As the world faces “unpredictable and chaotic times,” Midwest Reliability Organization Board Chair Dana Born reminded directors of the ERO’s role in ensuring stability of vital electric services.

Addressing MRO’s quarterly Board of Directors meeting Aug. 21, Born mentioned some of the dramatic events that have occurred since their previous meeting, such as the blackout on the Iberian peninsula that left the entire population of Spain and Portugal without power for up to 18 hours. (See Lauby Says U.S. ‘On the Right Track’ After Iberian Blackout.) However, she told attendees to keep their minds on the future and look for solutions, rather than pining for an imagined better past.

“At recent NERC meetings … I put little stars in my book [every] time people said that we really have made great progress. We have to remind ourselves of that, because there is so much work to do ahead,” Born said. “The real question is not how do we go back, but how do we move forward with clarity, conviction and a sense of purpose — our ‘why,’ and the significance of what it is that we do every day, who we are and why we are.”

CEO Sara Patrick echoed Born’s advice, noting multiple examples of collaboration across the ERO Enterprise. These included NERC’s Modernize Standards Processes and Procedures Task Force, whose proposal for using artificial intelligence to streamline the standards development process “supports both the MRO and ERO strategies to leverage advanced technologies to solve complex problems.” (See NERC Task Force Members Share Standards Modernization Progress.)

Patrick also held up the regional entity’s work on developing new action plans for risks identified as “extreme” or “high” in its annual Regional Risk Assessment and efforts to establish a data analytics function at MRO as examples of a collaborative approach making long-term progress.

“The ability to collaborate effectively and strategically is essential for achieving sustained success,” Patrick said. “MRO’s role within the ERO Enterprise positions us to provide expert analysis and inform key decision-makers on how local policy decisions can affect reliability of the entire system.”

Directors Agree to New Conduct Standards

Thomas Graham, chair of the Governance and Personnel Committee, brought the meeting’s sole action item, a vote on revisions to MRO’s antitrust policy and standards of conduct. According to Graham, the updates were part of “an ERO-wide effort … to harmonize the MRO policies with [those] of NERC and all the other” REs.

Among the changes in the new policy are expansion of prohibited activities, to include:

discussing or entering agreements among competitors regarding prices, product design or other matters;

use of sensitive information like pricing or terms in discussions with current and potential vendors;

discussions or agreements not to compete for, hire or poach employees;

discussions involving wages or benefits for current or future employees with participants outside MRO; and

agreements or discussions thereof not to seek or bid for work, grants or funds.

In addition, several existing entries on the prohibited activities list were updated to provide more clarity, such as the addition of language specifying that current and future pricing information is not to be discussed by MRO participants. Language on permitted collaboration between REs and NERC also was added, and the antitrust compliance reminder read at the MRO’s meetings was updated too. The new policy was approved without objection.

Later in the meeting, Tasha Ward, MRO’s director of enforcement and senior counsel, presented the RE’s semiannual report on its compliance monitoring and enforcement program (CMEP). Ward observed that MRO has seen a steady drop in incoming noncompliances annually over the past four years, with 169 violations reported to date in 2025 after 341 in 2022, 279 in 2023 and 261 in 2024.

A growing percentage of violations have been submitted via self-reports and self-logs rather than compliance audit, indicating that “entities are looking at their programs and actually submitting the issues that they find … for review by the MRO team,” Ward said. She also pointed out that a majority of open noncompliance cases in MRO’s inventory are less than a year old and only 21% are more than two years old, indicating an improvement in efficiency of noncompliance processing.

MRO’s next board meeting is scheduled for Dec. 4, 2025.

INDIANAPOLIS — The tone of Infocast’s 2025 Midcontinent Energy Summit was noticeably apprehensive compared with last year, owing to political and regulatory uncertainty, load growth ambiguity, fluctuating tariffs and a pending complaint against MISO’s long-range transmission plan.

MISO Senior Vice President Todd Hillman opened the Aug. 19-20 event in Indianapolis by recognizing the unpredictability wrought by ever-changing tariffs, growing data center demand, a rollback of environmental rules and even the surprise move of a Republican president appointing a Democrat to lead FERC.

“We’re not sure what ‘new normal’ is. We’re trying to figure that out,” Hillman said, speaking for MISO’s staff.

Hillman said MISO is trying to “get out of the way” in the rush to bring new data centers online. He noted the footprint could experience load growth of 60% in the next 10-15 years. Currently, almost half the transmission project requests the RTO receives are marked for expedited study treatment and are often meant to serve growing load, he said.

“They’re coming, and they’re coming fast and furious,” Hillman said. “The dog has truly caught the bus.”

“We’ll see how that plays out,” he said, offering no other comment.

Hillman said he wouldn’t guess at upcoming actions from the White House.

“Unless we have a cocktail break in the morning, I’m not going to go there,” Hillman joked.

He similarly refused to take a stab at potential next moves from Congress.

“Again, not enough beer in the bar,” he joked.

However, after being asked by the audience, Hillman said President Donald Trump’s One Big Beautiful Bill Act is likely to impact the 171 GW of generation interconnection requests MISO fielded in 2022. The record-breaking surge of applicants was almost exclusively composed of renewable energy and battery storage projects.

“I don’t know yet, but anecdotally, I think it will be significant,” Hillman said of the impact.

Hillman also promised MISO “will get better” and create more viable market participation rules for energy storage.

The RTO’s generator interconnection queue totals about 300 GW. Another 59 GW of projects have approvals to interconnect but are experiencing construction delays.

DOE Intervention and Load Growth

Brad Pope, director of legal and regulatory affairs at the Organization of MISO States, said the DOE’s involvement in fossil fuel plant retirements is “certainly a new element we’re grappling with.”

Pope pointed out that J.H. Campbell’s retirement was comprehensively examined before it was announced. He added that the $29 million bill the plant accumulated over its first 38 days of extended operations makes customer affordability a challenge.

“This isn’t just something that’s a local impact,” Pope said. He noted FERC’s decision that the cost of keeping the plant online be spread across all MISO Midwest participants means other states have no control over incurring costs.

However, Pope said “there’s a whole host” of new technologies, including HVDC lines and grid-enhancing technologies, and new procedures — including MISO’s expedited queue lane — that state regulators are also fitting into the RTO’s tapestry.

Illinois Commerce Commissioner Stacey Paradis said Illinois is concerned about how OBBBA could affect the goals of the state’s Climate and Equitable Jobs Act (CEJA). She said that so far, Illinois is lagging in reaching its 40% renewable target by 2030, and the state may open a new long-term procurement plan to secure more solar. Paradis added that the federal pullback of incentives for clean energy should make the next few years “interesting.”

Paradis noted that DOE hasn’t yet moved to keep plants on in Illinois and derail CEJA’s mandate that coal and gas generating units achieve zero emissions or close by the end of 2045 at the latest.

Paradis said non-disclosure agreements from data center developers are a stumbling block to efficient planning for regulators, utilities and RTOs. She said it’s a safe bet that if a data center is engaging Illinois about accommodating its load, chances are it’s also holding conversations with Wisconsin, Indiana, Michigan or even Missouri.

In some cases, non-refundable deposits of a few million dollars aren’t enough to deter developers from simultaneously courting multiple locations for a single project, she said.

“For some of them, that’s not even pennies on the dollar,” Paradis said. “We don’t want to overbuild. We don’t want to burden our customers with billions. We need to figure out what’s real.”

Indiana Utility Regulatory Commissioner Sarah Freeman said load growth projections have come into sharper focus compared with 18-24 months ago.

“They’re still not on a level to which I would risk the pocketbooks of my ratepayers, my fellow Hoosiers,” Freeman said. “The speed at which everything is moving does increase the risk of stranded assets.”

“Utility commissioners are risk managers,” Pope said, adding that the “truth is somewhere in the middle” for recent load forecasts.

‘Chaos’

Other panelists said OBBBA has introduced unprecedented uncertainty in the developer space.

“It’s chaos right now,” EDF Renewables Senior Director of Transmission Policy Temujin Roach said of today’s political climate. “We need to know what the hurdles are going to be. … You’re going to have to step back from the [federal government] and the executive branch as much as you can and work with the states.”

Roach advised renewable developers to employ that tactic for the three-year remainder of the current presidential administration, or however long it lasts.

He said generation developers are in a new environment where they must be more circumspect when submitting projects for interconnection study.

“We have to have quality and confidence in our projects. You can’t do the ‘spray and pray’ process we did for a while,” Roach said. “Are we still going to lose some projects? Sure.”

Roach said MISO’s 59 GW of incomplete generation is often “thrown in developers’ faces.” He acknowledged that developers weren’t as disciplined a few years ago and said interconnection procedures were likely too lenient to discourage speculation.

Roach noted also that the industry must do all it possibly can to increase use of energy storage, demand response and grid-enhancing technologies. He said grid planners cannot continue with no end in sight to prescribe billions of dollars of lines. At some point, he said, consumers will be unable to shoulder the costs.

“We’re going to have to explain how we’re being efficient with billions and billions of dollars,” he said.

Developers Back MISO Long-range Tx

However, Roach said the energy industry throughout the Midwest is relying on MISO’s $22 billion second package of long-range transmission lines to manage load growth and accommodate future generation plans. He said there comes a point where stakeholders should consider the transmission portfolio finished and move forward, referring to the recent five-state complaint at FERC. (See Five Republican States File FERC Complaint to Undercut $22B MISO Long-range Tx Plan.)

“It just turns into a death spiral of restudies. If we keep looking backwards and keep restudying, we’ll never move forward. Hopefully, FERC sees it that way,” Roach said. He added that stakeholders can always advocate for changes on the next MISO planning exercise.

“Yes, transmission is useful. I have no other comment. Ask me again in a year,” Robert Frank, a utility financial analyst at the North Dakota Public Service Commission, said dryly.

The North Dakota commission spearheaded the complaint against MISO’s second long-term portfolio.

Multiple developers said MISO’s long-range transmission planning makes the footprint more attractive for project development.

Anthony Doering, a senior director of interconnection and transmission at independent power developer MN8, said generation developers are working their hardest to bring the most viable projects forward. But developers are reliant on MISO, regulators and transmission companies to get the long-range transmission built on time, he said.

David Ticknor, senior interconnection engineer at RES Group, said MISO’s second long-range transmission portfolio is poised to support load additions, fleet change and reliability. He said it’s difficult to quantify reliability benefits of transmission, but MISO did a commendable job in its benefits analysis.

“I think it’s one of the coolest transmission buildouts we’ve seen in a long time,” Ticknor said.

However, Ticknor said his company is keeping a “keen eye” on the recently filed complaint from the five states against the portfolio.

“The cost allocation point is what it always comes down to,” he said, adding that MISO did a good job of planning despite not being able to solve all issues on the grid with a single transmission package.

Doering advised RTOs not to “cost-allocate the generators for your backbone transmission projects.” He said it’s difficult to get companies to sign on to power purchase agreements when potential generation projects are expected to entirely cover the cost of large transmission, with costs not commensurate with use.

“The need [for transmission] is already established. We don’t need to punish generators. We need to allocate the marginal impact of their use of the facility,” Doering said.

Ruchi Singh, vice president of interconnection and transmission at Brookfield’s Urban Grid, said if MISO planned transmission to increase capacity along the Midwest-South transfer constraint, it would open several possibilities to generation developers.

Swift Current Energy senior vice president Jim Marett said MISO is the easiest RTO to interconnect into today. He said although it’s slow and expensive, the MISO queue doesn’t experience the “sudden stops” that occur in other RTOs.

Development Becomes Trickier

“Development hasn’t been easy in the past year or so,” conceded Erik Ejups, director of power marketing at EDF Renewables. He said it’s become easy for a “small opposition group” to have an outsized impact on a solar project’s chances.

Foss and Co.’s Dawn Lima said OBBBA has set off a growing perceived risk from investors, who now request grandfathered projects whose construction started in 2024 and will be complete around 2026 or 2027.

Marett said there are enough renewable projects in the beginning stages or that will kick off physical construction before Sept. 2 (a federal deadline for wind and solar projects that plan to use the 5% safe harbor rule for claiming tax credits) to keep developers busy for the next few years and act as a de facto grace period for absent incentives. But he said growing capex costs will likely eat into developers’ margins. Fortunately, Marett said, data centers seem to have an appetite for new generation, even if it’s more expensive.

“What we’ve noticed is that an upgrade cost that would have gotten a project thrown out of the pipeline in 2017, we’re now ecstatic about. It’s a little bit more of a high-stakes poker game,” he said.

Conductor Solar CEO Marc Palmer said solar, storage and distributed energy resources “particularly got a gut punch” with the federal phaseout of incentives.

Palmer predicted that the remainder of 2025 and 2026 will contain strong construction trends, with a dip over 2027, followed by a recovery as costs of the assets naturally drop.

“We expect that to start bouncing back in time without any additional policy changes,” Palmer said. “We think the next 10 years are going to [see a] transition to value-driven growth, which is going to lead to a healthier market overall.”

Nick Panko, vice president of tax compliance firm CFO Services, said he expects the “emotional response” to the bill to wane.

“Every four years, you’re used to the swing,” agreed Brad Tyson, a vice president at Santander. Tyson said recent IRS guidance that laid out the transition in tax credits was a “small win” for renewable developers. He said some developers who braced for a tight, two-year shift breathed a sigh of relief when they found there would be a pathway to four-year safe harbor provisions. (See IRS Guidance on Wind and Solar Credits Not as Bad as Feared.)

Under OBBBA, wind and solar projects can qualify for the phased-out clean energy production tax credit and clean energy investment tax credit if they are placed in service by the end of 2027 or begin construction before July 4, 2026.

Panko said by the 2027 deadline, the U.S. will then gear up for another tax policy shift under a new presidential administration.

Cons Before Pros

John Davies, CEO of the eponymous public persuasion firm Davies, said this moment embodies the Chinese curse — not a proverb, he stressed — “May you live in interesting times.” He said for many, it’s challenging and for some, it’s a crisis.

“We look at this time as an opportunity for good companies, good players to make advances,” Davies said.

Davies said renewable projects, which often enjoy massive public support, fail because companies neglect to engage properly with the public. Davies said it may seem counterintuitive, but project developers should acknowledge the cons of a project before publicizing the pros to build credibility.

“If you can acknowledge, then contrast, you’re going to win every time,” he said.

Davies said currently, wind developers have the biggest perception problem, with more negative online articles available than positive.

“They have given up the web,” Davies said.

Davies said the people who have a “not in my backyard” attitude are either rational, irrational, or fearful of unknowns of the infrastructure or potentially being disrespected.

“They decide to be crazy because that’s what their political party tells them to do,” Davies said of the irrational types. He advised companies to listen to communities, perform outreach and cultivate relationships.

Davies advised against developers creating a social media page for projects, saying it’s a surefire way to create a hot spot for protesters. He joked that Mark Zuckerberg’s office contains a graveyard of renewable energy projects.

Brian Ross, vice president of renewable energy at Great Plains Institute, said every community should consider itself a “host” community for clean energy. He said the clear delineation that once existed between host communities and strictly consumer areas is evaporating. Every community contains the potential for solar energy, he said.

Ross said GPI is conducting campaigns where the nonprofit approaches municipalities to “soften the ground” and ask residents what they want from inevitable renewable projects versus what they dislike about them.

“Once you get them talking about what they want, the objections start to diminish,” Ross said. He said community members begin to associate projects with funding for local programs rather than usurping farmland.

Ross said developers might have to contend with lingering mistrust because developers previously publicized a project in a community, then vanished without explanation when upgrade costs jumped too high. He said those kinds of gaps are common in a “capitalistic landscape.”

Ross also said GPI as a rule doesn’t mention that a particular project will help alleviate climate change unless the community already has established climate goals. He said many communities view the “clean energy economy as thrust upon them.”

Hillman said, at the end of the day, the industry’s end goal is reliability. He said industry players need to have “elevated debates” in an era of “I’m right, you’re wrong.”

“Use phrases like, ‘Tell me more;’ ‘What’s your perspective?’ Or ‘While I don’t quite see it that way, I can understand where you’re coming from,’” Hillman urged.

Former FERC Chair Neil Chatterjee says implementation of the Inflation Reduction Act went too far in limiting fossil fuels and implementation of the One Big Beautiful Bill Act may limit renewables too strictly.

Both sides of the aisle need to recognize that a true all-of-the-above approach is needed in this time of growing power demand and potential inadequacy of generation, he said.

Chatterjee and former Texas Land Commissioner George P. Bush offered their thoughts on the impact of OBBBA on the energy sector during an HData webinar Aug. 21.

Bush, now a strategist in Texas, said the impacts of the bill are many and significant: “This is definitely going to be the consequential bill for Trump 2.0. It’s people like Neil and I that make a living helping people interpret it.”

Chatterjee said the present situation — rising power prices amid rising demand — is not a result of OBBBA’s cuts to renewable energy subsidies, it is due to the Biden administration accelerating generation retirement prematurely.

“I think the risk going forward for the [Trump] administration and for congressional Republicans, I don’t want to see them make the same mistake, quite frankly, that the Biden administration did,” Chatterjee said. But it is starting to happen, he added: “The Trump administration, since passage of the OBBBA, has taken a number of steps via executive orders and agency actions to really hinder the deployment of clean energy resources.”

Bush said the energy industry and its regulators need to rethink their operating model.

“My hope is that jurisdictions are going to cut red tape and allow for more behind-the-meter generation, allow the private sector — of course, in a very thoughtful way — to generate this power that can be used by large load users, namely in industries that we’ve talked about,” he said.

“I think a lot of utilities and districts are going to become entrepreneurial and help underwrite these projects or just administer the underwriting of the project.”

America cannot win the AI race, meet rising demand and keep prices affordable without a mix of natural gas, wind, solar, geothermal and nuclear, Chatterjee said. And those new gigawatts of power need to be optimized with transmission expansion, grid-enhancing technologies, energy efficiency, demand response, virtual power plants and distributed energy resources.

“It all needs to be on the table, and I’m optimistic that we can have conversations at both the federal level and the state level, and kind of come together to figure out what the path forward is.”

Bush observed: “I do not envy people that are now in this business, the regulator, and making sure you’re keeping power prices low enough for your constituents and helping underwrite the process for these massive asset projects.”

States and regions have long wrestled with market regulation, Chatterjee said, whether they have traditional vertically integrated utilities or competitive wholesale power markets. Neither model is perfect, he said, and both have challenges.

These new challenges will lead to the design of more innovative mechanisms, he predicted.

“Whenever you have big pieces of legislation, whether it be the IRA or the OBBBA at the federal level, that tends to prompt reactions at the state level,” Chatterjee said. “And so I fully anticipate in the coming years to see states who benefited from OBBBA or those who had their concerns with it, potentially modify policies within their own parameters to account for the shifting policy, legislative and market energy landscape.”

Texas has the second-largest energy storage capacity of any state and, not coincidentally, the second-largest solar capacity and the largest wind capacity.

Bush predicted storage capacity will grow: “I really do think commercial battery storage — a lot of folks in renewables will pivot to that to store the renewable capacity that they’ve already built.”

Bush said OBBBA’s impact on the industry will be wide-ranging, particularly in a state like Texas, where a massive amount of capital has been expended on renewables.

“We got a lot of calls in our practice with respect to, ‘How do we preserve these tax credits? We made these assumptions, we raised capital from outside investors, and what does that mean?’ And so there will be kind of an expedited time frame to work with, but the private sector, I think, is going to stand up to this challenge.”

Chatterjee had a similar take, saying the picture still is evolving a week after the IRS guidance on wind and solar tax credits was issued, and some businesses will be able to evolve with it.

“I think maybe there were some bad actors that were created out of the policy that came from the Inflation Reduction Act,” he said. “Folks chased the subsidies and got into the field without necessarily having a coherent business model, a lot of those bad actors are probably going to fail in light of the policy changes. But I think the companies, particularly on the clean tech side, that come through this, will come through stronger than ever, and will diversify their business model away from subsidies to provide that power and reliability.”

IESO will expand its industrial demand-side management program in September, increasing funding and allowing both larger and smaller participants than currently permitted.

The electric demand side management program (eDSM) incentives are intended to help industrial, municipal, institutional and health care organizations to implement “proven, commercially available” energy savings technologies that would otherwise be too costly.

The new program will triple the incentive cap to $15 million from $5 million per project, and allow participants five years to complete installation, up from three years.

The minimum savings to qualify will be reduced to 600 MWh/year from 2,000 MWh/year. For the first time, the program also will provide funding for feasibility studies (50% of total costs, up to $100,000).

The grid operator also is making the application process simpler, with a single sign-off application and a first-come-first-served intake.

The program is part of IESO’s $1.8 billion 2025–2027 eDSM plan, which is forecasted to reduce peak demand by 900 MW and save 4.6 TWh of electricity by 2027. Ontario, which is projecting 75% load growth by 2050, plans to spend $10.9 billion under a 12-year funding commitment that began in January, tripling the province’s historical EE spending. (See Ontario Integrated Energy Plan Boosts Gas, Nukes and IESO Seeking Feedback on Commercial HVAC Demand Response Program.)

The new industrial program was informed by the province’s experience under its Save on Energy program, a review of industrial programs in other regions and stakeholder feedback, Nicole L. Hynum, supervisor of IESO’s Custom Business Programs, said in an Aug. 21 webinar.

“Some customers [in the industrial energy efficiency program] did identify some challenges with the program, including funding cycles that maybe didn’t align with your capital planning cycles [and] a more risky application process that didn’t work for industry because it was competitive,” Hynum said. “The thresholds for the project size were … too large for some industries, and the incentive levels were competing with other demand-side management programs and were less than those other competing offers. So, you know, it impacted participation.”

Under the former program, incentives were proposed by participants based on their project needs. The new program will pay the lesser of $300/MWh ($450/MWh in areas having “local needs”), 75% of eligible project costs or the amount that would provide a project payback of one year.

A project that saves 5,000 MWh/year in a local needs area would receive incentives of up to $2.25 million (5,000 × $450), subject to the eligible cost payback test and a $15 million cap.

Participants can seek an exception to the $15 million cap based on their business case.

Eligible projects must save electricity for at least four years after the end of a one-year measurement and verification (M&V) reporting period.

Participants will receive 50% of their project incentive based on a review of their first-quarter M&V report and the balance after a review of the year-one M&V report.

Ineligible to participate are:

Electric generation projects, except approved waste energy recovery where the recovered energy offsets the facility’s own load;

Behind-the-meter storage, unless the storage improves the efficiency of other project components, resulting in net electricity savings;

Lighting projects (which can receive funding through the Save on Energy Instant Discount Program);

Fuel switching, unless approved by IESO; and

Local distribution company infrastructure efficiency measures.

The final design of the program is expected to be approved in early September, with the program launching late in the month.

“This is year one of a 12-year framework,” Hynum said. “We will no doubt be enhancing this program to meet evolving marketplace and electricity system needs.”

Yeah, that one. The Wall Street Journal’s op-ed broadside on Gov. Phil Murphy, New Jersey and PJM.

We’ll get to the punchline later, but let’s start with some reality checks.

Reality Checks

Energy independence in the past? Here’s the op-ed claim: “By 2016, New Jersey achieved energy independence … partially fueled by Pennsylvania gas.” That is a plain contradiction in terms. Not to mention that New Jersey’s gas power plants are totally fueled by out-of-state gas.

And, come to think of it, I haven’t noticed any uranium mines in New Jersey that could fuel New Jersey’s nuclear plants.

And even if the op-ed claim was meant to refer to New Jersey power plants (not their fuels), it’s still wrong: In 2016, New Jersey had 16,797 MW of generation capacity and 19,012 MW of peak demand (Slides 7 and 25), so New Jersey wasn’t “energy independent” no matter how you look at it.

Steve Huntoon

Coal plants shut down? How about the op-ed claim that New Jersey “shut down” all its coal plants? Coal plants in New Jersey shut down voluntarily because of poor economics, with the last of them, Logan and Chambers, shutting down in 2022.

Increased reliance on wind and solar? The op-ed claims that New Jersey has “increased its reliance on intermittent wind and solar power.” Actually, solar power has had a trivial increase from 117 MW to 181 MW, and wind power has changed, a la Mr. Blutarsky, from zero-point-zero MW to zero-point-zero MW. (See Slide 7 and Slide 8.) So much for facts.

Supply-side mismanagement? New Jersey is alleged to have had supply-side mismanagement leading to a 12% decrease in generating capacity. That is a smaller decrease than the regional decline of 20% that the op-ed claims later.

Blue-state PJM? Then there’s the claim that PJM has had the same bad policies as New Jersey because PJM’s “leadership” is driven by its “largely blue-state makeup.” This claim is baffling on multiple counts. PJM is not governed by states’ political leadership — instead by an independent board and “stakeholders” like retail customers, generators and utilities.

PJM is regulated by FERC. PJM states are not even “largely blue” — the legislatures are divided evenly, six red, six blue and two split, between its 13 states and the District of Columbia. With legislatures and governors considered it’s four red, five blue, and five split.

Facts are stubborn things.

What Actually Happened?

So what actually happened over the past 10 years? Low wholesale energy and capacity prices incented inefficient generators (mostly coal) to retire in New Jersey and across PJM. And they did. The PJM markets served consumers well, as summed up in a New Jersey BPU report: “The regional competitive market has performed well in offering secure, low-cost supply to New Jersey.” (See Page 9.)

The New Jersey average residential rate increased by 23.3% from 2016 to 2024 (less than 3% per year).

Data from the same Energy Information Administration chart shows that residential rates in the rest of PJM increased by an average of 27.9% over this same period. So the New Jersey rate increase was less than the rest of PJM. And the residential rate increase in the U.S. overall was 31.3% — so the New Jersey and PJM increases were both less. Please check out the numbers yourself.

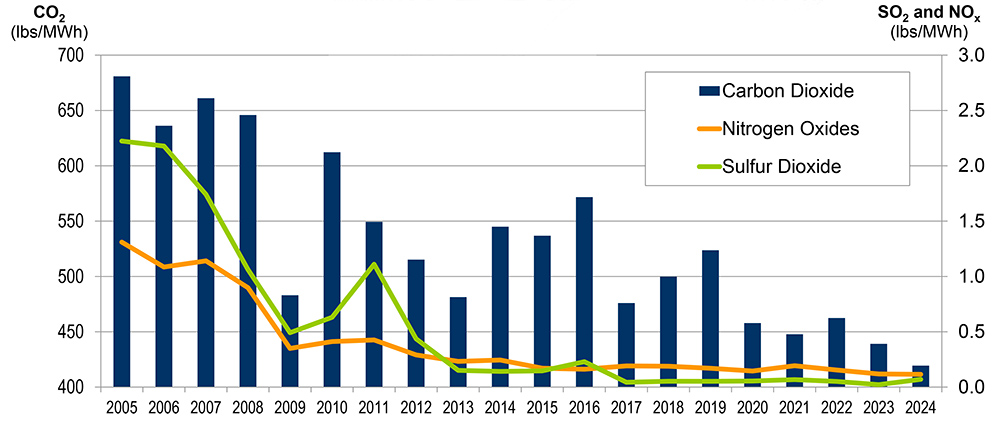

And, as a bonus, emissions in PJM have declined dramatically, as this chart shows. (See Slides 31 and 32.) Even if you don’t care about carbon emissions and global warming, you should at least welcome the amazing declines in nitrogen oxides and sulfur dioxide.

New Jersey average emissions | PJM

Now we’re in a new supply-demand situation from data centers driving big increases in forecasts of future demand. (See Slide 20.) This is increasing capacity prices. The higher prices are designed to attract new generation to meet that future demand. It’s that simple. And though tough challenges loom, including higher residential rates, thus far it’s working as designed.

By the way, something else you’d never guess from the op-ed: The capacity price increase for New Jersey is no less than that for the rest of PJM.

Leaving PJM

Now that we understand the fundamentals of where we were and are, let’s consider the op-ed’s punchline that New Jersey should leave PJM, and go it alone.

Hmm. New Jersey has 13,388 MW of generation capacity and 21,221 MW of peak demand. (See Slides 8 and 21.) So it’s short 7,883 MW.

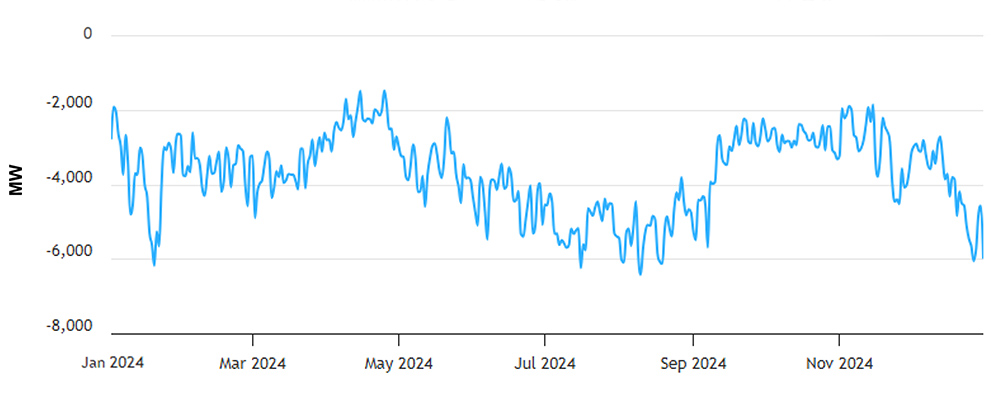

New Jersey net energy import/export trend | PJM

Here’s the chart of New Jersey’s electricity imports to meet customers’ needs. (See Slide 28.) You’ll notice that imports vary between 2,000 MW and 6,000 MW throughout the year. That means that if New Jersey left PJM to be on its own, there would be rolling blackouts around the clock, varying from 9% of New Jersey households to 28% of New Jersey households. Brilliant!

New Natural Gas and Nuclear to the Rescue?

The op-ed goes on to suggest that New Jersey could avoid shortages and blackouts with new natural gas and new nuclear generation. Sorry, no.

The op-ed says new natural gas plants could be delivered in New Jersey within three years — that’s not only wrong, but irrelevant. New natural gas supplies couldn’t be delivered to New Jersey for 10 years at best, as this timeline for the Northeast Supply Enhancement project illustrates. The last pipeline project proposed to serve New Jersey, the PennEast Pipeline, was proposed in 2014; targeted completion became 2023 before it was abandoned in 2021. So good luck with that.

New nuclear is even further off, not to mention prohibitively expensive (before cost overruns), as I’ve discussed before. As Brattle recently advised the New Jersey BPU: “If it chooses to embark on an ambitious new nuclear strategy, New Jersey may have a new, probably small, nuclear unit online by the late 2030s or 2040.” (See Page 6.) Oh boy, one small nuclear unit in 15 years or so. And good luck with the siting, especially in northern New Jersey, where the new generation would be needed.

The Upshot

New Jerseyites would suffer through many years of rolling blackouts, wondering why The Wall Street Journal promoted leaving PJM.

Columnist Steve Huntoon, a former president of the Energy Bar Association, practiced energy law for more than 30 years.

The U.S. Department of Energy has ordered the J.H. Campbell Generating Plant to remain available another 90 days, saying its capacity is needed to maintain MISO grid reliability.

Consumers Energy had planned to retire the 1,420-MW coal-fired facility in southwest Michigan on May 31, but DOE on May 23 issued an emergency order (202-25-3) under Section 202(c) of the Federal Power Act ordering it to remain ready to operate because of a shortage of electricity and capacity to generate electricity. (See DOE Orders Michigan Coal Plant to Reverse Retirement.)

That order expired at midnight Eastern time Aug. 21.

Energy Secretary Chris Wright issued the follow-up order (202-25-7) at 8:50 p.m. Eastern time Aug. 20; it expires Nov. 19.

In his Aug. 20 order, Wright indicated the generation shortfall in MISO is likely to continue.

President Donald Trump declared an energy emergency on his first day in office, and his Cabinet agencies have been scrambling to rejigger energy policy toward the fossil fuels he favors.

One of their stated priorities has been halting retirement of aging fossil-burning plants.

In a news release, Wright cited seasonal outlooks by NERC and NOAA warning of high temperatures in the Midwest as well as resource adequacy projections by MISO itself.

“The United States continues to face an energy emergency, with some regions experiencing more capacity constraints than others. With electricity demand increasing, we must put an end to the dangerous energy subtraction policies embraced by politicians for too long,” he said.

“This order will help ensure millions of Americans can continue to access affordable, reliable and secure baseload power regardless of whether the wind is blowing or the sun is shining.”

Section 202(c) has been a lightly used provision historically. Just 11 orders were issued during the Biden administration, all of them weather-related. This compares with nine by Wright since mid-May, only one of which was weather-related.

It also has been unpopular with environmental advocates.

Sierra Club Beyond Coal Campaign Director Laurie Williams said Aug. 21: “By illegally extending this sham emergency order, Donald Trump and Chis Wright are costing hardworking Americans more money every single day for a coal plant that is unnecessary, deadly and extremely expensive.”

Earthjustice Senior Attorney Michael Lenoff said: “Chris Wright is not a Soviet-era central planner, but his new order suggests he would fit right in. The order purports to override the considered judgment and careful work of many federal, state and regional bodies who actually have authority to keep the lights on. In their place, Secretary Wright blunders in.”

In a statement, MISO said it will “continue coordinating with Consumers Energy to comply with the order.”

But MISO again stressed that J.H. Campbell did not clear the planning resource auction and is unnecessary for resource adequacy in the 2025/26 planning year.

“MISO’s 2025-2026 Planning Resource Auction indicated adequate resources to meet anticipated demand. State regulators along with utilities have the responsibility of ensuring resource adequacy. MISO remains focused on reliably operating the grid using the resources our members provide, while working closely with stakeholders and regulatory partners, providing visibility into system needs and sending market signals to inform long-term resource planning,” MISO spokesperson Brandon Morris said in a statement to RTO Insider.

MISO leadership previously has said it might have to navigate similar future orders from the federal government to prop up retiring coal plants.

MISO Director Todd Raba said MISO might have to navigate similar edicts in the future, with about 30 coal plants in the footprint. At MISO’s June board meeting, he said it’s a “critical topic that will have huge implications in MISO.”

Lawmakers, health professionals and other officials gathered near the plant in West Olive, Mich., on Aug. 12 to protest its extension. On Aug. 18, a small crowd of community members marched to U.S. Rep. Bill Huizenga’s office in nearby Holland, Mich., to again protest continued operations.

Consumers Energy said it was evaluating the order extension and expects to “continue operating the plant as required by DOE.”

“We have worked closely with MISO and have been operating in compliance with the order and MISO’s dispatch requirements. All power generated by the Campbell plant and other Consumers generating plants is supplied to the MISO grid. Specific details on recent generation are not publicly available at this time,” spokesperson Brian Wheeler told RTO Insider.

Wheeler also said the utility was “pleased” with FERC’s approval of an allocation that’s set to disburse cost recovery of the plant among the 11 states or portions of states in MISO Midwest.

Consumers Energy declined to comment on the coal plant’s usefulness so far over the summer or how the plant will fit into the MISO market over the fall.

Data from power analytics company Yes Energy shows the 1.42-GW plant has been used consistently since the beginning of August, averaging an 84-88% hourly capacity factor.

A group of industry insiders looking at ways to meet data centers’ electricity demand found a common thread within their varied opinions: The power sector and its regulators need to be a lot nimbler.

The United States Energy Association’s monthly virtual press briefing Aug. 20 focused on ways Big Tech is reshaping the electric utility sector or even upending it, with the potential for major data centers to add their own power generation.

Speakers drawn from the power and technology sectors fielded questions from a panel of journalists on what is at once a potentially lucrative and disruptive scenario facing the electric power industry.

Among the themes:

How much additional generation needs to be built to serve data center loads — or is this more of transmission issue?

It is both, said Tom Falcone, president of the Large Public Power Council. There also are the secondary issues of supply chain and workforce adequacy, permitting and retirement of existing generation.

After two decades of flat demand, unprecedented growth is projected, said Clinton Vince, head of Dentons’ U.S. Energy Practice. Further, the 24/7 nature of this demand also is unprecedented, he said.

Jeff Weiss, executive chairman of Distributed Sun and truCurrent, said the 20th-century grid that exists is not up to the task: “Electricity scarcity is upon us, and this is the new world for industrials, for data centers, for consumers, where electricity is not abundant and we need to manage sources of power.” Fortunately, he added, battery storage is bridging some of the gap.

Speed is the overriding issue, said Derek Bentley, a partner at Solomon Partners, and trends are not favorable. GE Vernova needs a five-year lead time to equip a new combined-cycle gas plant that then takes a couple more years to build, while renewables are intermittent and the target of policy changes. “But with the data centers, you can generally build a data center in 12 to 18 months.”

Karen Ornelas, director of large load program management at Pacific Gas & Electric, said PG&E has started a cluster process for new load requests, which has reduced the duration and cost of engineering studies.

Tom Wilson, principal technical executive at EPRI, said demand flexibility will help ease the crunch that is developing. EPRI’s DCFlex initiative has involved more than 50 entities in multiple sectors to demonstrate ways data centers can moderate that 24/7 demand.

Balancing Act

How do you balance the sharp increase in new load with the imperatives of affordability and reliability? How do you balance the needs of new data centers with those of existing residential and industrial customers?

There is a lot of uncertainty, Falcone said, “and so what you see is a lot of reforms happening at the state level and with individual utilities to better understand and also get some financial commitments that are longer-term.”

Weiss said the nation is trying to grow in the 21st century using a 20th-century utility system, a prescription for failure, and “the regulatory construct puts a lot of lethargy” in moving forward from that. “Everything we do takes 10 years or more. We need to figure out how to do everything in two years … and it’s critical to our economy that we do that.”

That’s why so many behind-the-meter partnerships are being formed, Bentley said. “Unfortunately, there isn’t just a silver bullet solution right now, and so it does require a lot of things, all coming together, a lot of constituents working together to solve the problem.”

Bud Albright, senior energy adviser at the National AI Association, reminded listeners that policy does not exist in a vacuum: “We need to get in front of the public at a grassroots level, to educate them if you will, to the benefits of bringing new power online wherever it is. As we all know, there’s huge pushback when data centers come in, the public saying, ‘Don’t take our power, don’t take our power. It’s going to drive our costs up.’”

Trump Card

President Donald Trump is pushing through significant policy changes in the energy sector. What is he getting right, and what does he need to improve?

Vince praised Trump’s moves on nuclear power, battery storage and delayed fossil retirements but added: “I think the discontinuation of credits and other limitations on the solar and wind industry is unfortunate.”

The president has correctly framed the issue, which is the need for a review of existing processes and significant changes, Falcone said.

Redland Energy Group Principal John Howes said: “I think the president has done some very good things. For example, he’s done a lot to eliminate some of the bias against fossil fuels which existed in the last administration.” More attention must be paid to permitting reform, he said, as well as to the foundational components of the system, such as transformers, and to its human component, through workforce development.

Disruptive Presence

If hyperscalers can move more nimbly and set up behind-the-meter generation more quickly, do they become a threat to utilities?

If someone wants to cut the cord and truly be off the grid, they can order the equipment and install it, Falcone said, and maybe reach the finish line more quickly. But otherwise, they need to operate within the same construct as everyone else attached to the grid.

Vince said some utilities are working well with Big Tech and finding solutions. But many are not, and capitalized hyperscalers are proceeding without them, taking an entrepreneurial approach. “The slower utilities, I think, will be disadvantaged tremendously,” he said.

It need not be mutually exclusive, Bentley said — a data center that builds its own generation may not remain permanently or entirely behind the meter or off the grid. “We’re seeing a lot of unique and tailored solutions … a lot of innovative structures.”

Wilson said flexibility and adaptability such as demand response or onsite storage will help: “Agility is not just being able to buy equipment faster, but it’s being able to be an asset to the grid, as opposed to a passive load.”

With NERC entering the final phase of a FERC-directed standards project to address reliability risks of inverter-based resources, the chair of NERC’s Standards Committee said the ERO aims “to use [its] resources efficiently and wisely” to meet the commission’s deadline.

Meeting via teleconference Aug. 20, SC members voted to move forward with two standards authorization requests (SAR) for the fourth and final milestone of Order 901, in which FERC directed NERC to develop requirements pertaining to the reliable connection and operation of IBRs. (See FERC Orders Reliability Rules for Inverter-Based Resources.)

Milestone 4 of the order mandates that NERC submit standards by Nov. 4, 2026, “addressing planning and operational studies for registered IBRs, unregistered IBRs and IBR-DERs [distributed energy resources] in the aggregate” (RM22-12). Previous milestones concerned IBR performance requirements, including voltage and frequency ride-through, disturbance monitoring data sharing and post-event performance validation.

The SARs approved in the SC meeting tackle planning and operational studies separately and already have been reviewed by NERC’s Reliability and Security Technical Committee. (See NERC RSTC Tackles Priority Projects in Quarterly Meeting.) With the committee’s approval, both SARs will be posted for a 30-day informal comment period, and NERC will solicit nominations for drafting team members for at least 15 days; the operational studies team will be designated Project 2025-03, while those working on planning studies will be Project 2025-04.

NERC Manager of Standards Development Sandhya Madan told listeners that considering the deadline, NERC has classified both projects as “high priority,” which the ERO applies to projects that address “significant” risks as identified by the following criteria:

subject of a NERC or FERC directive with a set due date;

identified as a priority in NERC’s work plan; or

recommended to address a specific risk by compliance feedback, stakeholder feedback or a study.

Also considered high priority was NERC’s project to revise CIP-015-1 (Cybersecurity — internal network security monitoring), approved by FERC during its June open meeting. (See FERC Approves NERC’s Proposed INSM Standard.) In its order approving the standard, the commission directed the ERO to require that utilities extend the implementation of INSM to electronic access control or monitoring systems and physical access control systems outside their electronic security perimeter, the electronic border around their internal networks.

To meet FERC’s deadline of submitting the revisions by Sept. 1, 2026, NERC solicited 19 nominations from industry and recommended appointing 15 nominees to the project team, including a chair, two co-vice chairs and 12 members. NERC Manager of Standards Development Alison Oswald said the ERO desired two vice chairs instead of the usual one “to make sure that there’s always someone from the leadership team that can be able to attend the [project’s] numerous expected calls and in-person meetings.”

Oswald also confirmed that nine of the 15 recommended members, including at least one member of the leadership team, will return from the team that drafted the original standard. The proposal passed without objection.

A proposal to appoint five candidates to supplement the team for Project 2017-01 (Modifications to BAL-003 — Phase 2), which has lost four members who are retired or no longer able to serve, sparked some discussion after Robert Blohm of Keen Resources suggested adding a sixth member to achieve regional balance. The aims of the low-priority project include addressing “the real-time aspects of frequency response necessary to remain reliability [and developing] measurements to incorporate real-time resource and load characteristics.”

Blohm said his proposed candidate, who like other nominees was not identified by name during the meeting, had “the most direct subject matter drafting team experience” of all the nominees. In addition, he pointed out that the five candidates recommended by NERC represented five of the ERO’s six regions and that adding this person would ensure all regions were represented.

Other members were reluctant to take up Blohm’s cause, with several indicating they trusted NERC’s vetting. Oswald said NERC felt the five recommended candidates had “the correct mix of regional representation and utilities that would be subject to the standard,” but suggested the remaining candidates “would be great additions as active observers on the project.” Blohm’s motion to add the candidate failed with 13 votes against and five in favor; a subsequent motion to approve NERC’s slate passed unanimously.

Finally, members agreed to authorize a 30-calendar day solicitation of nominations to supplement the team for Project 2022-05 (Modifications to CIP-008 reporting threshold), which has also seen four members depart since its inception in 2023.

FERC approved SPP’s tariff revision that establishes separate planning reserve margins for the summer and winter seasons, saying it will provide “more granularity” by recognizing the reliability differences between the two seasons (ER25-89).

“We find that having separate, seasonal PRMs will help align resource adequacy requirements with seasonal reliability risks, which have been increasingly occurring in the winter season,” the commissioners wrote in their Aug. 19 order. “Moreover, as SPP points out, separate PRMs will help ensure that [load-responsible entities] are appropriately planning for both seasons.”

FERC granted the RTO’s request for an Oct. 1 effective date.

SPP performs a probabilistic loss-of-load expectation (LOLE) study at least biennially to determine the PRM. It told FERC that its 2024 report identified a predominant loss-of-load risk in the winter because it included incremental cold-weather outages in the 2023 study that would increase with the additional incorporation of intermittent resources.

Under the grid operator’s resource adequacy requirement (RAR), staff first determine a PRM based on an LOLE study analyzing the ability to reliably serve the balancing authority area’s forecasted annual peak demand, based on a one-day-in-10-years loss-of-load standard and the accredited value of the footprint’s resources. LREs are responsible for owning or procuring the capacity to meet their seasonal non-coincident peak load plus the PRM.

The Arkansas Electric Cooperative Corp. (AECC), East Texas Electric Cooperative and Northeast Texas Electric Cooperative protested SPP’s filing. AECC expressed concerns that the 2023 LOLE study results failed to assign an LRE’s winter RAR proportionately to its contribution to cold-weather outages, saying the grid operator failed to support its move from an annual peak demand construct to a seasonal PRM framework.

AECC and the other two cooperatives asserted that the PRMs’ swift implementation prevented a “robust consideration” of alternatives by members during the stakeholder process.

FERC rejected the arguments, noting it already had found SPP’s seasonal RAR construct just and reasonable.

The commission found that SPP’s proposal to use expected unserved energy (EUE) as one of the determinants will produce a more robust PRM. It said EUE “provides data on the magnitude and duration of outage events and is impacted by changes in load shape and load peak duration” that differ from season to season.

SPP’s board approved the separate PRMs in August 2024 despite stakeholder concerns. The approval set a 36% PRM for the winter season and a 16% margin for the summer, effective for 2026/27 and 2026, respectively. (See “Board Approves 36% PRM for Winter over Stakeholder Objections,” SPP Board of Directors/RSC Briefs: Aug. 5-6, 2024.)

The grid operator’s stakeholders had recommended a 33% winter PRM.

Clean energy advocates are urging California lawmakers to restore funding to a fast-growing distributed energy program that can serve as a peaker plant alternative and showed its ability to support the grid during a test run.

Funding for the Demand Side Grid Support (DSGS) program is expected to run out this year and an estimated $75 million is needed to keep it going in 2026, representatives of more than 30 clean energy groups and companies said in a letter to state lawmakers.

The letter also calls for $50 million for the Distributed Electricity Backup Assets (DEBA) program, which incentivizes the construction of cleaner and more efficient distributed energy assets to be on-call for emergencies. DSGS and DEBA are California Energy Commission programs.

“At a time when affordability and reliability are under such strain, cutting these programs would take away proven cost-saving solutions just as they are most needed,” the letter stated.

The Brattle Group recently completed an analysis of DSGS, focusing on the program’s “Option 3,” in which battery owners agree to make their stored energy available to the grid during energy emergency alerts or when day-ahead prices go over $200/MWh. Participants sign up through DSGS providers, which include companies such as solar-and-storage providers Sunrun and Tesla Energy.

Participants are compensated based on the power they share with the grid.

“It’s not a subsidy. It’s not a giveaway or anything like that,” Edson Perez, a senior principal at Advanced Energy United, told RTO Insider. Perez is one of the authors of the letter to lawmakers.

The Brattle study, which was prepared for Sunrun and Tesla Energy, estimates that DSGS Option 3 will reach 700 MW of nameplate battery capacity in 2025 and grow further to 1,300 MW by 2028.

Besides boosting the grid, DSGS can save money. Brattle projected program net cost savings of $28 million to $206 million from 2025 to 2028. The lower figure assumes the program provides capacity value and some energy cost savings. Program costs are mainly the payments to participating battery owners.

The higher savings scenario assumes California is paying more than $200/kW-year for emergency resources and that tariffs and supply chain issues are increasing capacity costs. In that case, DSGS would be “a significantly lower-cost alternative,” Brattle said.

The Brattle study also assessed a virtual power plant (VPP) test event July 29 involving about 100,000 residential batteries. The batteries were primarily enrolled in the DSGS program, and the two main aggregators in the test were Sunrun and Tesla Energy.

“Aggregating home generation and storage produces a reliable, flexible energy resource that dispatches at the same scale as multiple peak generation plants to help meet soaring electricity demand,” Sunrun CEO Mary Powell said in a statement.

Although the governor’s proposed budget in January included money for the DSGS program, that funding disappeared in later budget revisions. Perez said those who signed the letter to key legislators would leave it up to the lawmakers to decide how to fund DSGS.

And at least one state senator has indicated his support for doing so.

Sen. Josh Becker (D), chair of the Senate Energy, Utilities and Communications Committee, discussed the DSGS program during an Aug. 19 oversight hearing on grid reliability.

“That’s a program that I think has had a great success,” Becker said. “We had a great virtual power plant success recently. We need to make sure those are funded.”