to its bylaws that will allow western commissioners to join the committee upon the RTO’s expansion into the West in 2026. The expansion will make the Arizona, Colorado and Utah commissions eligible to add representatives to the committee.

Commissioners will be able to vote on proposed policy or tariff changes and other matters only if the proposal applies to the interconnection where their state is located. As Nebraska, New Mexico and South Dakota straddle both interconnections, those states will be limited to one vote if the proposal applies to both regions.

The Western commissioners will be eligible to join the RSC after April 1, 2026, when the RTO expansion goes live. Staff said vendors are successfully building and testing market systems, with member testing to begin in September.

Three Western commissioners sat in on the meetings: Arizona’s Kevin Thompson, New Mexico’s Greg Nibert and Wyoming’s Mike Robinson. Missouri’s Glen Kolkmeyer also was a guest although his chair, Kayla Hahn, represents the state on the RSC.

The committee also endorsed a three-person Nominating Committee consisting of RSC President Patrick O’Connell, South Dakota’s Kristie Fiegen and Tuma that will recommend the 2026 leadership during the November meeting. It also approved a 2026 budget that passes $1 million for the first time ($1.18 million) by including an extra $500,000 for consulting services and making allowances for increased membership.

Employee No. 3 Speaks out

Bruce Rew, who recently announced his pending retirement from SPP as senior vice president of operations, was greeted with a round of applause before one of his last updates during the Joint Stakeholder Briefing following the RSC meeting. (See SPP’s Rew to Retire After 35 Years in Operations.)

“Bruce reminds us he was Employee No. 3. I’m not sure 1 and 2 are still alive, but Bruce has had a remarkable career at SPP,” board Vice Chair Ray Hepper said, teasing the 35-year veteran. “So this may be among your last opportunities to really chew on Bruce in a board meeting.”

Rew said SPP has issued only one resource advisory thus far in 2025, which lasted two days in April, compared with five in 2024. During that period, demand peaked for the year at 56.6 GW, about 1,500 MW below the all-time high. Despite the demand but with negative LMPs, staff were able to export almost 5 GW of energy to MISO and PJM June 25-26 when the RTOs’ solar power vanished during the evening hours.

“As we gain more and more solar, that’s something that we’re going to continue to manage operationally to make sure that we’re prepared for that as well,” Rew said. “We potentially could have that same experience if we get 5 or 10,000 MW of solar.”

It will be a while yet. The grid operator recently added its first gigawatt of solar capacity, complementing its 35.6 GW of wind capacity. It has added more than 3 GW of capacity in the past year, pushing its registered capacity past 100 GW.

SPP has published a report on the April 26 load shed event near Shreveport, La., one of three in the footprint this year. The report analyzes the event, identifies the main causes, examines SPP’s response and provides recommendations and improvements to prevent similar incidents in the future. (See SPP Addresses 3rd Load Shed Since March 31.)

SPP Lays out Market Principles

Carrie Simpson, SPP vice president of markets, followed Rew to the podium and discussed the priorities for market design changes set in a staff white paper that is circulating: price discovery and transparency, economic efficiency, reliability effectiveness and system performance.

Referencing the 5 GW of exports to MISO and SPP, Simpson called it the result of a “healthy seam.”

“It’s a good indication … that our pricing was supporting the rest of the interconnection, because people were able to buy from us and sell into MISO and PJM,” she said. “Had these exports not occurred, our LMPs would have been significantly even lower because we would have had to back down even more generation. And so just a good indication of the market working well and the signals being available to participants to take action and move power where it was needed or more efficiently needed in the interconnection.”

WASHINGTON — The growing number of data centers offers a major growth opportunity for demand response, as it can help get the energy-hungry facilities online quicker than new generation, executives and data center experts said at CPower Energy’s GridFuture 2025 conference Aug. 6.

On top of that, renewables are growing, and their intermittency needs to be balanced, CPower CEO Michael Smith said at the event, held at the Omni Shoreham Hotel.

“We’ve dispatched more than we ever have this year,” he said. “So, all of these things are conspiring to create a further need for flexible load on the system.”

It takes a couple of years to build utility-scale solar and 15 years to build nuclear, he said. That does not factor how hard it is to get through the interconnection queues, or the relatively low forward prices in the markets compared to new-build costs that could rise further with the imposition of tariffs.

Policymakers are starting to pay attention to that fact, with Senate Bill 6 in Texas requiring new loads at 75 MW or above to provide DR, ENP Consultants Director Jim McDonald said.

“You’re going to see … a new version of Senate Bill 6” everywhere, McDonald said. “When AEP came out with their data center-only tariff a year and a half ago, that was a novel idea.”

Many utilities now have adopted similar rules to AEP’s, which require more upfront deposits to secure a place on the grid. The same week as the conference, Google announced deals with AEP’s Indiana Michigan Power and the Tennessee Valley Authority to reduce power at its data centers when the grid is stressed in their territories. (See related story, Google Strikes Demand Response Deals with I&M, TVA.)

Training artificial intelligence models has been driving demand growth from the sector, and while that is energy intensive, once those models are trained, they are going to be put to work, which will use more power, said Morgan Scott, vice president of global partnerships and outreach for the Electric Power Research Institute.

“As we become more mature in the way that we use AI, it will continue to use more energy,” Scott said. “Will we find efficiencies? Yes. Are these numbers wrong? Yes. But the point is, they are directionally correct and give you conceptually an understanding that this is going to continue to grow because of the way that we are going to use AI and what we are asking these models to do.”

The hardware side also is changing quickly, with the lifespans of the equipment in data centers getting shorter and shorter. Microchips degrade in one to three years now and innovations are rolling quickly, she added.

“We’re seeing massive jumps in terms of what that electricity draw is, and so you can see we actually have a forecast of 1.2 MW per rack in a data center because of those changes within Nvidia chips,” Scott said.

The business opportunity for CPower and the DR industry in general is huge when it comes to the growing demand from AI, Smith said in an interview after the event.

“Those activities can stress the grid because they can come on fast and they can consume a lot of electricity very quickly,” Smith said. “So, that’s exactly what we do. We’re that shock absorber that monetizes or optimizes the value of the flexibility that’s inherent in those machines.”

CPower and other DR companies are able to provide them a channel to monetize the flexibility that is possible in their operations, Smith said.

Data centers can offer flexible load either by curtailing their operations, including by shifting them to other sites, or using on-site resources such as backup generators or, as Duke explored in its study, batteries.

“We give the market operator access to those assets, and the market operator then can dispatch effectively those assets when needed,” Smith said. “And it really is a dispatch protocol. … A market operator can and should be able to dispatch a 500-MW peaking plant or a 500-MW data center equally.”

AI Opportunities and Risks

CPower is looking into AI to help improve its operations. Smith said his sales team uses it to take notes in meetings, but eventually it should help with the software the company uses to manage aggregations of DR customers.

“It will help that software make better decisions about where to put various customer assets, in what programs [and] at what times,” Smith said. “We do develop our own software. We have to be pretty cognizant of the tools that are available to us and use them appropriately. I’m not super comfortable just turning AI loose for the sake of turning AI loose, but I think our IT organization has done a really nice job of allowing AI to be used in the organization.”

While the demand growth from AI and other sources presents opportunities for the entire power industry, it is not without its risks, CPower Chief Legal and Regulatory Officer Ken Schisler said in a separate interview.

“If we’re not careful, what could be voluntary DR participation becomes power rationing, and that’s going to be rejected by the public,” Schisler said.

Conscripting demand flexibility like in Texas Senate Bill 6 could prove politically unsustainable as well, he said.

“People are going to want to see the transmission built or the power stations built so that they can use power when and where they want it, and if they have flexibility, they want to be able to make it available to the grid on their terms, rather than have it conscripted and rationed for them,” Schisler said. “So … unless you have those flexibility opportunities widely available, you’re left with no choice but to sort of simply ration power.”

Rising prices have led to political pushback, with states in PJM looking for reforms to cushion their consumers. Schisler said he is familiar with that dynamic from his time on the Maryland Public Service Commission. When the state restructured, it placed temporary caps on the price of electricity. Some utilities’ caps expired in 2004 — just before natural gas prices spiked in response to two historic hurricanes, leading to much higher bills for customers.

“It happened right before Katrina and Rita” in 2005, Schisler said. “You wouldn’t want to be me back in those times, and we’re in one of those phases now.”

States have been updating their policies and working to get reforms through at PJM in response to the situation, but one area Schisler said could help is improving access to data from customers to help enroll even residential customers into DR to save them money.

Data access varies by state. Schisler said ERCOT’s market, wholly within Texas, is one of the best examples of making it easy and New York is working on reforms to do the same thing. But in multistate RTOs like PJM, it has proven much more difficult.

“I can go anywhere in the world, and I have a safe, secure banking system that I can get money out of an ATM, check my balance, etc., and know that that system is secure,” Schisler said. “But we’re still at a place where, at scale, interacting with utilities to get data is still a patchwork.”

One way some companies have gotten around this is to install their own meters so they can help customers manage their loads, but that is economically wasteful, Schisler argued. The issue for data access has been around for years; President Barack Obama tried to address it with the Green Button Initiative, which Schisler called “an anti-standard.”

“We’re still acquiring data through lots of different channels now; Green Button didn’t make that go away,” he added. “The other challenge with it is it’s largely an issue that is under the domain of state commissioners, yet the [reason] for accessing this data is for participation in wholesale markets, and we haven’t bridged that need with state regulators and with utilities.”

Utility managers should not be afraid to explore the benefits that recent advances in artificial intelligence can bring to their frontline employees, a tech company leader told attendees of ReliabilityFirst’s annual Human Performance Workshop.

RF holds the Human Performance Workshop each year to share insights into factors affecting employee performance and suggestions for improving efficiency.

In his introductory presentation, Johnny Gest, RF’s manager of engineering and system performance, noted a phenomenon — what he called “performance drift” — that can develop in complicated organizations. Poor communication from managers, personal health and stress, organizational changes and overly harsh policies can all make it difficult for employees to understand their responsibilities within the system.

Barry Nelson, CEO of FactorLab, a developer of AI systems aimed at workplace improvement, picked up this theme in his own presentation, emphasizing the need for clear communication of expectations in the business world.

“The question is, what can we do to drive consistency [and] predictability with such a complex and dynamic environment?” Nelson said. “And in this particular case, can AI play a role — and not a role like writing an email, but a real role to help you, as leaders, maybe frame the problem or look at the problem in different ways to reduce drift?”

Nelson said AI can give managers a fresh look at their own systems, identify areas of improvement and set targets and benchmarks for success. For instance, an electric utility based in the southeastern U.S. used an AI product developed by FactorLab to improve communication in its safety meetings, leading to a double-digit reduction in the severity and frequency of serious injuries over two years.

Managers can use AI tools to examine their organizations’ communication from various angles, Nelson said. One product can score conversations on a range of factors, such as engagement of participants, level of detail on various topics and the quality of questions. With this information, organizations can work to improve the efficiency of their communication.

He also discussed the role AI can play in improving workplace communications by assisting with the editing of presentations and documents. Nelson gave the example of a daily briefing for frontline workers, in which managers have to keep the attention of employees who may feel bored or preoccupied with preparing for the day, and may zone out without catching important information.

“Technology can play a role in helping us find these pockets [of friction] and then understanding the system and cultural problems in order to fix the pockets,” Nelson said. He mentioned that AI can also help address language barriers, showing a video of a Spanish-language briefing translated into English in real time.

Nelson emphasized that the proper use of AI is not to replace human engagement but to improve efficiency within an organization so employees do not feel overlooked or undervalued.

“We find that the feedback has been incredibly positive from those in the field, because they know someone’s listening. They get the sense that … we care about these conversations, and that we’re trying to help them get better,” Nelson said. “Obviously, that’s not everyone’s cup of tea, but you would be surprised how many people in your organization are really looking for some feedback that we simply don’t have the human capacity to give at the moment.”

The Bonneville Power Administration’s proposed changes to its grid access process have prompted questions about how new readiness criteria will affect established industry practices and financing of new projects.

In February, BPA paused certain transmission planning processes to consider changes in light of significant growth of transmission service requests. The federal power agency’s 2025 transmission cluster study includes more than 65 GW of requests, compared with 5.9 GW in 2021. The requests exceed the total regional load predicted for the Pacific Northwest in 2034, according to the agency. (See BPA Halts Some Tx Planning Processes Amid Service Requests and Industry Sees Challenges as BPA Considers ‘Radical’ Updates to Tx Planning.)

On July 9, BPA outlined its proposed plan to tackle the queue during a workshop. The agency has developed a two-part approach: a transitional phase to get off the pause and a longer-term “future state” that will include more substantial reforms to BPA’s existing transmission processes. (See BPA Outlines Proposed Transmission Planning Reforms.)

“In general, our current model will not work to effectively evaluate and respond to the massive amount of requests and megawatts in the BPA transmission service queue,” BPA spokesperson Doug Johnson told RTO Insider. “The framework of our proposal revolves around instituting more rigorous requirements for transmission service requests. The goal is to process the queue as quickly as we can to advance our efforts to identify, plan and build the projects our customers need to do business as well as to provide interim service to those parties who have clarity about the service they need now.”

As part of this effort, BPA has proposed implementing readiness criteria to weed out speculative requests from commercially ready projects.

“The current practice in the Northwest is for load-serving entities to require developers who are bidding into their request for proposals to provide their own transmission,” Henry Tilghman, a consultant whose clients include Renewable Northwest and the Northwest & Intermountain Power Producers Coalition, told RTO Insider. (Tilghman spoke on his own behalf, not that of his clients.)

The load looking to purchase the output of a project doesn’t provide the transmission — the project provides it, Tilghman explained.

“So that puts the burden on the developer to get into the queue and obtain transmission service,” he noted.

Financing at Risk?

However, under BPA’s new proposal, the agency would require evidence of security or a power purchase agreement or bilateral transaction between a load and resource to establish commercial readiness, Tilghman said.

“You would not be allowed to even request transmission service until you have an agreement in place or provide security,” Tilghman said. “So that completely disrupts the existing model where the bidder into the [request for proposal] has to have transmission service placed in order to be eligible to bid.”

This could affect financing of new projects, Tilghman contended. He said lenders have conducted risk assessments based on criteria that have been in place for decades.

“One of those criteria is having transmission service in place with enough certainty that the project will be able to deliver … its output to its customer,” he added. “Now you’re going to have to do development without that … transmission as you bring your project through the development process.”

The Pacific Northwest Renewable Interconnection & Transmission Customer Advocates (PRITCA), a coalition whose members constitute more than 25% of the current BPA interconnection queue, has expressed similar concerns over BPA’s plans to apply commercial readiness criteria.

“Developers in the queue have generally sunk millions of dollars into developing their projects,” Eric Christensen, an attorney with Beveridge & Diamond PC, which represents PRITCA, told RTO Insider. “The fact that developers are willing to put their own money on the line demonstrates that projects are commercially viable,” Christensen said.

A more appropriate way to deal with the queue would be to study transmission requests in batches based on existing queue order, Christensen argued. He said this approach would allow viable projects to have a path forward to firm transmission while allowing unserious requests to exit on their own accord.

Because the proposals are new, it’s unclear whether lenders have had time to analyze how they could impact investments, Christensen said.

“We talk with financiers regularly, and one of the big variables in financing decisions is a certain path to [long-term firm] transmission,” Christensen added. “If BPA goes forward with the current proposal, we expect to see large financing cost increases or an unwillingness to provide financing, due to the uncertainty these changes create.”

PUD Support

However, in public comments submitted to BPA, public utility districts have supported readiness criteria.

For example, Mason PUD said it “generally supports the addition of readiness criteria, so encumbrances are not provided for requests that will likely not convert to service. This will create an actionable queue [that] only includes mature long-term transmission service requests.”

Grant County PUD said it “supports the development of additional and clarified readiness criteria in order for TSRs to remain in the queue.”

“Unknown and New-Point [Points of Receipt/Points of Delivery] should be deemed speculative and removed from the queue until and unless new procedures are developed to accommodate such PORs/PODs in a realistic and timely manner,” Grant argued.

Colorado regulators have approved Tri-State Generation and Transmission Association’s plan to add 1,657 MW of new resources from 2026 to 2031, despite objections about the inclusion of a new natural gas plant.

The Colorado Public Utilities Commission voted 3-0 on Aug. 1 to approve the plan.

New resources in the plan include 400 MW of wind, 300 MW of solar and 650 MW of battery storage, along with 307 MW from a new natural gas plant in Moffat County in northwestern Colorado. The battery resources will be Tri-State’s first experience with battery storage systems.

In addition, Tri-State plans to replace turbines at the J.M. Shafer gas-fired plant to boost capacity.

The 1,657 MW of resources were included in Tri-State’s preferred portfolio, one of six analyzed in the implementation report for its 2023 electric resource plan (ERP). The report follows commission approval for Phase 1 of the ERP and a competitive bid process.

Another plan, referred to as Portfolio 6, excludes the new gas plant but increases battery storage to 1,175 MW, for a portfolio total of 1,900 MW. That plan also includes new turbines at Shafer.

Tri-State chose its preferred portfolio “as a result of the portfolio’s overall performance across the reliability, environmental and financial categories,” the Colorado-based power cooperative said in its implementation report.

The preferred portfolio was the least-cost option based on the present value of revenue requirements (PVRR), not including the social cost of emissions. The PVRR of the preferred portfolio would be about $88 million less than that of Portfolio 6.

Like all the portfolios analyzed in the implementation report, the preferred portfolio meets reliability targets. It achieves an 80% reduction in greenhouse gas emissions in Colorado in 2030 relative to 2005 levels.

“However, the other portfolios analyzed result in significant, unnecessary financial burdens by aggressively pursuing resources with high transmission interconnection upgrade costs” not needed to achieve the same benefits, Tri-State said.

The new resources are needed in part due to the retirements of the Craig and Springerville coal-fired power plants, slated for 2028 and 2031, respectively.

“Retirement of dispatchable coal resources cannot be affordably or reliably replaced solely with semi-dispatchable resources,” Tri-State said.

Commission Chair Eric Blank said he understood the resource diversity benefit of natural gas.

“For me, given our lack of rate regulation over Tri-State, I don’t think we should be substituting our judgment for that of the utility when there’s a tough choice to be made between competing portfolios where either could be deemed reasonable,” Blank said.

Commissioners also agreed with Tri-State that “time is of the essence” for procuring new resources due to a “volatile” market for renewable energy equipment and recent federal tax and trade actions.

Non-gas Portfolio

Other parties had urged Tri-State to choose Portfolio 6, which excludes the new gas-fueled power plant.

The Natural Resources Defense Council and the Sierra Club, filing together as “the conservation coalition,” said the present value of revenue requirements for Portfolio 6 was similar to that of the preferred portfolio when considered over the 19-year analysis period. Portfolio 6 had the lowest PVRR when the social cost of emissions was included, they said.

Portfolio 6 would result in lower GHG emissions for Tri-State “for little to no incremental cost,” the coalition said in a filing. The groups noted that Tri-State must eliminate its Colorado GHG emissions by 2050.

The groups also questioned the excess capacity resulting from the new gas plant and the “explicit assumption that Tri-State will overbuild capacity in order to sell into the market.”

“The commission’s rules, and prudent utility planning, simply do not countenance a regulated utility operating like a merchant generator in the way Tri-State proposes,” the coalition said.