For decades, Portland General Electric watched electricity move from north to south through its system during the summer, as relatively cheap hydroelectric power from the Pacific Northwest flowed to California.

But now, the flow on a typical summer day has reversed, with electricity moving from south to north, PGE officials told the Oregon Public Utility Commission.

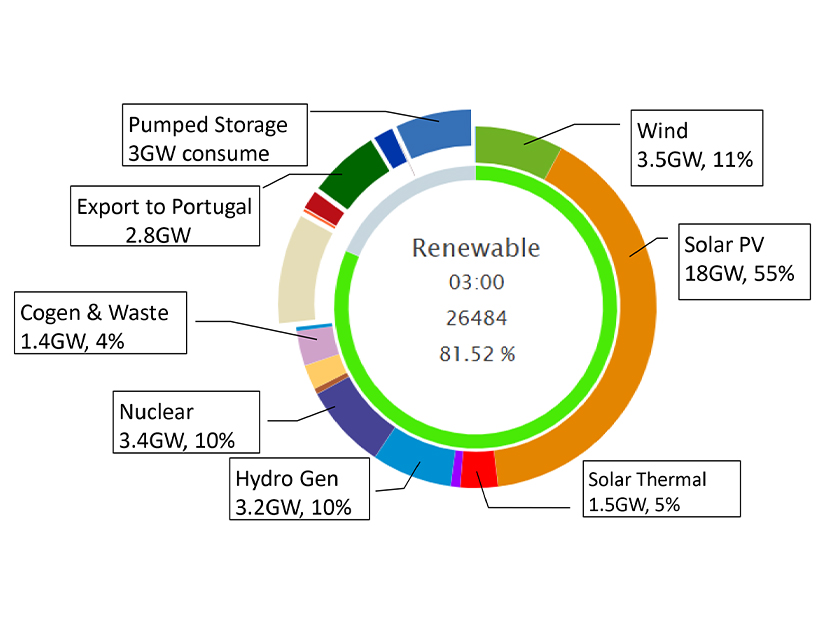

“With the 10,000 MW of batteries and 20,000 MW of solar that California has, we see a reversal of paths, where there is a huge northbound flow from California — cheap energy — up into the Northwest,” said Lee Recchia, PGE’s senior manager of the grid control center.

Recchia spoke during a special OPUC meeting on summer readiness on June 24.

The flow reversal has created issues that PGE “didn’t really see coming,” Recchia said, particularly on the North of Pearl transmission path. The Bonneville Power Administration owns the Pearl flowgate, and PGE partially owns some 230-kV lines out of Pearl.

“We’ve seen some overloads that we hadn’t seen in the past years, and it’s one of our big congestion points,” Recchia said.

PGE has developed a North of Pearl action flow chart for operators and a forecasting tool. The utility also is in regular discussions with BPA.

“It strikes me as one of those places where there will be really important coordination, as they move forward with their Markets+ decision,” OPUC Chair Letha Tawney said. “This could get hairy.”

PacifiCorp Preparations

Weather forecasters predict higher-than-average temperatures for most of the West this summer.

But PacifiCorp’s predicted summer peak of 11,163 MW is not a significant jump from its 2024 summer peak, according to Ben Faulkinberry, senior originator in the company’s energy supply business unit.

Since summer 2024, PacifiCorp has added 1,000 MW of wind resources and 320 MW of solar while also completing a 75-MW natural gas plant expansion. Another 400 MW of wind and 500 MW of solar are expected by the end of this summer.

PacifiCorp also energized the Gateway South transmission line, a 500-kV line that will carry electricity from the company’s wind power projects in Wyoming to the load center in Utah.

With the new line in service, curtailments of Wyoming wind are down by about 70%, Faulkinberry told the commission. And during the summer, when there’s less wind in eastern Wyoming, Gateway South gives PacifiCorp greater capacity to transact with market participants on the east side of the Rockies, he said.

“Our load requirement has not jumped substantially. We’ve added new resources. We’ve added new connectivity,” Faulkinberry said. “So we’re feeling, on the whole, pretty well-situated going into summer 2025.”

Still, PacifiCorp faces potential summer threats. One concern is the possibility of extreme heat simultaneously hitting the Pacific Northwest, Desert Southwest and California regions.

“That really puts a stress on our system as well as for the region as a whole,” he said.

Another worry is wildfire, which could affect transmission across the grid. Southern Oregon and southern Idaho, areas where PacifiCorp has “some pretty key connectivity,” are particular concerns, Faulkinberry said.

PacifiCorp also is expanding its demand response programs, including Cool Keeper, which has been a longstanding program in Utah.

Through the program, which PacifiCorp now is rolling out in Oregon, a technician installs a device that curbs power to the air conditioner compressor of a residence or small business. The company controls the device, and the customer can’t bypass it.

A typical Cool Keeper event lasts 5 to 15 minutes — enough time to stabilize the grid when it gets out of balance.

Because the fan and air handling components of the air conditioner keep running, customers generally don’t feel uncomfortable. Customers receive a bill credit for participating.

PacifiCorp forecasts that participation in Cool Keeper, along with a battery incentive program called Wattsmart, will offset the need to build three natural gas peaker plants within four to five years.