FERC on Aug. 25 approved CAISO’s Western Energy Imbalance Market (WEIM) implementation agreement with Imperial Irrigation District (IID).

The approved agreement specifies how CAISO will bring IID into the WEIM, including the costs and the scope of work involved. The commission’s order notes the ISO said the plan “adopts substantially similar provisions to WEIM implementation agreements previously approved by FERC” (ER25-2789).

Under the agreement, IID will pay CAISO a fixed implementation fee of $120,000, and either party can terminate the agreement for any or no reason after first engaging in good faith discussions for 30 days to resolve any differences. The agreement also outlines limits of liability, notices and dispute resolution language, among other elements.

CAISO and IID are also developing an implementation agreement for the ISO’s Extended Day-Ahead Market (EDAM). CAISO plans to admit IID into the WEIM and EDAM on the same day, no later than Oct. 1, 2028.

Located in Southern California, IID provides power to about 165,000 customers and operates more than 1,800 miles of transmission and 5,000 miles of distribution lines. IID in May announced its intention to join the CAISO markets, a move the utility’s, general manager, Jamie Asbury, said “is a significant step toward modernizing how we purchase and manage power.” (See Imperial Irrigation District Inks Agreement to Join CAISO Markets.)

In its order, FERC also granted CAISO a waiver request to allow IID’s WEIM implementation date to occur more than 24 months after the implementation agreement effective date of Sept. 2, 2025, which allows the utility to join the WEIM and EDAM concurrently in 2028.

“CAISO and IID will require more than 24 months from the requested effective date of the WEIM Implementation Agreement to undertake the implementation steps needed to allow for IID’s concurrent participation in WEIM and EDAM,” CAISO said in its filing with FERC.

The commission said it approved the waiver because CAISO “acted in good faith” by “promptly” filed the request shortly after the ISO and IID executed their agreement and “sufficiently in advance of the proposed effective date.”

Two laws signed by New Jersey Gov. Phil Murphy (D) aim to dramatically expand community solar and storage incentive programs as the state searches for new generation sources to help meet a predicted energy shortfall.

One of the laws, S4530, instructs the New Jersey Board of Public Utilities (BPU) to increase the capacity of community solar by 3,000 MW by 2029, or whenever the limit is reached. The state’s current allowed capacity is 150 MW a year, although a one-time measure increased it to 250 MW in 2025.

The second law, S5267, requires the BPU to launch an incentive program that would stimulate the development of “transmission-scale energy storage systems,” those with a capacity of at least 5 MW that are connected to PJM. The total project capacity would be 1,000 MW. In the first phase of the project, the legislation requires the BPU to approve projects with a capacity of at least 350 MW by the end of 2025 and approve the remainder by June 30, 2026. Eligible projects must have a commercial operations date of no later than Dec. 31, 2030, and have completed the PJM connection process to the system impact study stage.

Under the law, the BPU must allocate $60 million each year to the incentive fund.

“This legislation addresses real problems,” said BPU President Christine Guhl-Sadovy. “More New Jerseyans will get access to the benefits of expanded community solar programs — one of the best ways for residents to lower their utility bills while contributing to clean energy in the Garden State. And large-scale battery storage will strengthen our electric grid and keep the lights on when we need it most.”

Officials in New Jersey, an importer of energy, argue that solar and storage development are key elements in the effort to boost electricity generation, and that the two methods can create power more cheaply and rapidly than would be possible by developing other sources, such as nuclear or gas generation.

New Jersey, like other states in PJM, faces a dramatic increase in demand, due mainly to the expected development of energy intensive data centers. PJM also argues that future energy capacity has been hindered by the closure of fossil generating sources at a faster pace than new sources — mainly clean energy — have come online to replace them.

Officials say the predicted shortfall in generation contributed to a 20% increase in the average New Jersey electricity bill in June.

Powering 1M Households

Murphy said he expected the new laws to “build a cleaner, more resilient future” for state residents.

“By accelerating the process for bringing new sources of energy online and rapidly building new energy storage facilities, we will meet growing demand while also making life more affordable for our state’s families,” he said at a press conference Aug. 22.

The New Jersey branch of the Sierra Club said the solar legislation would “enable the equivalent of one million households to receive solar power by 2028.” The storage bill will “vastly” accelerate the construction of storage in the state, the environmental group said in a release.

“Energy storage is essential to make renewable energy sources like solar provide energy to its fullest potential by allowing excess energy generated during sunny periods to be saved for peak demand,” said Anjuli Ramos-Busot, director of the club’s state branch. “Incentivizing transmission-scale energy storage while increasing community solar targets will generate more power capacity, help reduce cost of electricity, improve grid reliability, reduce emissions and combat climate change.”

New Jersey’s community solar program has been a bright spot, and a source of pride for state officials. The first two solicitations in the program were fully subscribed, allocating 500 MW of capacity. A third solicitation is underway. The program is seen as a key element in the state’s goal to reach 12.2 GW of solar energy by 2030 and 32 GW by 2050.

The BPU’s June report showed that 456 community solar projects were providing 740 MW, or about 11%, of the state’s 6.56 GW of installed solar capacity. BPU officials in the past opposed efforts to dramatically expand the program, saying the extra stress would negatively impact the state’s solar programs. (See NJ BPU Opposes Community Solar Program Expansion.)

New Jersey has struggled to develop storage. The state missed a legislative goal of developing 600 MW of storage by 2021 and now is seeking to put 2,000 MW of storage in place by 2030. (See Developers Seek Deadline Extension in NJ Storage Plan.)

FERC on Aug. 25 granted NextEra Energy’s request to waive certain rules under MISO’s tariff to allow the company to restart its Duane Arnold nuclear plant by the end of 2029.

The commission ruled that NextEra is free to combine interconnection service and alter a point of interconnection, bringing the company a step closer to recommissioning the 50-year-old Duane Arnold Energy Center in Palo, Iowa (ER25-2989).

NextEra is in the process of reinstating the plant’s operating license with the Nuclear Regulatory Commission and claims it could resume commercial operation on the plant by the end of 2028 at the earliest and the end of 2029 at the latest.

In its Aug. 25 order, FERC permitted NextEra to combine leftover interconnection service at the site and use a nearby standalone interconnection agreement from a NextEra affiliate company to accommodate Duane Arnold’s historical peak winter net capacity range of 600-619 MW.

The commission also allowed NextEra to use MISO’s generator replacement process to support recommissioning, even though an affiliate company — and not NextEra itself, the historical owner — is heading recommissioning efforts and cannot meet the original commercial operation deadlines of the stitched-together interconnection services.

The Duane Arnold plant was idled in August 2020 after a derecho damaged the plant’s cooling towers and Alliant Energy ended its power purchase agreement five years ahead of schedule. NextEra subsidiaries quartered Duane Arnold’s interconnection service among four planned solar farms, only one of which was constructed and sold. The three remaining solar generator interconnection agreements are set to be bundled with NextEra affiliate Kinsella Energy Center’s 200-MW interconnection service to support the nuclear plant’s re-entry on the grid. NextEra plans to consolidate the interconnection service at the 161-kV level.

NextEra said equipment necessary to repower the plant, including generator step-up transformers, isn’t scheduled to arrive until 2028, making the 2026 commercial operation target of the trio of original solar plans infeasible. The plant’s boiling water reactor is currently in long-term storage after being de-fueled.

‘Old-fashioned Way’

In its order, FERC also accepted NextEra’s request for a Dec. 31, 2029, commercial operation deadline and agreed with the company that a late 2029 restart date would allow for “unexpected delays resulting from challenges driven by the complexity of a project of this nature including parallel supply chain activities, physical site work and regulatory processes that will be required to return the plant to power operations.”

NextEra said it and MISO agreed that a change to the point of interconnection would have “no material adverse impacts” on the grid or other interconnection customers.

NextEra said without waivers of MISO’s interconnection rules, it could have been forced to start fresh and apply to enter the RTO’s interconnection queue, which could add years to the restart goal.

FERC said NextEra “acted in good faith in investing significant capital and securing interconnection rights in order to pursue a consolidated [generator interconnection agreement] necessary to recommission Duane Arnold.” NextEra said it could invest anywhere from $50 to $100 million over 2025 to fire up the plant within three to four years.

The commission said without the waivers, MISO would have been forced to terminate the existing interconnection rights that Duane Arnold is counting on to reconnect. It said granting extra time would give NextEra the space to “obtain regulatory approvals, procure necessary equipment and recommission Duane Arnold.”

Pamela Mackey Taylor, director of the Iowa Chapter of the Sierra Club, protested the waivers and said they weren’t necessary because they weren’t caused by unforeseen circumstances. Taylor argued also that the nuclear restart would lead to the abandonment of about 600 MW of solar development, making impacts more pronounced than NextEra claimed. Finally, she said NextEra has no guarantee from the NRC that Duane Arnold can reopen.

NextEra said data centers’ need for high-capacity baseload generation led it to alter its solar power plans at the nuclear site.

FERC said it wasn’t presented evidence that the solar projects will be “wholly abandoned.” The commission also said it would not opine on NextEra’s proceeding at the NRC.

Speaking at Infocast’s 2025 Midcontinent Energy Summit on Aug. 19, MISO Senior Vice President Todd Hillman said nuclear power could play a bigger role in the RTO.

“In MISO, we’re just doing it the old-fashioned way. We’re turning on old stuff,” Hillman joked, referencing nuclear power plant restarts at Palisades in Michigan and Duane Arnold in Iowa.

On July 29, at 7 p.m., California’s three investor-owned utilities, in partnership with SunRun and Tesla, orchestrated the largest activation to date of customer-sited batteries across 100,000 locations.

Within seconds, 539 MW of power from this aggregated virtual power plant (VPP) was flowing back into the grid, reducing peak evening demand. This may have been the largest demonstration of its kind to date. It won’t be the last.

An Expanding Resource: Pacific Gas and Electric (PG&E) noted in its press release that the batteries were enrolled in California’s Emergency Load Reduction Program (ELRP) — which calls for 20 hours of dispatch annually — and the Demand Side Grid Support (DSGS) initiative — which requires at least one event per month. “If no real emergencies happen,” the utility said, “test events like this one will continue to make sure everything works as expected.”

Peter Kelly-Detwiler

California leads the nation with 686 MW of commercial and 1,829 MW of residential distributed batteries as of April, at more than 25,000 sites. That population is growing quickly in California and elsewhere, often in tandem with solar installations. SunRun reported that in Q2 of 2025, 70% of its customers also bought batteries (up from 54% during Q2 of 2024). The company is dispatching its battery fleet across the U.S., providing 340 MW of batteries to grids in California, Massachusetts, New York and Puerto Rico during a single June day.

Tesla operates in California but also is coordinating battery-based VPPs in Texas, where it gained approval in 2023 to participate in ERCOT’s Aggregated Distributed Energy Resource (ADER) pilot project serving Houston and Dallas. It coordinates with VPP platform company Energy Hub to provide services to Massachusetts, Connecticut and Rhode Island while overseeing a separate aggregated offering in Puerto Rico.

Utilities Increasingly Embrace VPPs: Across the U.S., more utilities are deploying batteries to push the boundaries at the grid edge, offering reliability to customers while creating capacity management, renewables integration and grid balancing services.

To cite some examples, Utah’s Rocky Mountain Power launched a pilot six years ago, connecting 12.6 MW of batteries deployed by solar and storage company Sonnen to its control room. Following that success, it received approval from the state’s regulators in 2020 for a tariff to retrofit batteries to existing distributed solar installations. This year, it went further, signing an agreement with Torus for up to 70 MW of distributed storage systems using batteries and flywheels.

Batteries on Wheels help school districts access grid revenues | Electric School Bus Initiative

Vermont’s Green Mountain Power (GMP) continues to expand its battery program started in 2016. By 2023, it had 22 MW of distributed batteries that had delivered 10,000 hours of backup power to customers during the previous winter. Under GMP’s program, customers can lease the batteries or own them and receive rebates for participation in the utility’s Bring Your Own Device aggregation program, which pays participants up to $10,500. As of 2025, 5,000 customers are engaged in the program, with batteries both providing backup power and helping GMP reduce exposure to wholesale power costs by an estimated $3 million this year.

Minnesota’s Xcel Energy is adopting a unique approach, installing solar arrays and batteries as part of a distributed capacity program including up to 1,000 MW of DERs in a utility-owned and rate-based VPP. The plan won regulatory approval in February, with a detailed proposal expected this October.

VPPs Go Well Beyond Batteries: While batteries form the backbone of many VPPs, other technologies often are involved. Grid-interactive water heaters frequently participate in load-shifting and peak management programs and have provided frequency regulation services.

Air conditioners and smart thermostats also are part of the mix, with VPP programs expanding in recent years as technology improves. Late in 2024, for example, NRG teamed up with Renew Home and Google Cloud in Texas and aims to distribute, connect and orchestrate hundreds of thousands of thermostats into a 1,000-MW AI-powered VPP by 2035.

Electric Vehicles: Class of Their Own: EVs represent a potentially massive and growing resource. Sophisticated charging architectures and improved batteries now can accept charges of 300 kW or more (and trucks can exceed 1MW). It will become increasingly important to manage when they are charged. The cost of not doing so can run quickly into the billions, as distribution grids come under significant related stress.

Water heaters can shift load, AND help manage frequency | Brattle Group

EV batteries are big, especially when compared to residential storage. The bidirectional capable battery in the smaller of the Ford 150 Lightning models is 98 kWh, more than seven times larger than a 13.5-kWh Tesla Powerwall battery, while the large Ford version boasts 130 kWh. For its part, a typical “Type C” school bus battery sits around 200 to 300+ kWh.

Multiple auto manufacturers now include vehicle-to-grid (V2G) capabilities in charging and battery architectures to take advantage of the potential grid revenue streams. When BlueBird upgraded the warranty on its Type C bus battery to 360 MWh of lifetime throughput, it specifically cited the ability of EV fleet operators “to sell excess energy stored in school bus batteries back to electric power companies at a profit.”

While only a handful of drivers participate in bidirectional charging pilots, vendors and utilities are addressing the technical and behavioral challenges holding this potential back. School Bus V2G programs are having the most initial success, with 26 utilities in 19 states having rolled out programs to date.

Last year, leasing company Zum announced a program to deliver 2,100 MWh of energy annually from 74 electric buses (leased to the Oakland Public School District) back to PG&E. This month, PG&E teamed up with Fremont Unified School District (FUSD) and The Mobility House to manage 14 bidirectional-capable school buses.

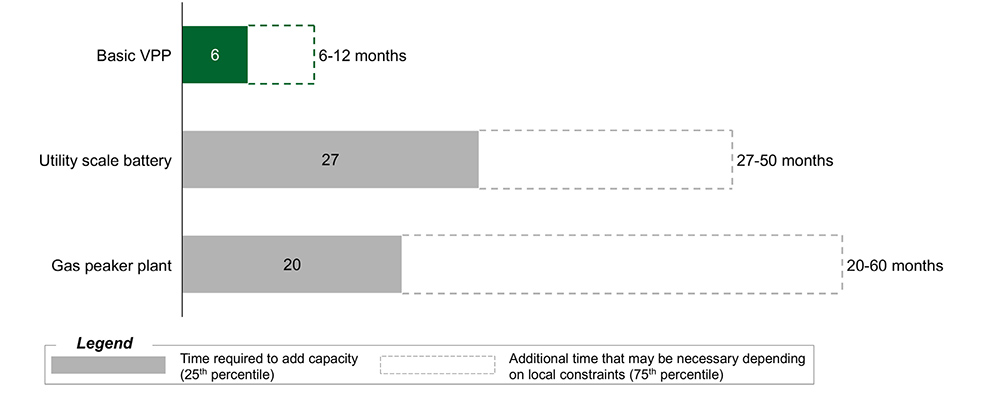

The Outlook: Fast, Flexible, and Expanding: As electricity demand grows, and generation has trouble keeping pace, VPPs offer a nimble alternative. A recent Department of Energy report (now unavailable on DOE’s website) found that VPPs can be built over just six to 12 months, far faster, and at a lower cost than batteries or gas-fired generators. The report also suggested that VPPs eventually could grow to represent as much as 10 to 20% of U.S. peak demand.

The DOE report noted that VPPs still face some critical obstacles. Areas to be addressed include simplification of asset enrollment, increased standardization of operations and improved integration of these aggregated resources into both utility and wholesale markets.

The VPP world is fragmented and generally characterized by pilots and evolving initiatives. There is a long way to go before we move from today’s typical demand response programs — with limited numbers of dispatch events — to a more seamless and price-responsive future, in which on-site assets simply react predictably to price signals or specific grid conditions.

Nonetheless, solutions providers are making true progress, and the achievements are considerable. To take some other examples: EnergyHub reports 2,000 MW of flexible load, made up of 1.7 million DERs. Demand response provider CPower manages 6,700 MW of dispatchable load across 23,000 customer sites, while its competitor Voltus stated recently that it is dispatching distributed assets every single day.

Timeline to add 20 MW of dispatchable peaking capacity, months | DOE

The challenge of resource adequacy will become increasingly critical as supply resources struggle to keep up with rapidly growing demand. However, as artificial intelligence and grid software improve, VPPs will become an even more helpful tool for improving economic efficiency, reliability and resilience. Keeping the lights on in the decades to come may in part depend on how quickly these virtual power plant resources become a normal part of our electricity landscape.

Around the Corner columnist Peter Kelly-Detwiler of NorthBridge Energy Partners is an industry expert in the complex interaction between power markets and evolving technologies on both sides of the meter.

Adapting charging of electrical vehicles to real-time grid conditions could save utilities up to $30 billion annually by 2035 and reduce peak energy demand, according to a new report by The Brattle Group and smart charging provider ev.energy.

The purported benefits would come from enabling managed-charging programs that encourage off-peak charging. This reduces strain on the grid and can help utilities avoid costly infrastructure upgrades, according to an Aug. 21 press release.

The report finds that managed charging can save up to $575 for each EV and 10% on home utility bills, with benefits potentially doubling with the inclusion of bidirectional charging, according to the release.

“As demand grows, and the world electrifies, there’s a real risk that households across the U.S. will face higher energy rates,” Nick Woolley, CEO of ev.energy, said in a statement. “The challenge for utilities is demand is rising fast, and traditional solutions — like building power stations — are slow to deliver and costly.”

Enabling demand flexibility can provide a solution and reduce rates across the board, Woolley added.

Citing data from the U.S. Energy Information Administration, the report states that forecasts show a 15% increase in peak demand by 2030.

“Electric vehicles represent a massive portion of this surge,” the report states. “While some forecasts predict a near-term slowdown, even conservative estimates project a 1400% increase to 60 million EVs by 2035 (Bloomberg, 2025), while others expect nearly 80 million (Edison Electric Institute, 2024),” the report states.

At the national level, EV sales in the first half of 2025 were up 1.5% year-over-year, with 607,089 vehicles sold, according to a report from Cox Automotive’s Kelley Blue Book. Second-quarter figures were down 6.3% year-over-year. Cox also noted the industry is facing further headwinds with government-backed incentives ending in September and economic pressures mounting. (See Calif. Fights to Maintain ZEV Momentum.)

Still, “the fundamental per-vehicle value is so significant that the business case for managed charging remains urgent even under more conservative adoption scenarios, such as those highlighted in recent industry reports,” according to ev.energy and Brattle’s report.

A similar report by Brattle published in February found that New York could achieve 8.5 GW in “grid flexibility” measures by 2040, saving consumers more than $2 billion a year by using programs like managed charging. (See Study Finds Considerable ‘Grid Flexibility’ Potential in New York.)

The February study said implementing grid flexibility improvements could avoid $2.9 billion a year in power system costs by 2040, $2.4 billion of which could be returned to consumers. These cost savings come primarily from reducing how much investment in generation capacity would be needed to maintain reliability. Avoided distribution and energy costs were $408 million and $384 million, respectively.

Managed electric vehicle charging, heat pump load control and residential behind-the-meter storage all had significant potential for increasing grid flexibility, according to the February report.

In a statement on the most recent study, Ryan Hledik, principal at The Brattle Group, said: “Past analyses have shown that virtual power plants can deliver reliable power at costs up to 60% lower than traditional generators. This new research goes further — offering a rigorous, quantitative framework that confirms EV flexibility as a critical, cost-effective tool for preserving both grid reliability and affordability.”

IESO officials say they will release more information on how the ISO constructed its study of the potential for incremental energy savings in Toronto after stakeholders complained they lack enough details to comment meaningfully on the analysis.

At a webinar Aug. 21, IESO said it and Toronto Hydro could cost-effectively secure 219 MW of incremental summer demand savings and 50 MW of incremental winter demand savings through energy efficiency, demand response and behind-the-meter DER programs.

The savings are in addition to the forecast 847 MW (summer) and 757 MW (winter) of future electric demand side management (eDSM) program savings already reflected in the Toronto Integrated Regional Resource Plan (IRRP), according to the study, which was conducted with consulting firm ICF.

The results from the ISO’s draft Local Achievable Potential Study will affect recommendations for how non-wire alternatives can defer or reduce the need for more electric infrastructure. “The results show that incremental eDSM alone is not able to meet Toronto’s needs,” the ISO said in a presentation.

IESO asked for feedback on the results by Sept. 11. The final report is set to be published on the Toronto Regional Planning website in October.

But several stakeholders said they would be unable to respond intelligently based on the information the ISO has released to date.

“It would be very helpful if you could provide us with the draft report that you’ve got so we can look at your input assumptions, look at your analysis and give you meaningful feedback,” said Jack Gibbons, chair of the Ontario Clean Air Alliance. “Because some of your assumptions may be wrong. Some of your analysis may be wrong. And we don’t want to just take your findings that you’ve given us today on faith.”

IESO’s Tom Aagaard noted that the ISO received feedback on its input assumptions in a webinar in December and said the ISO still was refining its conclusions. “We’ll have to take back [to see] what we’re able to share sooner.”

“You’ve got a draft report from ICF. I don’t see why you can’t just share it now and be transparent,” Gibbons persisted. “What harm is it going to do to give us what you’ve got now?”

The study uses a bottom-up approach to estimate the total electricity savings at the station level. It employs a “digital twin” of Toronto’s building stock, to which eDSM measures are applied. The resulting savings are simulated at the building level and aggregated to the transformer station for each scenario. | IESO

Keith Brooks of Environmental Defence, Chris Caners, general manager of renewable energy co-op SolarShare, and David Robertson, of Seniors for Climate Action Now, agreed with Gibbons.

“Without an understanding of what the final assumptions are in more detail, it’s really, really impossible to give meaningful feedback,” Caners said.

IESO responded in an email the day after the webinar, saying it would work with ICF “to expedite the release of more detailed information on methodology and assumptions, including measure characterization and more information on achievable potential established from economic potential results.” The information will be posted on the Toronto Regional Planning engagement website.

Methodology

The study used two load forecasts:

A reference scenario assuming a steady increase in demand based on current policies and growth in EVs and electrified heating and “low/steady growth” of data centers.

A high-electrification scenario that assumes Toronto will meet its net-zero targets for buildings by 2040 (with 30% EV adoption by 2030 and 100% by 2040) and see “elevated” data center growth.

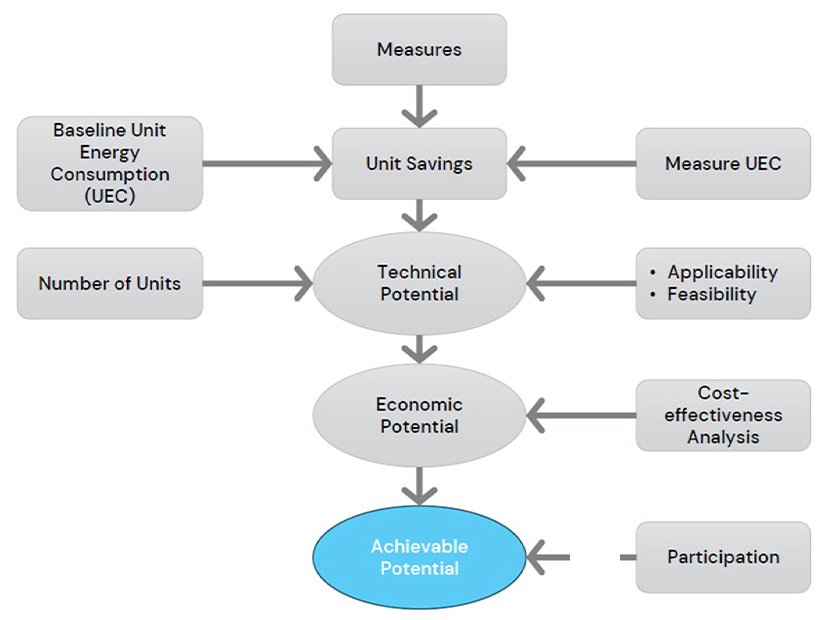

For each scenario, the study identified three levels of potential electricity savings:

Technical Potential. Savings from implementing all technically feasible measures regardless of cost-effectiveness and customer awareness.

Economic Potential. Savings from technically feasible measures that are cost-effective based on avoided generation (capacity and energy) and transmission costs and forecasted retail rates.

Achievable Potential. Savings that realistically can be acquired based on expected adoption rates considering market barriers and customer awareness.

The study used “digital twins” of Toronto’s building stock, to which DSM measures were applied. The resulting savings were simulated at the building level and aggregated to the transformer station for each scenario.

Draft Results

In 2045, the study concluded that achievable savings under the reference scenario were 1,066 MW in summer and 806 MW in winter:

Demand response (including EV charging, HVAC equipment and water heaters) had an achievable potential of 440 MW in summer and 324 MW in winter under the reference scenario. IESO said the difference in achievable potential between the reference and high-electrification scenarios is modest because the reference case includes significant heating electrification and because of the poor cost-effectiveness of EV demand response programs due to time-of-use pricing.

Energy efficiency (heat pumps, HVAC, lighting, appliances, weatherization and hot water) could save 605 MW (summer) and 471 MW (winter).

Behind-the-meter distributed energy resources (including battery storage and solar) could save 21 MW (summer) and 11 MW (winter). The low winter potential reflects the “limited value of solar to meeting winter needs,” the ISO said. Technical and economic potential match because measures in current Save on Energy programs including solar and solar-plus-storage were judged cost-effective. The reference and high scenarios had identical potential because the technical potential is affected by factors like usable rooftop area for solar rather than load.

Robertson and Brooks questioned the gaps between economic and achievable potential.

“It’s hard for us to give feedback on the results if we don’t understand how you arrived at them,” Brooks said.

“It would be really helpful and useful if there was something in your reports and presentations that talk about how do you close the gap,” said Robertson.

Existing Measures

IESO said the achievable savings in the study were muted because the Toronto IRRP already assumes 847 MW (summer) and 757 MW (winter) of new peak demand savings in 2045 from eDSM programs. In January, the Ontario government announced it would spend up to $10.9 billion on its eDSM programs through 2036.

The IESO and Toronto Hydro’s EE programs already have reduced peak demand by 800 MW in the past 15+ years.

The city’s Green Standard’s high energy performance requirements reduce the amount of additional cost-effective efficiency opportunities in new construction.

“Robust” participation in net metering, microFIT and other DER programs reduce the remaining rooftop solar potential, the ISO said.

Vehicle-to-grid

Another point of contention was the ISO’s decision to exclude bidirectional charging measures (vehicle-to-grid) from the study. The ISO said it could not properly model V2G based on current information and lacked confidence “that a program of meaningful scale could be delivered cost-effectively in the near future” because of the limited availability of vehicles capable of bidirectional charging, uncertain customer acceptance, costs and technological barriers.

Robertson questioned the ISO’s conclusion, saying “a study [with a] horizon to 2045 should anticipate developments” such as V2G.

Aagaard said it would be “kind of reckless” to include savings from V2G based on current information.

“We have very, very limited core data [to make] really important modeling assumptions to understand how much technical potential is actually out there. How many vehicles are actually going to have bidirectional charging capability? Do customers actually want this? Will [they] be willing to participate in programs when they’re called upon?” he said. “There’s just a million kind of consumer choice factors that come into play. … To include it in the modeling would be like really pulling numbers out of a hat.”

VALLEY FORGE, Pa. — An Aug. 11 load-shedding event in Baltimore was caused by equipment failure at the Brandon Shores substation, causing all breakers to open and cutting the city off from a major transmission feeder. (See PJM Initiates Load Shed in Baltimore Region After Substation Disconnect.)

Isolated from the 230-kV network passing through Brandon Shores, increasing strain was placed on the 115-kV lines running into the city until PJM issued a load-shed directive at 3:52 p.m. The load-shed directive was preceded by a voltage reduction action initiated at 2:15 p.m.

About 20 MW of load was shed for 28 minutes to mitigate an identified N-5 cascading outage risk that could have taken 1,200 MW offline, PJM Director of Operations Planning Dave Souder said at the Aug. 20 Markets and Reliability Committee meeting. He said PJM worked closely with Baltimore Gas and Electric (BGE) to identify regions where load shedding would be most valuable.

“We knew early on that we were going to have to go into emergency procedures,” Souder said.

Exelon Director of RTO Relations and Strategy Alex Stern said PJM worked extremely closely with BGE to limit the impact.

Six transmission lines intersect with the Brandon Shores substation, and two generators are tied into it: the 1,289-MW Brandon Shores and 843-MW H.A. Wagner, both owned by Talen Energy. The generators are running on reliability-must-run (RMR) agreements to maintain transmission security while network upgrades are constructed to facilitate their deactivation. (See FERC Approves $180M Annually for RMR Deals with Brandon Shores and Wagner Plants.)

Stakeholders questioned why the emergency procedures page and PJM Now mobile app incorrectly showed that the load-shed directive initiated a performance assessment interval (PAI), which would place capacity resources at risk of penalties if they failed to underperform.

PJM Senior Vice President of Operations Mike Bryson said staff took a broad stance on sending notifications that a PAI had been initiated to allay stakeholder concerns that capacity resources could be penalized without owners realizing an event had begun. Based on feedback since the Baltimore load shed, PJM is open to reconsidering how it sends those notifications and can add a discussion to the Sept. 11 Operating Committee agenda.

Souder added that the localized nature of the incident and its basis in a transmission emergency, rather than generation, precluded it from being a PAI. Responding to questions of whether a PAI would have been declared if load shedding were initiated across the BGE zone, he said they are declared for reserve zones, not transmission owner (TO) zones or subzones.

Bruce Campbell, of Campbell Energy Advisors, said the distinction between reserve and TO zones during emergency operations may not be widely known across stakeholders and may warrant further education. He added that there is only one reserve zone, which covers the full RTO, and one reserve subzone, Mid-Atlantic Dominion.

Several questions were raised about whether the two Talen generators were on outage during the event or if their availability contributed to the emergency. Souder said PJM does not publicly post information about generation outages and reiterated that the substation itself was unavailable. All available generation in the area was dispatched, but Brandon Shores was disconnected from the grid by the substation outage, and Wagner’s start-up time prevented it from coming online until the next day.

One of New York’s largest fossil-burning power plants will host a pioneering test run by a non-combustion hydrogen generator.

National Grid Ventures and Mainspring on Aug. 21 announced the project as the world’s first commercial installation of a linear generator operating on 100% hydrogen. September 2026 is the target date to start generating electrons.

The hope is that a year of rigorous testing on the grounds of National Grid’s Northport Power Plant will provide important lessons for potential larger-scale applications in commercial power generation. Along the way, its low-temperature, non-combustion process will produce minimal emissions and up to 250 kW of power for internal operations at the plant.

The project also could become a building block for the dispatchable emissions-free resources that are central to New York state’s clean-energy strategy in the 2030s and 2040s. No DEFRs have been identified that exist in scalable form.

“We were really drawn to the technology that Mainspring has to offer,” Will Hazelip, U.S. president of National Grid Ventures, told NetZero Insider. “This was really about seeing how that works and how it could potentially be a DEFR.”

The New York State Energy Research and Development Authority (NYSERDA) is contributing $2 million to the project.

The Long Island Power Authority also supports the effort. The Advanced Energy Research and Technology Center at nearby Stony Brook University will design the framework and methodology for the testing and then evaluate the results.

National Grid Ventures, the energy business arm of the UK-based utility, is confident it can obtain enough green hydrogen for the test program.

“So what we really want to be able to do is show that it’s fully capable of utilizing hydrogen as a fuel, and what that looks like in very specific generation technology terms,” Hazelip said, “so that specifically New York state has a better idea of how this particular type of technology could be a part of the energy mix in the future.”

The total project budget was not disclosed.

Mainspring’s linear generator is a 250-kW modular unit the size of a shipping container; it is compact enough that as much as 18 MW of capacity plus external inverters could be sited on a single acre. It operates at slightly more or less than 46% efficiency, depending on whether it is fueled with biogas, hydrogen, natural gas or propane.

The selling points are its simplicity (there are only two moving parts, and they do not need to be lubricated); its black-start and rapid-dispatch capacity; its versatility (it can switch from one fuel type to another, or use a blend, or use impure fuel); and its reduced emissions.

Nitrogen oxide emissions are near zero, because the fuel is being compressed rather than burned, and with carbon-based fuels the carbon emissions are lower than they would be in combustion systems.

Spokesperson Kevin Hennessy told NetZero Insider that Mainspring has deployed dozens of megawatts of capacity in the past five years for applications such as agriculture, landfills and wastewater treatment, the majority fueled by natural gas or biogas, and has hundreds more megawatts in various stages of its pipeline.

The Northport Power Plant was built by LILCO in phases starting in the 1960s as an oil-burning facility and later was converted to dual gas-oil capability. Its four main turbine-generator units are rated at a combined 1,516 MW and once provided more than a quarter of Long Island’s electricity.

National Grid has owned the facility since 2007, and while the plant is operated at a lower capacity factor than it once was, it remains an important grid asset. It recently reached its highest-ever output — 1,564 MW — during the July heat wave.

The state presents ambitious objectives and then creates an ecosystem to support these types of new applications, Hazelip said.

Mainspring, meanwhile, hopes to take what is learned in Northport and apply it nationwide, Hennessy said: “From our perspective, New York’s on the vanguard, leading the way with some thoughtful policy initiatives — certainly on the East Coast, but I think nationally — so it’s a great, great market to prove it out.”

NYSERDA President Doreen Harris said the project “represents a pivotal frontier in building a resilient electricity grid to power Long Island homes and businesses. This first-of-its-kind project will demonstrate how clean hydrogen can serve as a dispatchable resource to help maintain grid reliability while supporting an affordable energy transition.”

The $2 million grant for the Northport project comes through the Advanced Fuels and Thermal Energy Research Program administered by NYSERDA. The other grants announced Aug. 21 were:

GTI Energy, over $220,000 to evaluate New York’s geological hydrogen storage potential;

Plug Power, $2 million to partner with Verne to co-develop new hydrogen distribution trailers with cryo-compressed storage technologies;

Stony Brook University, over $4.9 million for a low-pressure, ambient-temperature hydrogen storage system at Northwell Health Hospital; and

SWITCH Maritime, $2 million to develop and demonstrate New York’s first hydrogen fuel cell-electric ferry.

A spokesperson said NYSERDA hopes to gain insight from the Northport project about the technology being used: “NYSERDA will analyze the project data throughout the demonstration, assessing the technical and economic viability of linear generators. The research will inform NYSERDA’s future work on clean hydrogen, and findings will be shared with the public and utilities to help determine potential pathways for broader adoption in New York state.”

FERC has replied to a request for clarification from NERC on its directive that the ERO revise the recently approved reliability standard requiring utilities to implement internal network security monitoring (INSM) at some grid-connected cyber systems.

FERC provided NERC the information it requested while denying a request from several trade organizations for a technical conference to provide further clarity (RM24-7).

The commission approved CIP-015-1 (Cybersecurity — INSM) on June 26, 2025; the standard requires utilities to implement INSM for all high-impact grid-connected cyber systems with or without external routable connectivity (ERC), as well as medium-impact systems with ERC. (See FERC Approves NERC’s Proposed INSM Standard.) FERC directed the standard’s development in response to the SolarWinds hack of 2020, in which malicious actors infiltrated the update channel of a common network management tool to push malicious code to customers worldwide.

Along with its approval of the new standard, FERC directed NERC to make further changes, due 12 months after the effective date of the final rule, requiring that utilities extend the implementation of INSM to electronic access control or monitoring systems (EACMS) and physical access control systems (PACS) outside their electronic security perimeter, the electronic border around their internal networks.

However, NERC later filed a request for clarification seeking to “eliminate ambiguity regarding the intended scope of the commission’s directive.” (See NERC Requests Clarity on FERC’s INSM Order.) At issue was the term “CIP-networked environment,” which FERC had used in an earlier notice of proposed rule-making (calling on the ERO to protect “all trust zones of the CIP-networked environment”) without defining it.

FERC said in its order approving CIP-015-1 that the CIP-networked environment “does not cover all of a responsible entity’s network” but does include “the systems within the [ESP] and network connections among and between [EACMS] and [PACS] external to the [ESP].”

NERC asked the commission to explain whether the term refers only to communication paths between CIP devices, or if it means “all communications on the network segment.” It also requested that FERC specify whether communication between PACS and non-PACS controllers are part of the CIP-networked environment.

The request for a technical conference came from the American Public Power Association, Edison Electric Institute, and the National Rural Electric Cooperative Association, which sought to confirm that FERC’s order “does not require monitoring of network traffic between non-CIP assets and intermediate systems that are classified as EACMS.”

In its Aug. 21 filing, FERC explained that the term “is not intended to capture non-CIP assets” and that the assets specified by NERC — non-CIP cyber assets, non-PACS controllers and non-EACMS firewalls — are all out of scope. This means that “for shared network segments located outside the electronic security perimeter containing both CIP (i.e., EACMS or PACS) and non-CIP assets (e.g., corporate devices), only the east-west traffic for access monitoring of EACMS and PACS is within the scope of the term CIP-networked environment.”

Regarding NERC’s second question, FERC confirmed that because non-PACS controllers are not CIP assets, “CIP-networked environment” therefore does not include “communication between PACS and non-PACS controllers.” On the other hand, communication between PACS and PACS controllers is in scope because such communication “is considered internal traffic of the PACS.”

In light of its clarification, FERC determined that its order “is sufficiently clear on how NERC should implement [FERC’s] directives” and that a technical conference is not required. However, the commission said NERC could hold its own conference if the ERO and industry stakeholders consider it appropriate.

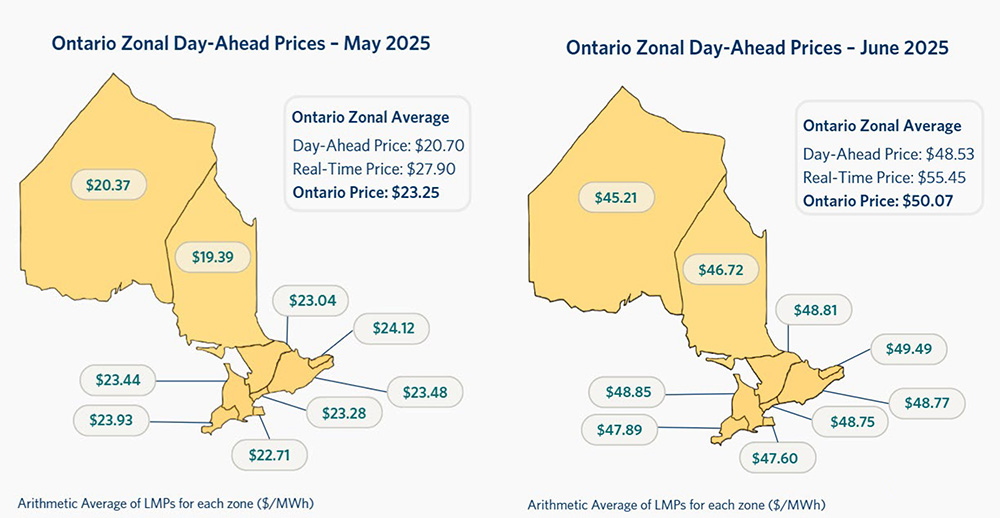

Nearly four months after the launch of Ontario’s nodal market, IESO officials say they are shifting from correcting implementation problems to seeking improvements to ensure the new model meets the goals of increasing market efficiency, transparency and competition.

“We’re getting … pretty close to what I would call more of a steady state … where we’ll be able to start to move from … addressing the day-to-day issues that come up for things that didn’t quite get implemented exactly as planned, to [looking at] the longer term,” Candice Trickey, director of Market Renewal Plan readiness, said in a briefing Aug. 21, the first in a promised quarterly series of updates. “How are things progressing? Are we seeing the things we wanted to see? … And where we aren’t, what do we need to [do to improve] that?”

Despite some implementation problems, IESO said the market has been working well, with prices strongly correlated to demand.

Data Points

Some data points as the market nears the four-month mark:

Nearly 30 traders have registered to transact in the virtual market, which allows them to submit hourly bids and offers in nine zones. Problems completing traders’ authorizations delayed the launch of the virtual market from May 8 to May 13. One large consumer has registered as a price-responsive load. Other organizations have begun the process of registering for the two new participation types.

All required participants have registered reference levels under market power mitigation rules, with some refining their values based on their experience in the market. Reference levels include energy and operating reserve prices and resources’ energy ramp rates and lead times. The Market Power Mitigation Working Group has reduced its meeting frequency to monthly, with “no significant issues” identified.

IESO said it has been issuing settlement statements and invoices within the required timelines, although increased processing times have resulted in invoices being issued later in the day than preferred by participants, an issue the ISO is working to address. The ISO created a Settlements Notifications webpage to advise participants of updates.

Participant inquiries have increased under the new market. IESO said its Customer Relations unit has answered 80% of inquiries within two business days, although more complex questions have taken “much longer.” The ISO said 40% of market participants responded to its final market readiness survey, with nearly 90% saying IESO’s Customer Relations or Marketplace Training were “very” or “somewhat” effective. About 63% of respondents reported they generally are “comfortable operating,” and 35% said that “non-critical” operations still are incorporating changes. Only a few organizations reported they were “struggling to operate effectively,” IESO said.

‘Defects’

As expected, Notices of Disagreement have increased since the market launch. The ISO has confirmed its initial statements in two-thirds of cases and attributed one-third to defects that have been corrected. The grid operator is working through a backlog of disagreements.

Most of the defects affected small groups of participants, such as price responsive loads and resources eligible for generator offer guarantees — non-quick-start resources that commit to economically scheduled hourly generation commitments in advance of real-time (RT) dispatch.

Candice Trickey, director of Market Renewal Plan readiness | IESO

But one defect, caused by a calculation error regarding residual uplifts, had a widespread effect. Although the two-settlement energy settlement amounts were calculated correctly, the day-ahead and real-time residual uplifts were calculated incorrectly and distributed to loads and exporters, resulting in adjustments to four uplift charge types. The ISO issued a notice Aug. 12 identifying the issue, the affected charge types and how resettlement will be completed.

Trickey said the rate of new defects in market systems has fallen from the first few weeks and that most were addressed with interim “workarounds” to avoid market effects.

One of the workarounds involved the five-minute interval Ontario Demand values reported in real time, which were overstated in some “limited circumstances.” IESO’s workaround “effectively adjusted forecast demand to largely mitigate this defect,” it said.

The ISO said some defects had no effect because workarounds were implemented, while others affected market outcomes briefly and required it to administer prices or correct schedules before settlement.

More complex defects required “extensive assessment” to determine if there was a material effect and could not be completed prior to settlement.

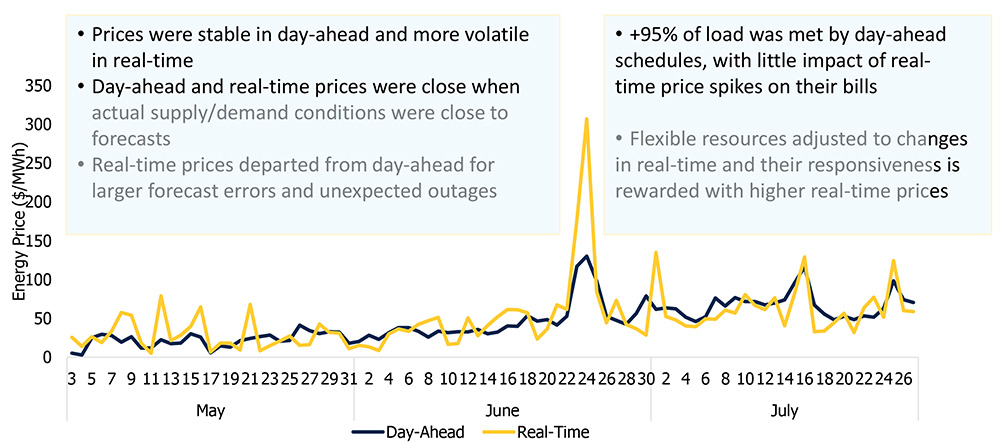

Real-time prices have been more volatile than the day-ahead market, with prices converging when actual conditions matched forecasts, and diverging when there were large load forecast errors or unexpected outages. | IESO

Thus far, the ISO said, two of those assessed had material effects necessitating the issuance of dispatch scheduling errors (DSEs): an incorrect calculation of the external congestion and net interchange scheduling limit price components for May 1-4; and an incorrect limit considered in the DAM for the ONT-PQAT interface on May 6. DSEs are issued when problems are discovered after settlements are issued; they allow the ISO to provide compensation to harmed parties but do not change prices.

Another five issues requiring extensive assessment are outstanding; the ISO said it likely will take another three to six months to determine whether these had material effects requiring DSEs.

Market Results

IESO officials said market results generally have been in line with expectations.

The market began during the “freshet,” the annual influx of water from spring rainfall and melting snow. Many hydropower projects must exit the operating reserve market and operate as “must-run” generators in spring because they have to flow the excess water through their turbines. (See Operating Reserve Prices Surge in Ontario.)

Joseph Ricasio, a member of IESO’s control room team | IESO

Summer brought its own challenges, Joseph Ricasio, a member of IESO’s control room team, said during the webinar. Hot weather sent the province’s demand soaring above its 2024 peak of 23,852 MW on seven occasions, with peaks as high as 24,862 MW. “I don’t remember the last time we received a lot of successive heat waves,” he said.

Between June 23 and 24, Ontario shifted from a net exporter during peak hours — as strong wind generation allowed it to ship energy to New York and Michigan — to a net importer as wind diminished.

It was a net importer on July 14-16 due to economic conditions and on July 27-29 as two large generators were “forced offline.”

“The generation and transmission performed very well this summer,” Ricasio said. “One advantage [of] being a net exporter is that it gives us a lever to address any adequacy concerns, and that’s because if it’s needed, we can curtail those exports.”

Despite the challenges, Ricasio said, the financially binding DAM has improved IESO’s ability to commit adequate generation for the next day. Some Level 1 Emergency Energy Alerts — a notice that all available generation resources are committed — have been identified based on day-ahead results, IESO said. “This gives advance notice to your neighbors that we may need their help,” Ricasio said.

‘Non-intuitive’ Results

Trickey said numerous participants have questioned “non-intuitive or unusual” market results. Some identified defects, while others were a result of the challenging summer temperatures and the new market’s multi-interval optimization.

“In an LMP market, the [offer] price is certainly an important determinant. But because we’re looking at optimizing over many, many intervals, [there can be] a difference in what the scheduling algorithm and the pricing algorithm are looking at,” she said. “So, you might see an offer close to the margin that appears uneconomic that gets scheduled.”

Director of Markets Darren Matsugu | IESO

Director of Markets Darren Matsugu said the market had produced prices “reflective of system conditions and efficient resource schedules” with real-time and day-ahead prices converging when actual conditions matched forecasts, and diverging when there were deviations in real time due to large load forecast errors or unexpected outages. Although real-time prices were more volatile than day-ahead, more than 95% of load was met by day-ahead schedules, minimizing the price effect on consumers, the ISO said.

“Moving from the mild temperatures in May — where we saw … seasonally low demands and abundant supply — into what’s turned out to be a very hot summer, we’ve seen an associated increase in entry market prices, which is exactly what we would expect,” Matsugu said.

“We also observed higher natural gas prices over the summer, and as gas is often the marginal resource during these two periods, that also has upward pressure on market clearing prices,” he added.

Prices have consistently separated between the north, where bottled hydro supply can suppress prices, and the transmission-constrained south.

“This past May when demand was relatively low and we had substantial baseload generation available, we had very few intermediary peaking resources that were already online and available to increase output immediately,” he added. “But what we have seen is demand has increased over the summer, and more and more of those resources are being committed ahead of real time, either in day-ahead or in pre-dispatch. This increases the amount of incremental flexibility that can be dispatched on the system, if required.”

Prices have consistently separated between the north, where bottled hydro supply can suppress prices, and the transmission-constrained south. | IESO

An average of 80 to 90% percent of non-quick start gas generators dispatched in real time — units that need one to six hours to start up and synchronize with the grid — were scheduled in the DAM over the first three months, providing grid operators and market participants “a clearer view and financial certainty for the next day’s operations while also leaving room to adjust to forecast uncertainty and outages in real time,” the ISO said.

Challenges in Scheduling of Pseudo Units

While the experience generally has been positive so far, “it isn’t perfect,” Ricasio said, citing IESO’s difficulties with pseudo unit (PSU) configurations, which model the mechanical interdependencies of combustion turbines and steam turbines.

Under the Renewed Market, PSU modelling is applied for DAM, pre-dispatch and RT timeframes for commitment, scheduling and dispatch.

IESO notified affected generators of workarounds to address the issues and said it is working on permanent fixes.

No Major Changes Expected

Matsugu said the market thus far has worked as designed to reduce out-of-market payments and increase efficiency.

“I do expect that over time, there’ll be some fine tuning that may be eventually required on these things, as is to be expected with any market — and particularly given the significance of the change that we’ve introduced with Market Renewal,” he said. “But at this point, there are no major design issues that require immediate fixes, just something that we’ll continue to pay close attention to.”

Matsugu cautioned that IESO had only two seasons of experience with the new market rules, saying it will gain valuable knowledge in the coming fall and winter.

“It is premature, I think, to draw too much based upon the still very short time frame that we’ve been operating,” he said. “We are still working toward … a steady state, where we can see the market performance under a diverse set of outcomes and conditions. [And] the participants themselves are still establishing their own competitive bid and offer strategies.”

Participants’ Questions

ISO officials answered several questions from stakeholders during the Aug. 21 presentation. Aaron Lampe, of Workbench Energy, asked about the effect of the market on pre-dispatch prices.

Matsugu said comparing PD prices before and after May 1 is “really comparing apples to oranges [because] in pre-market, our pre-dispatch was doing a one-hour optimization and not looking out across the balance of the day.”

“The only thing in common between pre-market pre-dispatch and our current pre-dispatch is really just what it’s called,” he added.

Rob Coulbeck, of Red Jar Energy Partners, said the ISO’s pre-dispatch three-hour look ahead was restrictive and asked if it could add another hour for import and export transactions that don’t clear in the DAM.

“I think that probably falls in the bucket of future design enhancements,” responded Matsugu. “There’s probably a whole bunch of different things that we can start to consider once we’re satisfied that the current market is performing.”